by Chris Becker

A series of good news and possible intervention by Chinese authorities in the local stock market, coupled with some exhaustion has seen a generally positive day across Asia. Outside big falls in iron ore, commodity prices are generally stable as Australian bonds were sold off.

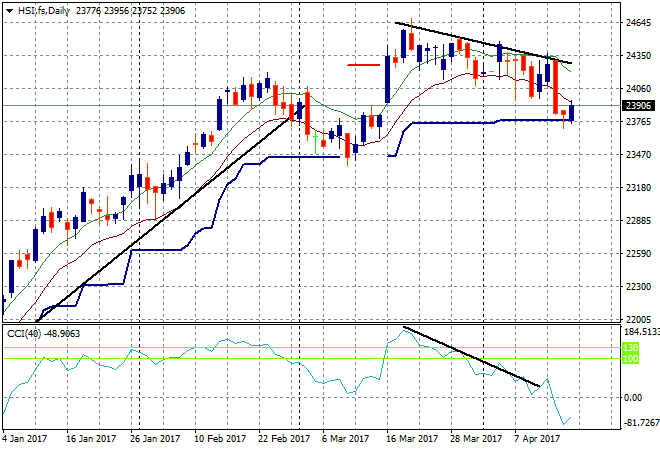

In China, the Shanghai Composite is steady going into the close, a late post-lunch dip mysteriously filled to make for a scratch session but still closing below key support at 3200 points. The Hong Kong based Hang Seng is doing a little better, up 0.4% to take back yesterday’s losses but still just below 24000 points as it remains tentatively above the trailing ATR support zone at 23700:

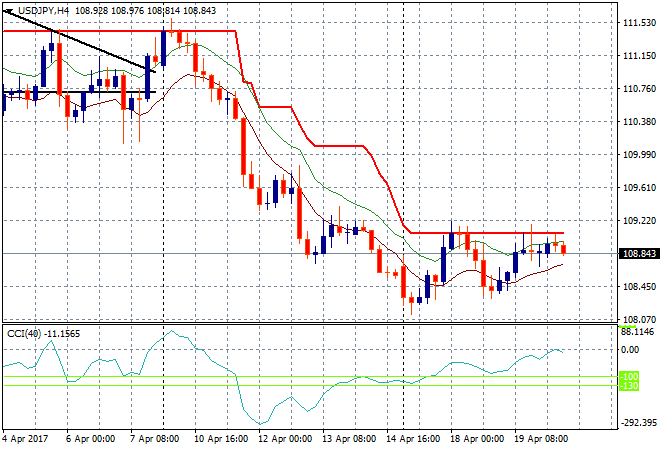

Some good trade figures didn’t really help Japanese stocks that much even as Yen sold off against USD, with the Nikkei putting in yet another scratch session, closing at 18430 points – still below key support at 19,000. The USDJPY pair has tried to build on its gains from yesterday, but refuses to head substantially above the 109 handle in what looks like more short term positioning before the London open as momentum remains negative on the four hourly chart:

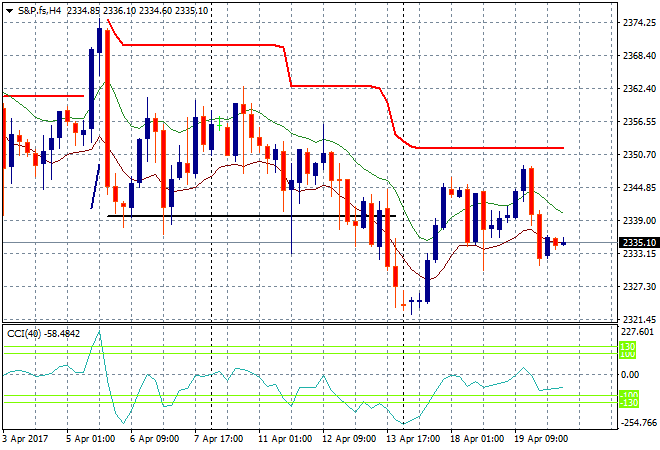

S&P futures are dour moving into the transatlantic session, not happy to take no selloff in Asia as good news:

The ASX200 finally put in a positive session, closing up 0.3% to 5821 points, albeit with high volatility across the majors, particularly banks and miners with oil stocks mainly ending up in the red on the continued LNG debacle and a drop in overnight WTI contracts.

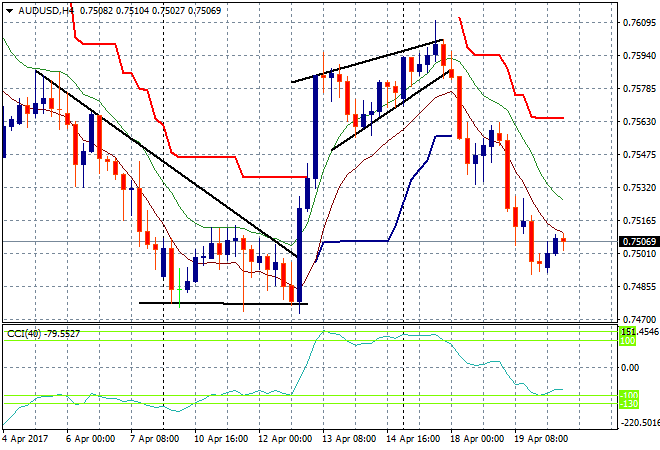

The Aussie dollar is trying to claw back above the 75 handle proper against USD but its looking extremely weak here going into the London open, unable to breach the low moving average on the four hourly chart:

The data calendar tonight includes a very closely watched speech by BOE Governor Carney in Washington followed by initial jobless claims.