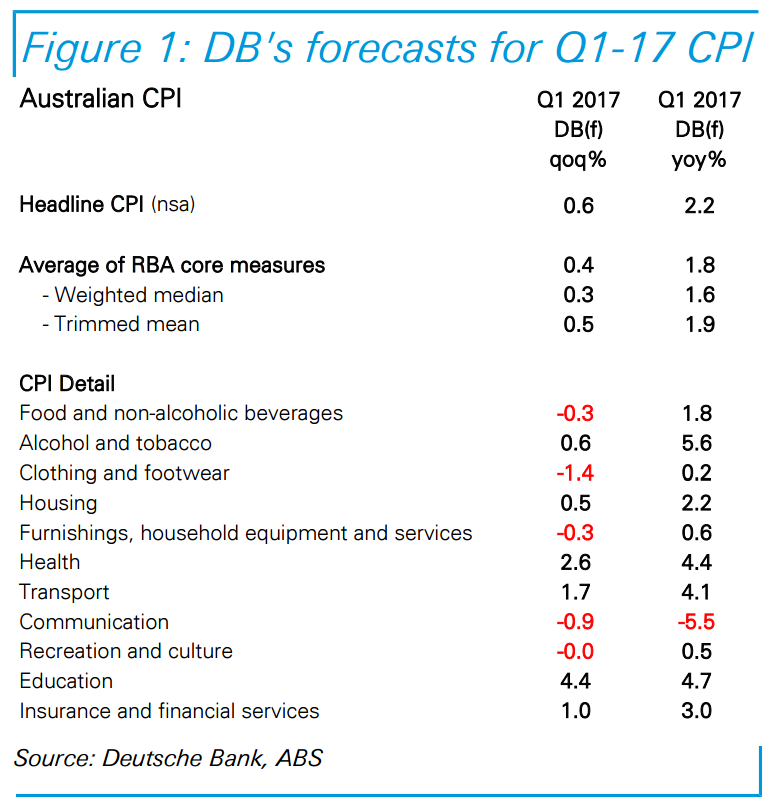

Our pick for Q1-17 headline CPI is for a 0.6%qoq/2.2%yoy outturn. We expect the average of the core measures to print at 0.4%qoq/1.8%yoy. We see headline CPI printing at 0.6%qoq in Q1-17 (due 26 April), and for the average of the core measures to print at 0.4%qoq.

Despite an apparent rise in wholesale fruit prices in the quarter, we expect both fruit and vegetable prices to fall in Q1, and this is the main driver of the overall decline we expect for the ‘food and non-alcoholic beverages’ group. The Melbourne Institute’s monthly inflation gauge noted falls in prices for fruit and vegetables in each month of the quarter. Moreover, recall that fruit prices rose by almost 20%qoq in Q3-16, with the ABS noting at the time the impact of “adverse weather conditions, including floods, in major growing areas”. Fruit prices only fell slightly in Q4 – and the usual pattern after large price rises is for a couple of quarters of downside correction. Aside from weakness in fruit and vegetable prices, we have also factored some moderation in beef prices following elevated price gains between Q1-14 and Q1-16.

For the housing group, we have factored some strength in utilities, but this is offset to some extent by ongoing weakness in rents. Note that from this quarter the ABS will augment the measurement of new dwelling prices by including a price index for attached dwellings (i.e. apartments). As we discussed in more detail in a note on 2 March, we expect this to impart modest downside pressure to the measurement of ‘new dwelling purchase’ prices. That said, we have also factored some offsetting upside pressure on dwelling prices more generally, reflecting capacity pressures associated with the high level of dwelling construction activity at present. Elsewhere, seasonal strength drives the rises we expect in the education and health groups, and we estimate a ~5.5%qoq rise in fuel prices in the quarter – the key driver of the gain in the ‘transport’ group. Seasonal weakness drives the expected decline in ‘clothing and footwear’. Our pick for the ‘recreation and culture’ group is for a flat outturn: data compiled by the Bureau of Infrastructure, Transport and Regional Economics points to a lift in domestic airfares in the quarter, while we expect international airfares to fall in line with typical seasonal patterns.

We expect core inflation to remain soft. Our pick is for trimmed mean at 0.5%qoq and weighted median at 0.3%qoq, leaving the average of the two RBA measures at 0.4%qoq and 1.8%yoy.

The Melbourne Institute inflation gauge rose by 0.9%qoq in Q1, which is stronger than our pick. Recall though that the inflation gauge rose by 0.8%qoq in Q4, against a 0.5%qoq rise in headline CPI.

We see few implications for the RBA if the CPI prints as we expect. Our forecast looks for a slight acceleration in year-ended underlying inflation, though this is impacted by base effects following the especially soft core inflation prints in Q1-2016 (when the average of the RBA core measures was just 0.2%qoq). We would characterise our forecasts as broadly consistent with the RBA’s projections as outlined in the February SMP (underlying inflation is expected by the RBA to be around 1¾% by Q2-17).

No impact in Q1 from Cyclone Debbie, some impact in Q2 (and possibly beyond), but with Banana crops spared this time around, we expect a smaller impact than Cyclone Yasi in 2011 Within the CPI basket, fruit and vegetable prices can be particularly vulnerable to adverse weather events. For the record, we do not envisage any impact in Q1 from Cyclone Debbie related damage and floods in Queensland and northern NSW. The cyclone impacted the mainland on March 28, so any retail price impact will not materialise until Q2, and possibly beyond. While it is hard to gauge the full impact at this early stage, we would expect a much less noticeable influence on headline CPI than during past cyclones. A key reason for this is that banana crops – which are uniquely vulnerable to domestic weather events because of quarantine-related import restrictions – have not been impacted this time around. Following Cyclone Yasi in February 2011, the ABS noted an almost 400% rise in banana prices over the six months to June. We would expect any price rises for other crops impacted by the latest weather events to be much more moderate.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.