The NAB survey continues to point to some other economy today:

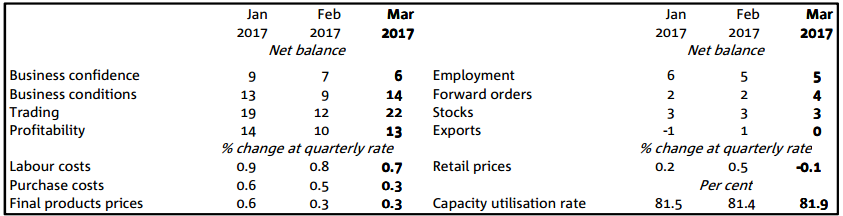

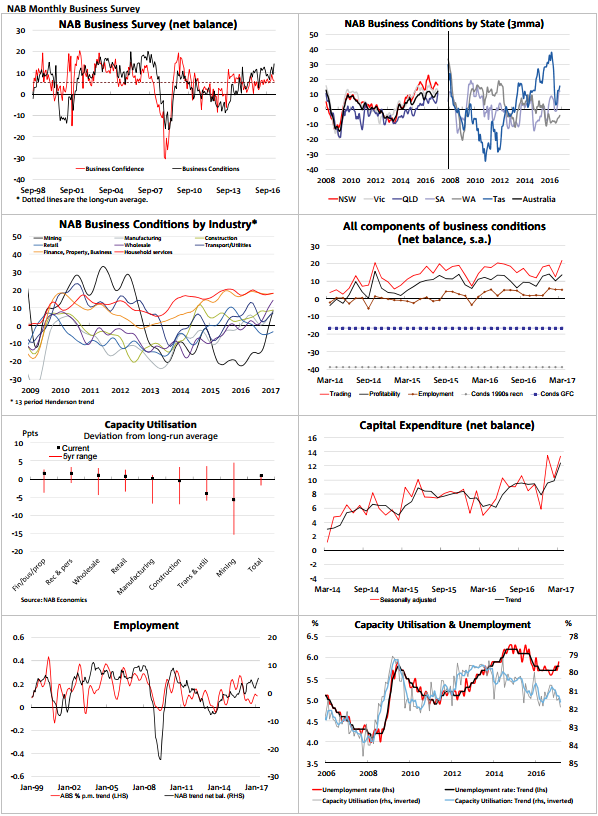

Results from the March NAB Monthly Business Survey indicate an overall healthy economy that appears to be gaining momentum, at l be gaining momentum, at least in the near- in the near-term. Business conditions have been fairly volatile of late, but the underlying trend has been encouraging – as is evident in service sector strength and the commodity price inspired jump in mining and Western Australia. That said, Cyclone Debbie may well be overstating Cyclone Debbie may well be overstating the one Debbie may well be overstating the magnitude of the kick in conditions magnitude of the kick in conditions in conditions as the number of respondents in the Survey from Queensland (and especially North Queensland) was the lowest since 2011. That is, the kick in Queensland conditions (up 12 to +20) may reflect a large concentration of respondents in the stronger South East vis-a-vis a struggling North Queensland. Overall, business conditions index jumped 5 points l, business conditions index jumped 5 points in March, to be at +14 index points in March, to be at +14 index points – ch, to be at +14 index points – and is trending well above long- trending well above long-run averages. run averages. run averages. Stronger trading conditions (sales) drove most of the improvement in business conditions, with the other components (employment and profitability) flat-to-modestly higher. The NAB employment index was stable and still suggests a healthier labour market than official ABS statistics. The lift in business conditions was not uniform across industries, however, with the major services sectors and wholesale making the largest contribution. In contrast, the retail industry continues to be a concern with conditions falling further, dropping into negative territory. Cost price measures in the Survey were modestly lower, while final prices were flat – although retail prices were much weaker (falling in quarterly terms). There was also evidence of higher commodity prices having an inflationary impact on the wages bill in mining.

• Business confidence outcomes have been more perplexi Business confidence outcomes have been more perplexing outcomes have been more perplexing, diverging somew ng hat from business conditions of late – albeit staying at solid levels. At this stage it is not clear what is driving a wedge between the two measures – global political uncertainty is a likely candidate although longerterm domestic uncertainties cannot be ruled out either. The business confidence index fell 1 point to The business confidence index fell 1 point to +6 index points in February dex points in February dex points in February, which is in line with the series long-run average. Meanwhile, other indicators were reasonably solid, with the capacity utilisation capacity utilisation rate lifting, consistent with acity utilisation a solid read on capital expenditure capital expenditure capital expenditure, while forward orders forward orders forward orders also rose in the month. • The March NAB Monthly Business Survey results are encouraging in terms of the near-term economic outlook. It suggests an improving labour market (in contrast to official measures) and an environment where non-mining business investment should continue to recover. This is consistent This is consistent with NAB’s outlook for economic growth to accelerate in H2 2017, following some likely disruption in Q2 from Cyclone Debbie. How 2 from Cyclone Debbie. However, recent volatility and ongoing weakness in the retail sector suggests there is still cause to be cautious about the longer- us about the longer-term outlook, particularly as other growth drivers (LNG exports, commodity prices and housing construction) begin to fade. Meanwhile, the RBA has emphasised its financial stability concerns, which are expected to keep them on hold for the foreseeable future. NAB Economics will release updated financial and economic forecasts tomorrow.

• The March NAB Monthly Business Survey results are encouraging in terms of the near-term economic outlook. It suggests an improving labour market (in contrast to official measures) and an environment where non-mining business investment should continue to recover. This is consistent This is consistent with NAB’s outlook for economic growth to accelerate in H2 2017, following some likely disruption in Q2 from Cyclone Debbie. How 2 from Cyclone Debbie. However, recent volatility and ongoing weakness in the retail sector suggests there is still cause to be cautious about the longer- us about the longer-term outlook, particularly as other growth drivers (LNG exports, commodity prices and housing construction) begin to fade. Meanwhile, the RBA has emphasised its financial stability concerns, which are expected to keep them on hold for the foreseeable future. NAB Economics will release updated financial and economic forecasts tomorrow.

Approaching boom conditions now. For some other economy!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.