There seems a fixation on whether we should call the situation in the gas market a crisis or not. We can think of numerous words for it, most of which aren’t publishable within a refined institution like Credit Suisse. Whatever we call it though, we see lots of posturing, plenty of derriere covering and sadly, at the moment, no concrete evidence that suggests long term, affordable gas supply is being committed to the domestic market.

What came out (publically at least) of this week’s meeting in Canberra, between the PM and the gas suppliers, was that the ACCC will undertake (another) enquiry into the gas market for the next 3 years with 6 monthly public updates.

Also being floated is a pipeline from the West Coast to the East Coast. We struggle with this concept enormously. Dependent on the true amount of domgas from the LNG projects, if you believed that the West Coast market moved back up to a netback LNG price then adding ~A$4/GJ of transportation costs with a pipeline makes it more expensive to deliver than sending the LNG tanker around the coast.

When do we get to find out about this ‘new’ gas?

The ACCC release on the inquiry commented that “the gas industry has also revised supply and production figures which, subject to further study by AEMO, should help address projected shortfalls”.

Our natural assumption is that production figures relate to the volumes they expect to export. Given there has been, from what we have seen, no new project FID’s, no commitment of incremental capital, no step up in exploration spend and no signs of better well productivity from anyone, we can only assume that these new figures have addressed the production side of the ledger.

Perhaps there has been some “commitment” on undeveloped resources such as Arrow, Narrabri and Ironbark, or a commitment to more capital spend in producing assets, which will deliver more gas. Roll back a few years though and most of these assets were in the forecast and on paper flowing material volumes by now (or in the near future). Unless we know at what price this gas is willing to be made available, and given most new sources of gas will be 3-4 years away what happens in the interim, the conversation remains short on bankable realities.

At face value It seems that the LNG projects may have said that there’s no shortage -and hence that AEMO’s numbers are wrong – because forecast LNG exports are expected to be below contracted volumes. This may be true, but there is a difference between providing a forecast to the PM, and providing a commitment to the PM that these volumes will not increase if oil prices or LNG market conditions improve. If exports are set to be less than contracted volumes, then why not commit these volumes to the domestic market?

How much gas, for how long and for what price though?

If the sole aim of this whole process is to ensure physical supply, at any cost, for electricity generation at times of peak demand then we can all sleep easy. If anyone remotely cares about industry in Australia then we perhaps need to scratch a little bit below the surface. If there is any focus on ensuring sufficient, affordable gas for a longer duration than 12 months to industrial buyers then an awful lot more information is needed.

The construct of export parity being fine as a price is one we simply cannot subscribe to as logical. On a medium term view there is undeveloped gas that, at the well head at least, should be economic at $8-10/GJ. Whether this can be delivered to domestic users at a palatable price is a different question. However, forcing all of the domestic market to take on oil price risk, with just a view that export parity, whatever it may be, is fine seems illogical.

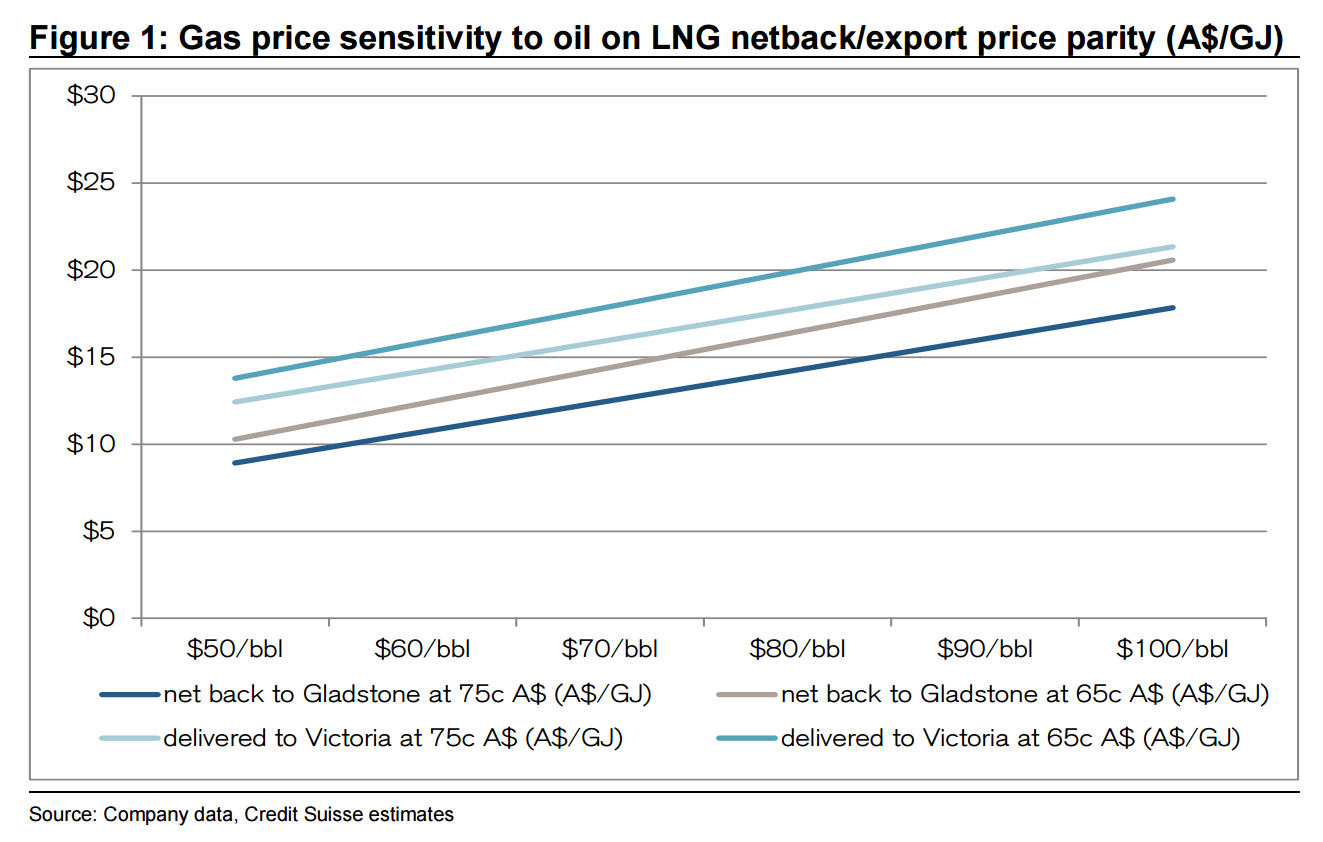

In Figure 1 we have shown the price at which we believe Shell becomes cash-flow ambivalent between selling their gas to the export market or the domestic market. These numbers are not supposed to be definitive, but we think broadly logical. To be clear on a couple of assumptions:

■ We have assumed the LNG contract is on a slope of 14x with no constant

■ We have effectively assumed that downstream cash costs are 9% of the gas price (it would largely be fuel gas), hence we take 9% of the price to get the net back to Gladstone

■ Given Shell have a take or pay to APA over their pipeline capacity, this is not a deductible cost for net back (they pay it irrespective of whether the gas is exported and have no variable opex over it). So we think Gladstone is the right “selling” point for an exporter like Shell

■ Given this all the domestic price effectively becomes a “net back plus” rather than a netback – i.e. you aren’t netting off transportation costs back to say Victoria, you are adding them on as Shell (or the other LNG projects), without intervention, would rationally look to sell at that FCF ambivalent price for them

■ We have assumed that transportation costs to Victoria from Queensland are the A$3.50/GJ that Shell have discussed publicly (we guess the ACCC will shine a spotlight on the exact numbers here)

As can be seen, even at a 75c A$/US$ and a US$70/bbl oil price, gas on this basis would be delivered to Victoria >A$15/GJ. At US$80/bbl and a 65c A$/US$ (we are not saying this should be a base case) it arrives in Victoria at ~A$20/GJ.

In no shape or form would we be subscribers to the argument that high prices are ok as it will incentivise new supply. It may well incentivise supply (although a lot of resource owners still have a lot of deleveraging to do), but given the lead times to approve and develop a new project is 4-5 years not much of domestic demand will still be alive and kicking after 5 years of these kind of gas prices.

Perhaps the ACCC can do our book build idea?

We do not want to diminish the work, or the importance, of this latest ACCC inquiry into the gas market. It will have the power to compulsorily demand information from all parts of the gas value chain.

It will certainly provide a clearly spotlight on the challenges and hold those making commitments to more accountability. As has been clear from all of their public rhetoric, the upstream producers feel it will also shine the spotlight on the supernormal profits being achieved by the pipeline operators.

The extent to which the inquiry will drive real answers and real change will, in most likelihood, depend on the questions it asks and the willingness to recommend draconian action if that supply isn’t coming.

So why would the ACCC not carry out our book build idea? Ask each producer to commit to a price, volume and duration for volumes in the coming 5-10 years. If, buts and maybes about making sure short term volumes are made available, at inflated prices, is not a resolution that industrial users can rely on for long term investment decisions.

It is hard to see how it can do any harm (and it can do a lot of good) for someone who actually has the power to ask for this information to be made available. There are a thousand nuances on delivery, level of take or pay etc that leaves a little bit of wriggle room but if someone says they can do 50PJa for 10 years at say A$9/GJ and buyers try and take them up on that offer only to be told they can only actually do 10PJa then we probably know a few porkies have been told.

The simple facts remain both perverse and painful

When taking a step back from this all, forgetting the corporate interest (something very silly for an equity analyst to say), the simple facts of the situation are both depressing and hard to explain in equal measures.

The East Coast of Australia has seen ~A$80bn and counting spent on 3 LNG projects which at US$65/bbl oil would struggle to collectively muster a 5-6% IRR (i.e. massive value destruction). They are selling gas to customers who, in most cases, don’t want it and are having to resell much of the gas for a loss into the spot LNG market. This all despite the fact that these buyers are paying ~50% less for the gas than 2-3 years ago.

Meanwhile domestic buyers, who do want the gas and can’t get volumes committed to them, are having to pay, in some instances, 3-4 times more for the gas than they were 2-3 years ago.

We often hear the pub test talked about, this certainly fails that test. In the Samter household we have the 5 year old logic test (although young Charlie Samter now says “no, dad, I am not 5 years old I am 5 and eleven twelfths) and this situation resoundingly failed that test too. It if wasn’t all so serious, it would verge on being comical.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.