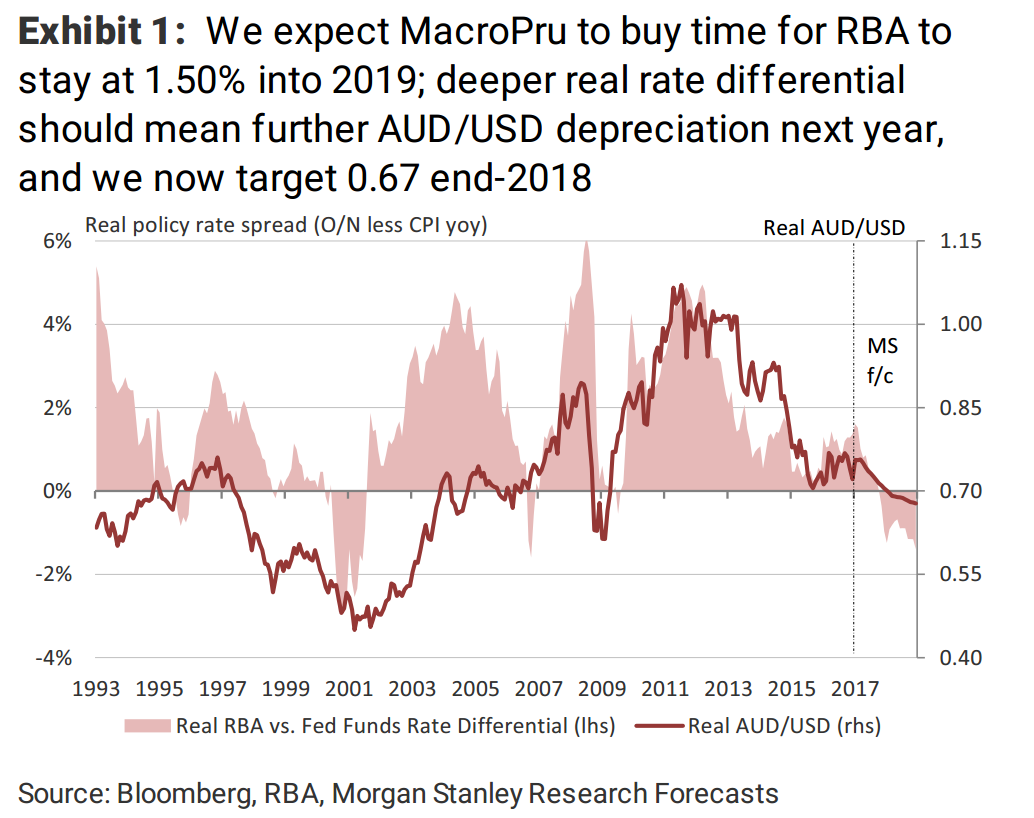

The RBA’s Rock and a Hard Place; On Hold Until 2019 The RBA is stuck at 1.50%, unable to cut given housing risks, yet unable to follow the Fed’s hikes given labour market weakness. Policy shifts further with MacroPru-2, and we now see the RBA on hold into 2019 while the market is pricing hikes. As a result, we lower our AUD forecast to 0.67 in 4Q18.

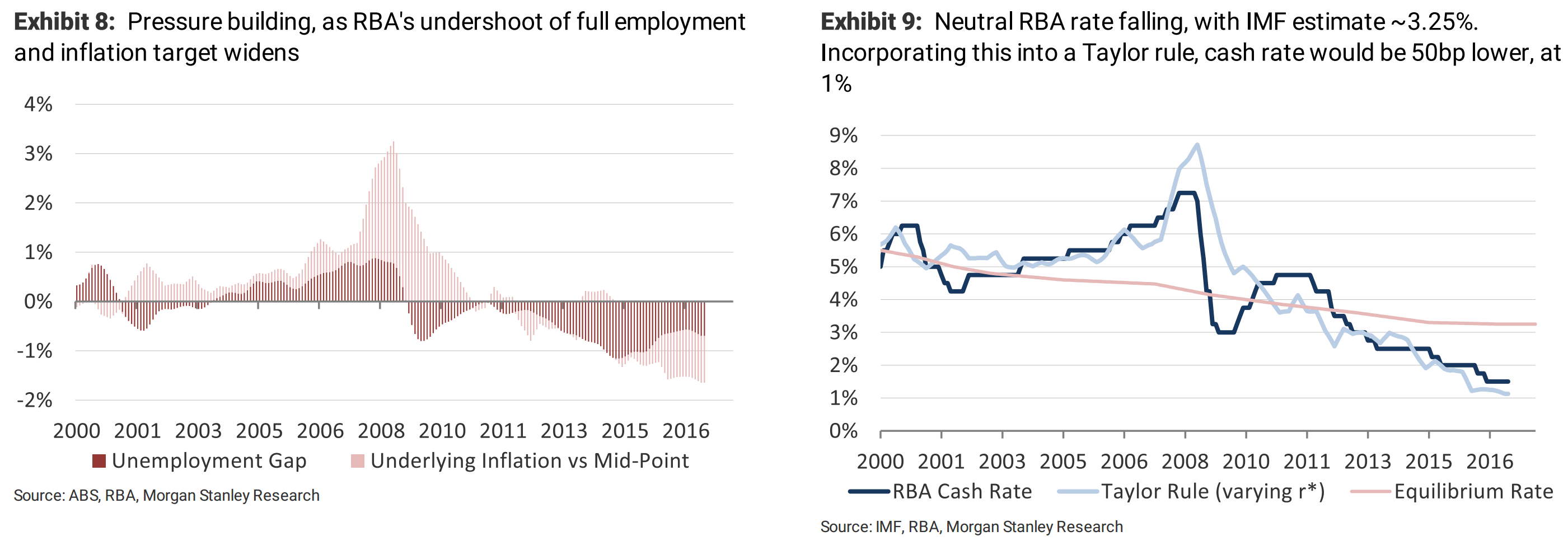

We believe the RBA cash rateis trapped between a rock and a hard place: Speculative conditions in established Sydney and Melbourne housing are the ‘rock’ preventing further rate cuts that are, in our view,needed to boost aggregate demand (in large part through a lower AUD). Meanwhile, the weak labour market and highly-geared household balance sheets are the ‘hard place’ preventing the cash rate from being hiked to tackle housing imbalances.

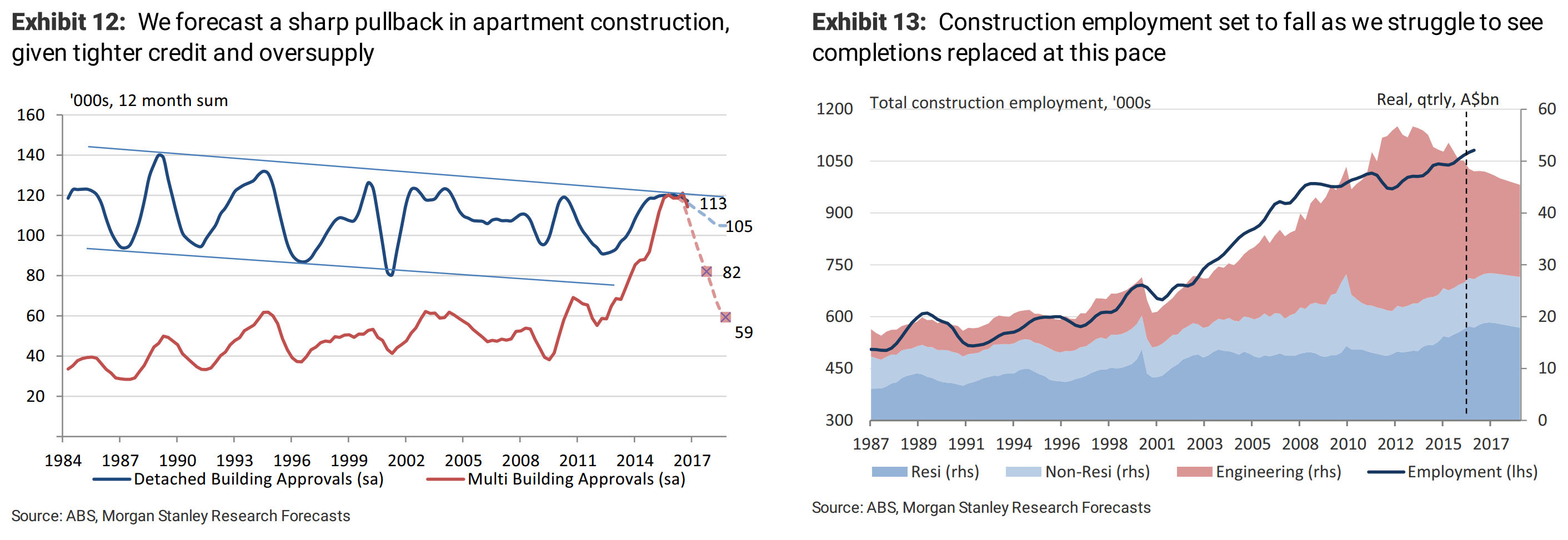

More reliance on MacroPru: Recent focus on cutting the share of interest-only mortgages is likely just the beginning of a two-step further tightening, with risk weights on investor/interest-only mortgages to increase materially, potentially as soon as June. This has macro implications, including tighter financial conditions, slower credit growth and tempered wealth effects. We see a cumulative -2ppt impact on household ‘free’ cash flow,and expect consumption to disappoint.

Macro – growth risks build: With monetary policy stuck and fiscal space underutilised, we think greater use of MacroPru will lower credit growth, slow the housing cycle (and wealth effects) and hold GDP down at our bottom-of consensus forecast.Furthermore – we expect the resi construction downturn to push unemployment towards our well-above-consensus 6.4% forecast.

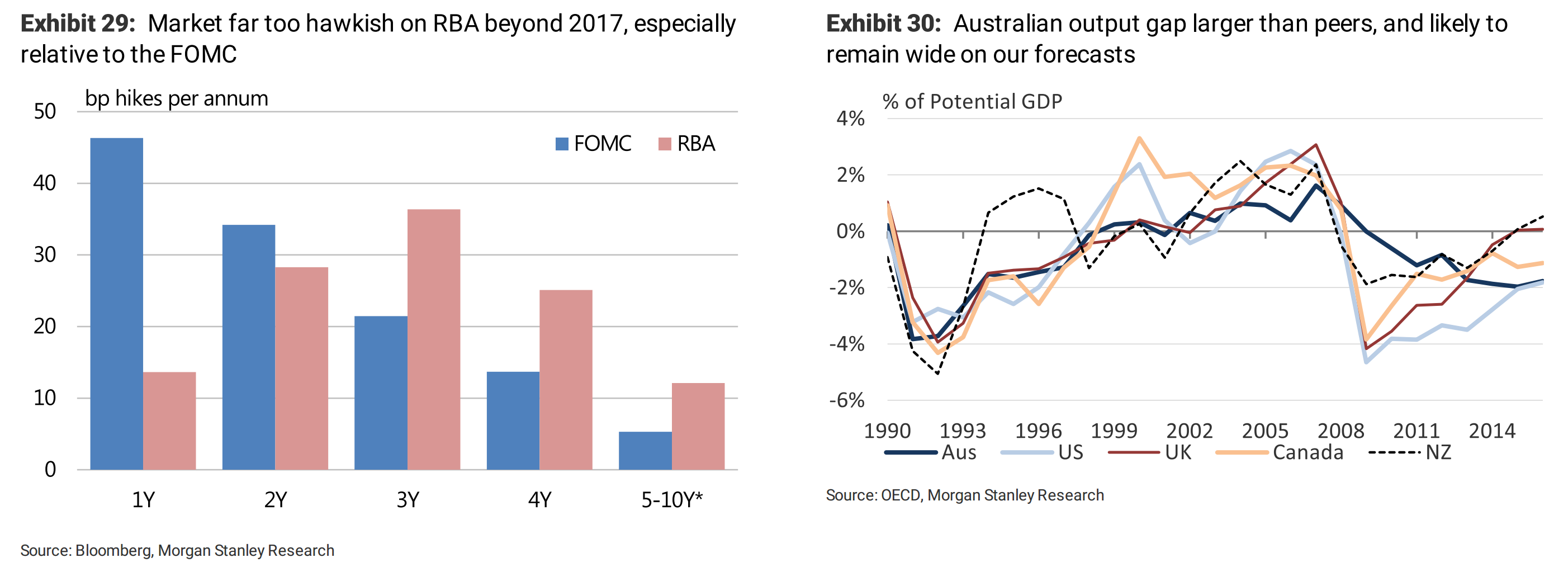

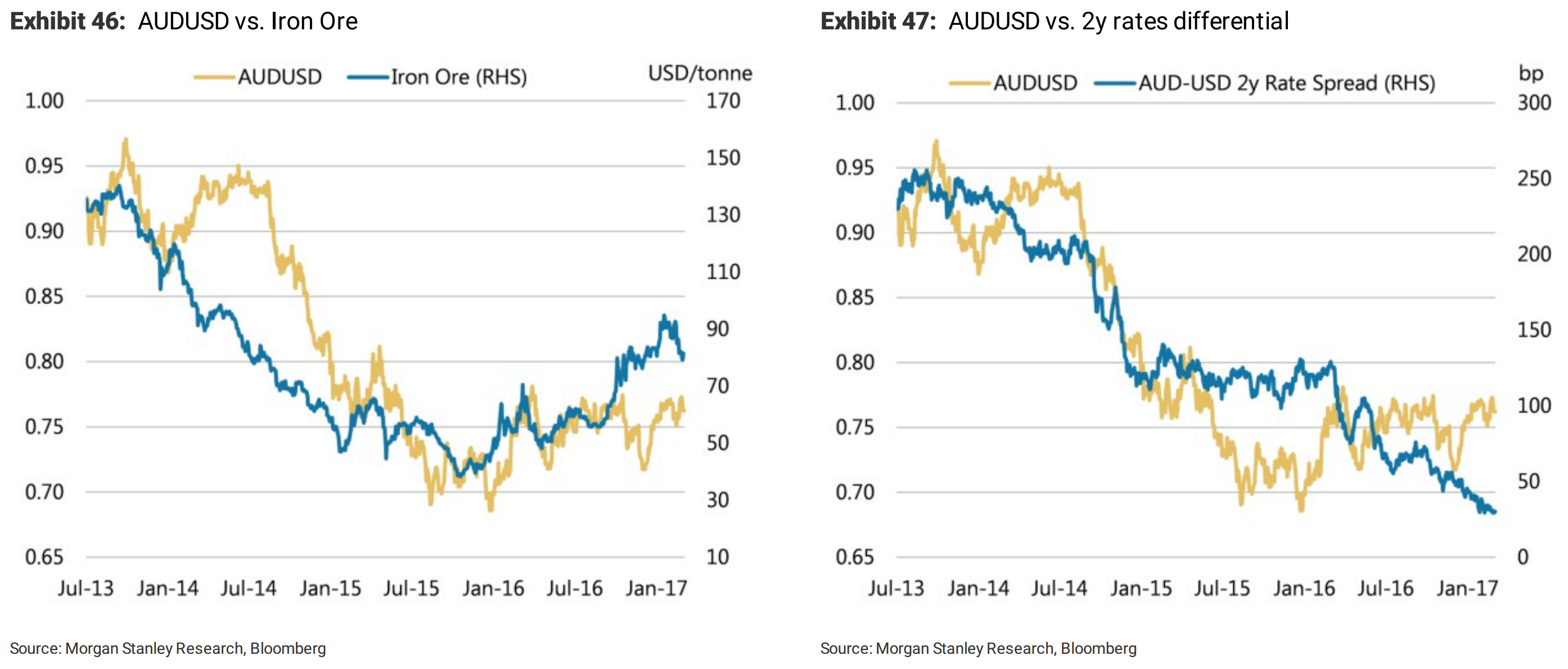

Rates – missing the price: The market is pricing the RBA to hike by August 2018, and by more than the Fed from 2019. We think this misses the fact that a 3% cash rate is equivalent to ~6.25% pre-GFC given world-leadinghousehold leverage. As a result, we like the front-end/belly of the AUD curve,and would look to enter 1y1y receivers around 2.10%.

FX – negative AUD carry: We believe the looming growth disappointments and a swing to negative rate differentials will pressure the AUD lower over 2018. With the removal of 50bp of RBA hikes in 2H18, our Global FX Strategy team lowers their 4Q18 AUD/USD forecast from 0.74 to 0.67.

Equities – UW the domestic cycle: The ASX200 outlook is oscillating around the perceived health of the domestic industrial cycle. Housing is the economy at present,and the slowdown underway means lower credit, income and consumption growth than consensus. We retain key UWs across Banks, Consumer,and Housing-Linked sectors.Focus should look back to Quality, Growth,FX-Earners and Resources for exposure to global reflation and value.

This is a fabulous report. The only problem is it is too bullish. MS’s outlook for iron ore is too high so all of its targets are too high as well. MB remains of the view that the next move for interest rates is down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.