Gas producers will argue the energy market regulator has it wrong on the risk of looming shortages on the east coast when they are hauled to Canberra again next week, calling into question part of the premise upon which Prime Minister Malcolm Turnbull declared an “energy crisis” last month.

The companies will also point to new domestic sales contracts as evidence they have responded to the Prime Minister’s request to make more local gas available from the Queensland LNG projects, despite those deals being months in the works.

…”The noises combing out of Canberra are the right ones but the reality is we are not clear on what the specific actions are going to be yet,” said Stephen Bell, chief executive of Qenos, the country’s only manufacturer of the basic polyethylene plastic, which depends on gas and ethane to run its plants near Sydney and Melbourne.

Gas producers look set to take issue with the forecasts from the Australian Energy Market Operator, which prompted Mr Turnbull to call the meeting.

Producers will claim that AEMO’s forecast over-estimated how much LNG the three Queensland export projects will ship. They say AEMO assumed the plants would all run at their rated capacity, while in reality they will produce less, particularly at Santos’s $US18.5 billion GLNG venture, which said last August it wouldn’t produce any more than its contracted sales.

The industry is also expected to point to the likelihood of gas being developed from the Arrow fields in Queensland owned by Shell and PetroChina, in contrast to AEMO’s forecast that excludes those resources in the absence of information on when they would come to market.

It’s all a whitewash. The amount of gas drip fed into the market has been tiny – 8Gj for Engie versus 200Gj needed – was pre-existing contract negotiations, and has clearly been targeted only at preventing blackouts not ending the pricing gouge. Arrow is not being developed at scale at all. It needs new “use it or lose it laws”.

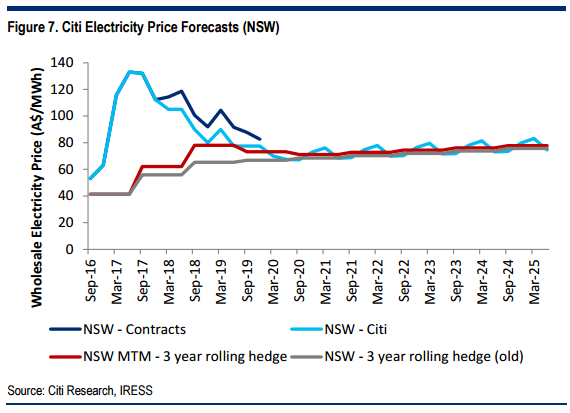

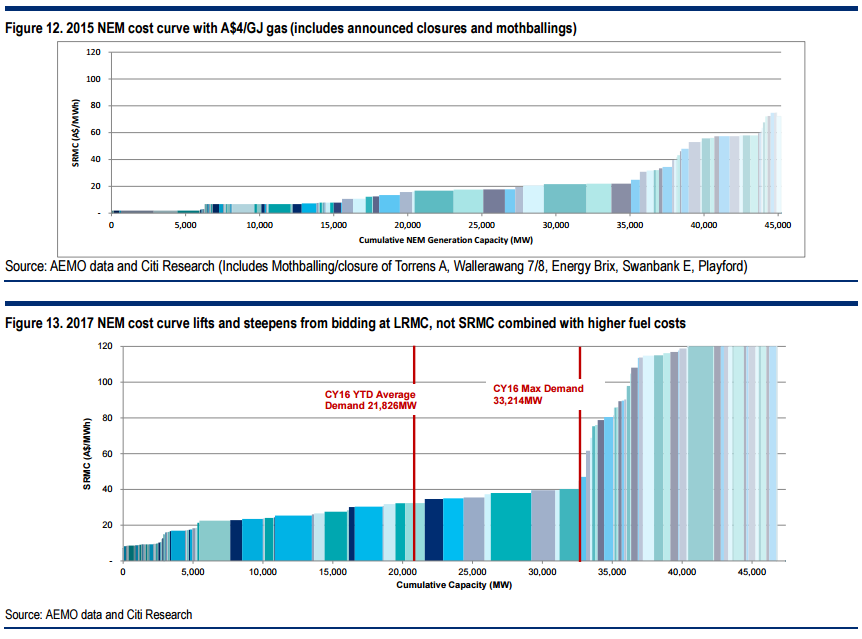

Citi today describes the problem:

Advertisement

In our base case electricity price forecasts we assume that the status quo continues, namely no change in market design or material political interference occurs beyond that already announced. We show our forecasts below in Figure 7, before discussing our assumptions of the key moving pieces on the following pages, and then the factors that could create different outcomes.

There is currently a lack of competition to provide peaking capacity due to the increased market tightness post Hazelwood closure, combined with limited gas availability for peak electricity generation capacity. In current conditions coal can bid at the cost of gas (A$100/MWh+) due to the lack of alternatives in the market to fill the Hazelwood shortfall. In particular we note: Gas is setting the price. While there is limited gas generation actually being used, the SRMC of gas (A$100-120/MWh) is setting the price. This is due to the absence of sufficient black coal fuel to easily replace lost volumes from Hazelwood and both coal and hydro bidding just under the cost of gas. In addition, Hydro running has been limited in FY17, we expect a rebound in FY18. Hydro typically bids at a similar price to gas because it offers a peaking service and looks to maximise the value of its scarce fuel (water). The additional complexity of hydro running comes from the RET scheme. Each year hydro generators have a baseline of generation to meet before they earn valuable

Gas is setting the price. While there is limited gas generation actually being used, the SRMC of gas (A$100-120/MWh) is setting the price. This is due to the absence of sufficient black coal fuel to easily replace lost volumes from Hazelwood and both coal and hydro bidding just under the cost of gas.

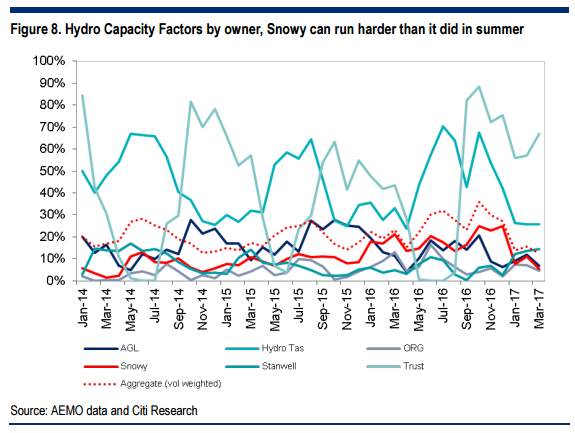

In addition, Hydro running has been limited in FY17, we expect a rebound in FY18. Hydro typically bids at a similar price to gas because it offers a peaking service and looks to maximise the value of its scarce fuel (water). The additional complexity of hydro running comes from the RET scheme. Each year hydro generators have a baseline of generation to meet before they earn valuable large scale generation certificates (LGCs). The optimal strategy is then to run hard one year to earn lots of LGCs, and in the following year limit running to rebuild water levels in dams. We think that Snowy may be pursing this strategy, otherwise it becomes hard to understand limited capacity factors over the 2017 summer when prices have been high, see Figure 8.

FY19/20: Prices ease as coal generation increases

The coal into electricity arbitrage is currently huge (~A$70/MWh), this suggests to us that at some point someone would generate harder and the arbitrage will likely narrow. The reason why this arbitrage is yet to close, in our view, is that volatile coal prices make it hard to negotiate a long term coal contract. With coal prices falling and stabilising this could allow new contracts to be signed at both ORG’s Eraring and AGL’s MacGen power stations. In addition, we believe high electricity prices would start to create a demand side response such as industrial demand loss through energy efficiency, more distributed generation and in some cases customer closures.

Long Term Price of A$65/MWh (FY21+)

Based on our analysis discussed later in this note we forecast the long term NSW electricity prices to be A$65/MWh (nominal from FY21). The key assumptions behind this are as follows:

Coal to set the floor price in off-peak periods at A$40-45/MWh

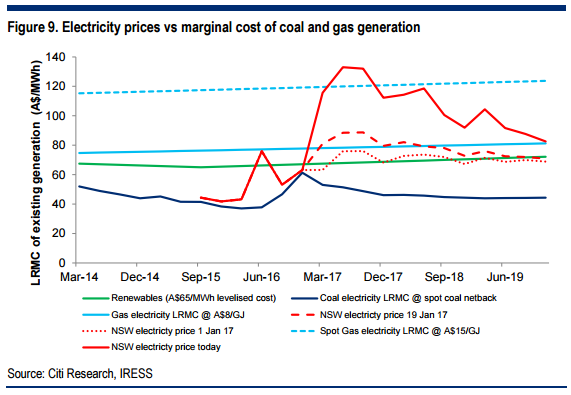

Coal closures have resulted in gas currently setting electricity prices, as demonstrated by Figure 9. This shows that NSW electricity prices have increased to levels where prices are being set based on the cost of sourcing higher cost fuel to physically support these financial contracts. We estimate the long term SRMC of coal at ~A$38/MWh and LRMC at A$45/MWh based on US$60/t 56,000Cal Newcastle export netback coal cost.

With Gas to set peak prices at A$80-100/MWh

We think in off-peak periods (i.e. Spring and Autumn), the flexibility within coal plants can be sufficient to balance the market without requiring material gas usage. However, until sufficient renewables capacity is built to move the market back to an excess supply situation, coal controlled by incumbents is likely to bid its generation against high priced gas thereby keeping peak prices at A$80-120/MWh (A$8-12/GJ delivered flexible gas). While the SRMC of hydro is <A$10/MWh it bids against gas to maximise the value of its scarce water resource.

Renewables act as long term price cap at A$65/MWh

The build out of renewables will put downward pressure on off-peak prices and increase the portion of the day under which the SRMC of coal sets the price as the market moves back to being over-supplied. We forecast the cost of renewables on a LRMC basis of ~A$65/MWh, but once built the SRMC of generation is <A$0/MWh due to the value of creating LGC certificates. The key variables determining the timing and extent of the renewables impact in our forecasts are:

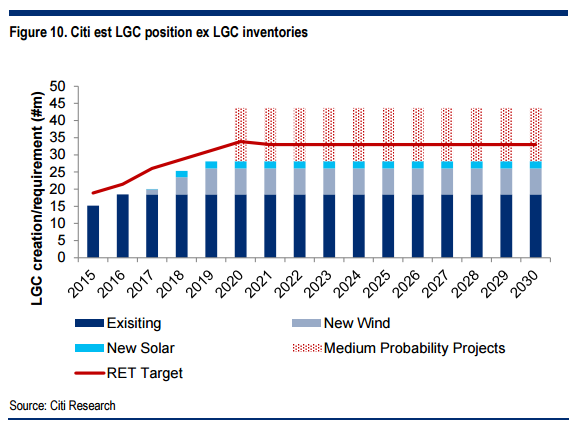

RET target likely to be met, VIC/QLD schemes to expand build out. With rising electricity prices and high LGC prices we see momentum building towards realising the Renewable Energy Target (RET) by 2020/21, see Figure 10. Beyond 2020 if the VIC/QLD 30%/50% renewable targets are pursued this would add material new generation capacity. In addition we think continued rooftop solar penetration will be incentivised by the coming increase in electricity bills. We think that renewables will require an average realised price of A$75-80/MWh to incentivise newbuild, above our average electricity price assumption due to renewables intermittency, with the A$10-15/MWh value gap filled by the price of LGCs.

More renewables, while demand is declining reduces pricing power of coal. We envision a scenario where aggregate demand falls, driven by Industrial closures/energy efficiency (Retail load flat, with average demand declines offset by population growth). With material renewables being built, this will gradually rebalance the market, and then lead to overcapacity with coal stations losing their current pricing power until the next wave of coal closures in response to weaker prices/age (mid-late 2020s).

Renewables penetration adds price volatility, but government intervention and price signals are starting to incentivize demand shifting. We have previously noted that renewables adds to price volatility, especially in in tight markets (SA the perfect example) as explored previously in our note Are the winds changing on renewables?: Defining impacts from evolution in the energy space. Both AGL and ORG benefit from more volatile prices, with ORG able to capture periods of volatility via gas fired generation, and AGL from the uplift to average prices across its coal fired baseload generation.

However, we think that the doubling/trebling of wholesale electricity prices will start to incentivize load shifting, as seen through VIC/SA large scale battery tenders, 2,400MW of proposed pumped storage, Industrial customers becoming more open to demand response, and before considering household level actions (all discussed in more detail later). This load shifting can reduce demand peaks and associated electricity price spikes/volatility.

Diversity of Renewables to have less impact on price going forward than historically in SA. The current and future phases of renewables are more geographically spread out across the NEM (reduces weather and therefore generation correlation) and across more technologies i.e. solar as well as wind. We therefore think that this will reduce the peakyness of generation and prices compared to what has been seen in SA (wind’s 25-30% discount vs average price). We do note that QLD will likely have to deal with a duck curve (see Figure 58) on a daily basis as large scale solar is added to a large quantity of rooftop solar in SE QLD.

In summary: Why A$65/MWh as a long term electricity price

We see the market gradually returning to oversupply as renewables get built and Industrial demand falls in response to high prices, periodically rebalanced by coal closures starting with Liddell in 2022. As coal loses its current pricing power, offpeak prices return to the SRMC of coal (A$40-45/MWh), peak prices continue to be set by gas (A$80-100/MWh), adding A$10-15/MWh to average prices over the year. Finally we expect a contract price premium of A$5-10/MWh above spot prices due to renewable intermittency adding cost/difficulty in providing financial hedge contracts.

In short, if we address the foundation of the problem – the gas cartel gouge – then more gas generation will open up, dropping prices and triggering renewed competition from other capacity as well.

To do that is very easy, as Credit Suisse says:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31.

Advertisement

Bada bing! Problem solved. Get on with it, Do-nothing Malcolm. Only new rules will break the cartel.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.