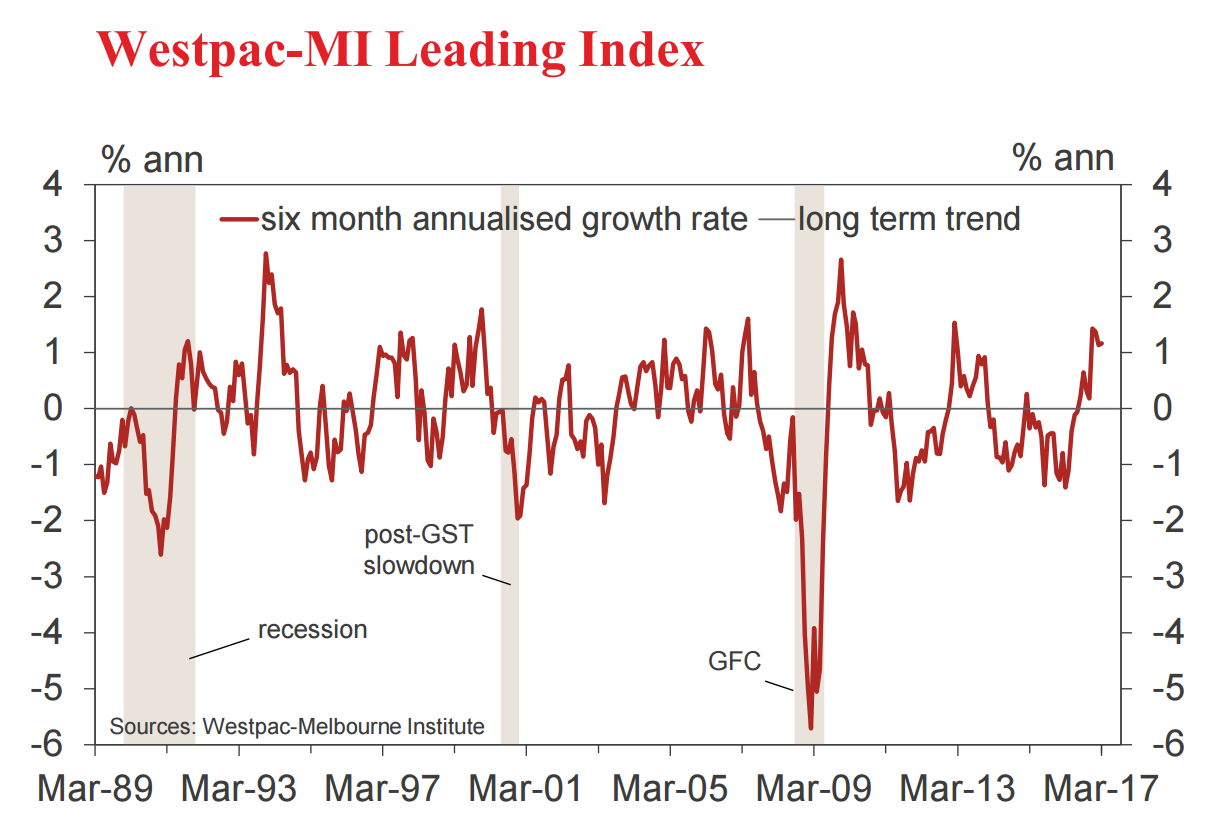

• The six month annualised growth rate in the Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from 1.14% in February to 1.17% in March.

This marks the eight consecutive month where the growth rate in the Index is at or above trend. That followed a period of fifteen consecutive months where the growth rate had been below trend. That sustained period of below trend growth in the series had been pointing to the weakness we saw in the economy in the September quarter (although no lead indicator could have prepared us for a negative growth print).

The resumption of positive growth in the Index in August last year gave us some comfort that the bounce back in growth in the December quarter to 1.1% could have been anticipated.

While the strong bounce back in the December quarter was partly statistical in response to the negative quarter in September the ongoing positive signal from the Index gives us some comfort that we can expect solid growth in the first half of 2017.

In the April minutes from the Reserve Bank’s Monetary Policy Board meeting (released on April 18), the statement included in the March minutes, “Year- ended growth was expected to pick up gradually to be above its potential rate over the forecast period”, was excluded.

It may be that the Bank is considering lowering its growth forecasts given its concerns with the labour market; wage incomes and the feedback loop to consumption.

“The comment in the March minutes was consistent with the Bank’s latest forecasts (midpoint) from its February Statement on Monetary Policy of 3% growth in 2017 and 3.25% in 2018.

Westpac concurs with the Bank’s current forecast of 3% growth through 2017. That growth rate is above trend and consistent with the positive leads from the Index over the last eight months.

However we do have concerns for growth beyond 2017. Prospects for growth in 2018 look discouraging. Housing construction is likely to be contracting through 2018 while export growth will slow and the terms of trade are likely to be falling, slowing nominal income growth. Prospects for an offsetting boost from household spending and business investment are not encouraging given the ongoing negative feedback loop from weak labour incomes to consumption and final sales.

The Leading Index growth rate has lifted over the last six months from 0.31% in October to the current 1.17%. Over that period the key drivers of that improvement have been global factors: rising commodity prices (0.52 percentage points); the steepening of the yield curve (0.29 percentage points); the ASX200 (0.19 percentage points) and US industrial production (0.11 percentage points).

Of less importance have been the domestic components: Westpac – MI CSI expectations Index (0.04 percentage points) and Westpac –MI Unemployment Expectations Index (0.02 percentage points).

In fact two domestic components have been a drag on the Index: aggregate monthly hours worked (–0.23 percentage points) and dwelling approvals (–0.07 percentage points).

The Reserve Bank Board next meets on May 2. The Board is certain to keep rates on hold. As discussed previously the Board is concerned about excessive household leverage which has been boosted by rising house prices. While this concern might be alleviated by a rate hike the real economy is in no shape to deal with higher rates. Considerable spare capacity persists in a labour market with the unemployment rate “stuck” at about 1 percentage point above the full employment level; inflation remains below the Bank’s target zone and is expected to remain at the bottom of the zone; and incomes and confidence are restraining consumption.

The authorities are therefore opting for a policy mix of steady official rates and heightened regulatory controls around the housing market. Indeed, in the Bank’s Board minutes for April it was noted that, “depending on how the system responds to the various measures, members noted that the Council of Financial Regulators would consider further measures if needed.

It’s pretty amusing that as Australia ploughs into one of the steepest terms of trade shocks ever that the LI is rising. Then again, it is only six months advanced so we I guess we can forgive it. One should never allow such mechanical indicators to paralyse one’s thinking.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.