From David Uren today:

Since gaining office in 2013, the Coalition government’s strategy for repairing the budget has had three elements: any new spending will be offset with savings measures; improvements in the budget resulting from strengthening of the economy will be banked, not spent; and the return to surplus will be assisted by savings that “build over time”.

The strategy is failing. If the forecasts in the first Coalition budget had been met, the Treasurer would be handing down a budget with a small $2.8bn deficit in four weeks and would be looking forward to a surplus next year. Instead, the deficit will be 10 times larger and a pivotal question will be whether the government can stick to its latest estimated date of a return to surplus in 2020-21. That surplus was halved to a mere 0.1 per cent of GDP in the December budget update, which is not much more than a rounding error.

…Morrison has no alternative strategy to the one that isn’t working. The government has not been able to generate a sense of urgency around budget repair, fearful that to do so would undermine confidence and make things worse. Economic growth has been reasonable and opportunities for the leadership shown by Peter Costello to achieve huge budget savings in 1996-97 and Paul Keating a decade earlier have been lost. A populist parliament is in no mood for sacrifices. Crossbench senators ask of every measure put before them, “Will this win or lose me votes?” — and vote accordingly. Labor is operating from Tony Abbott’s opposition playbook of rejecting everything.

Two years ago, former Reserve Bank governor Glenn Stevens told the House of Representatives economics committee that when a downturn arrived, the budget deficit would go from 2 per cent of GDP to 5 per cent or 6 per cent “in a heartbeat”. “Some of you will be there,” he warned the parliamentarians. At the moment, financial markets are more than happy to lend Australia the $30bn to $40bn a year it needs to cover its deficits. But they would be much less forgiving of deficits two or three times that size. The savings forced by financial markets in the middle of a downturn would be much more painful than those parliament thumbs its nose at today.

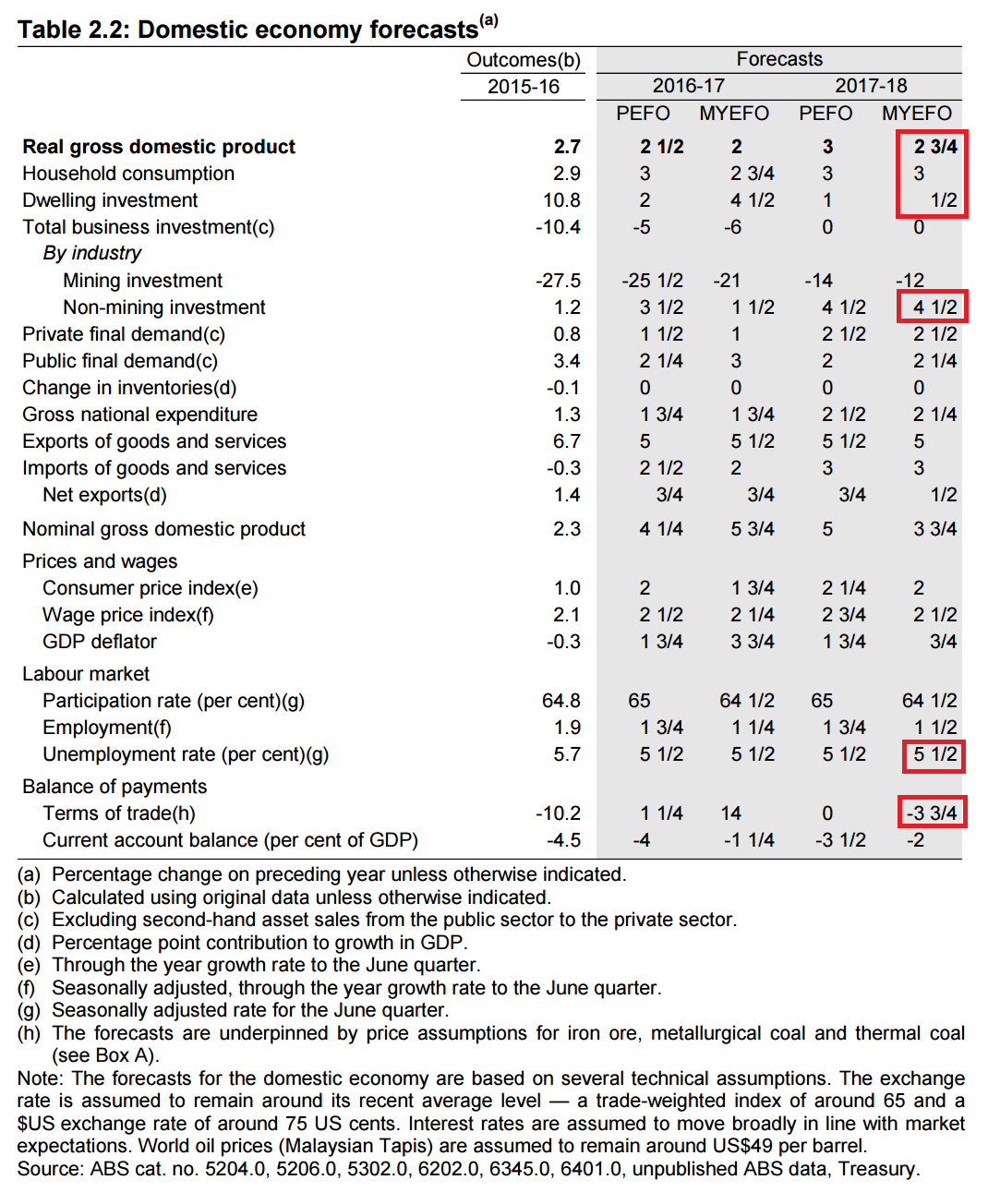

Quite right. And don’t forget that the economic forecasts remain too bullish as iron ore heads back to $50 and below in 2018 and coking coal with it:

Any short term commodity windfalls will go straight back out the door.

So there you have it. A Budget limping towards a sovereign downgrade even before the next global shock and, when it comes, a re-rating of risk such that interest rate may well RISE at the worst possible moment.

Nice job.