The whining over Labor’s proposed ban on self-managed superannuation funds (SMSFs) being able to borrow money to fund property purchases hit a crescendo over the weekend. Let’s take a look at the arguments on offer.

First up, The Australian editorial claimed that “Labor’s plan would cost us dearly”:

Bill Shorten wants to penalise Australians with the initiative to save for their retirements by investing in self-managed superannuation funds…

Labor’s decision to ban self-managed super funds from borrowing to buy property, as a means of curtailing the Sydney and Melbourne property markets, would create uncertainty for investors, who have made long decisions on the basis of current rules… Labor, which introduced compulsory superannuation in the Hawke-Keating years, should understand that principle…

Recently, columnists in this newspaper such as Robert Gottliebsen have demonstrated how the Turnbull government’s tinkering with superannuation rules has fuelled the rise of house prices in Sydney and Melbourne. Politically and economically, it makes little sense for either side of federal politics to tinker in the housing market… Labor’s housing and superannuation proposals show Mr Shorten would lead a centralist, interventionist government.

No facts, no evidence, just pure ideology and rent-seeking on behalf of its conservative baby boomer readership base.

Next, we have Firstmac – a non-bank mortgage lender – hailing the policy ‘populist’:

“This is populist politics at play here with various segments of the property market being held up and demonised as the cause of high property prices,” [CFO James] Austin said.

“It is easy to blame SMSF borrowers, it is easy to blame investors, it is easy to blame negative gearing. No politician is going to stand up in parliament and shed a tear for investors – they are a convenient mark.”

Next, enter the property lobby rent-seekers:

“We need investment in housing supply,” said Michael Corcoran, president of the Urban Development Institute of Australia.

“I don’t think it’s right for one investment class to be blocked to SMSF or super funds. We don’t think that banning or restricting super from investing in housing is going to help supply.”

The Property Council of Australia said the sharp increase of SMSF investment in property was not alone enough to curb the practice.

Finally, enter the SMSF industry lobby group:

SMSF Association CEO Andrea Slattery said there was “little or no convincing evidence” that the use of borrowing by small super funds was playing a significant role in affecting housing affordability.

Self-managed super funds own 0.18 per cent of the property market and banning them from borrowing will do nothing to bring down property prices or help first-home buyers, she said.

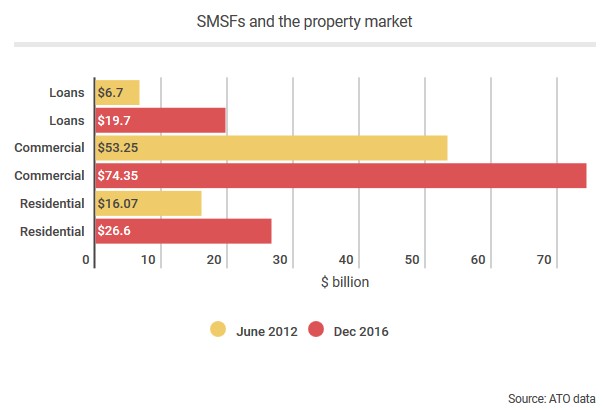

Now, let’s contrast the above special pleading with some actual data, which shows that SMSF leverage into property has grown strongly over recent years, adding to housing demand and helping to raise prices:

It is this embryonic growth of SMSF property leverage that prompted the final report of the Murray Inquiry into Australia’s financial system to explicitly recommend banning their ability to borrow:

Recommendation 8

Remove the exception to the general prohibition on direct borrowing for limited recourse borrowing arrangements by superannuation funds…Further growth in superannuation funds’ direct borrowing would, over time, increase risk in the financial system… In addition, borrowing by superannuation funds implicitly transfers some of the downside risk to taxpayers, who underwrite adverse outcomes in the superannuation system through the provision of the Age Pension…

Borrowing by superannuation funds also allows members to circumvent contribution caps and accrue larger assets in the superannuation system in the long run…

It is also inconsistent with the objectives of superannuation to be a savings vehicle for retirement income. Restoring the original prohibition on direct borrowing by superannuation funds would preserve the strengths and benefits the superannuation system has delivered to individuals, the financial system and the economy, and limit the risks to taxpayers.

The RBA raised similar concerns in its submission to the House of Representative’s Inquiry into Home Ownership:

Another change in the landscape since 2003 is that superannuation funds are now able to borrow. Some self-‐managed superannuation funds have taken advantage of this by adding geared property into the fund portfolio, both residential and, in particular, commercial property. At the margin, this has increased the population of potential investors. Although the share of the housing stock owned by these funds is small, it has grown quickly (RBA 2013). The Bank has previously observed that leverage in superannuation funds may increase vulnerabilities in the financial system and therefore supports limiting the scope for leverage in these funds (RBA 2014c).

Chris Joye has raised concern that the non-recourse requirement on SMSF borrowing means they could be similar to the sub-prime loans issued in the US in the run-up to the GFC:

“… the problem with a non-recourse loan is: it sounds very similar to a subprime loan in the US, which used to be called “jingle mail” because the lender had no recourse to the borrower beyond the asset itself, so they could just leave the keys in the house and walk away”.

Whereas independent economist, Saul Eslake, has argued that SMSFs have artificially pumped demand for housing, reducing housing affordability:

“The last thing Australia needs is more ways to channel funds into existing property.”

And Eslake has labeled the policy a big mistake by the Howard Government:

“This was a bad decision by the Howard government in its dying years,” Mr Eslake said. “Labor is absolutely right to be focussed on it.”

In a similar vein, Stephen Anthony, chief economist with Industry Super Australia, claims the SMSF involvement in residential housing investment was a negative:

“Do we want mechanisms like SMSFs, along with negative gearing and capital gains tax discounts, pumping up the housing market?”

“We have a supply issue but those measures are not targeted at supply.

“They also help maintain the budget deficit (because they cost the government money) which the ratings agencies will punish us for after the budget.”

In short, the Howard Government’s decision to allow super funds to leverage into property and other investments was a big mistake. Specifically, it allowed SMSFs to be turned into speculative vehicles rather than savings vehicles, in turn dramatically increasing the riskiness of Australia’s retirement savings and financial system, further inflating Australian house prices, and transferring some of the downside risk to taxpayers, who of course backstop the retirement system via the Aged Pension.

It’s a view shared by the FSI, the RBA, and others, therefore, Labor’s policy to ban SMSF leverage is not only justifiable but also entirely correct.