By Gareth Aird, senior economist at CBA:

Key Points:

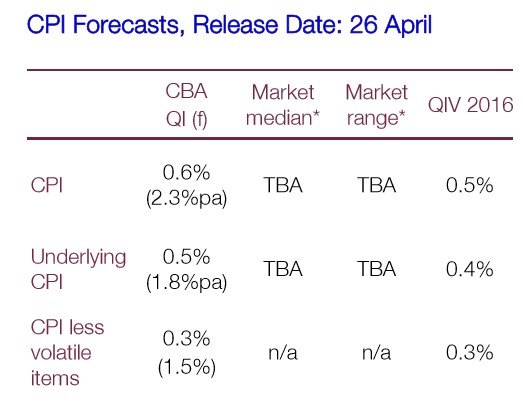

- We expect the headline CPI to rise by 0.6% in QI (2.3%pa).

- The underlying CPI on our forecasts will print at 0.5% (1.8%pa).

- Inflation outcomes in line with our forecasts are commensurate with monetary policy on hold given concerns around rapid dwelling price growth.

Overview

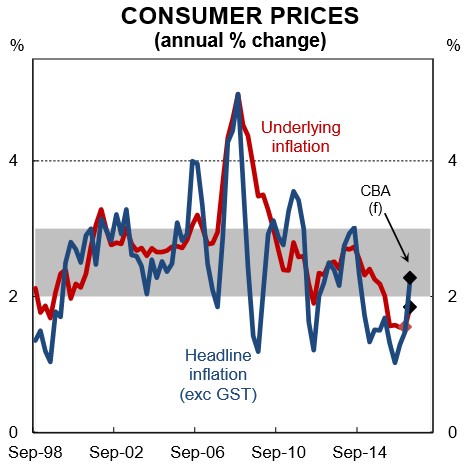

The QI CPI figures should confirm that the underlying pulse of inflation in Australia remains weak. Soft wages growth, underpinned by elevated spare capacity in the labour market, means that core inflation will once again print sub-2%pa. But headline inflation is expected to lift to within the RBA’s 2-3% target band for the first time since QIII 2014. The annual headline inflation rate looks to have hit its cyclical low point in QII 2016 at just 1.0%.

An anticipated very gradual tightening in the labour market and a lift in both domestic and global inflation expectations suggest that core inflation bottomed out in QIII 2016. That said, we don’t expect underlying inflation to pick up materially in 2017 and essentially have the annual rate of core inflation tracking sideways in a narrow 1¾-2% range throughout the year. As a result, rate rises are off the table. We think that the RBA remains on hold deep into 2018. The risk, in our view, still lies with further easing, particularly if the housing market falters.

Headline

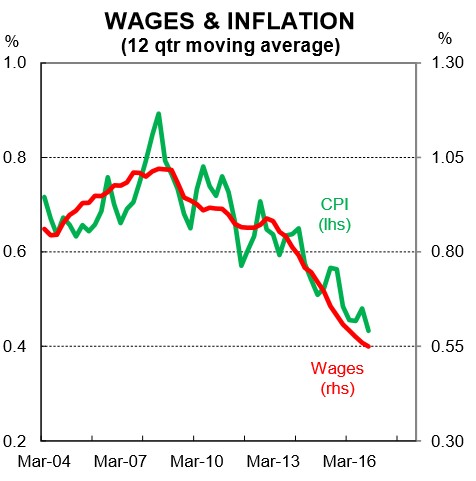

We expect the headline CPI to rise by 0.6% in the quarter after posting a 0.5% lift in QIV. On our forecasts, the annual rate of inflation would step up sharply to 2.3% because the shock 0.2% q/q fall in QI 2016 will drop out of the annual calculations. As a result, real wages growth (i.e. deflated by CPI) will turn negative.

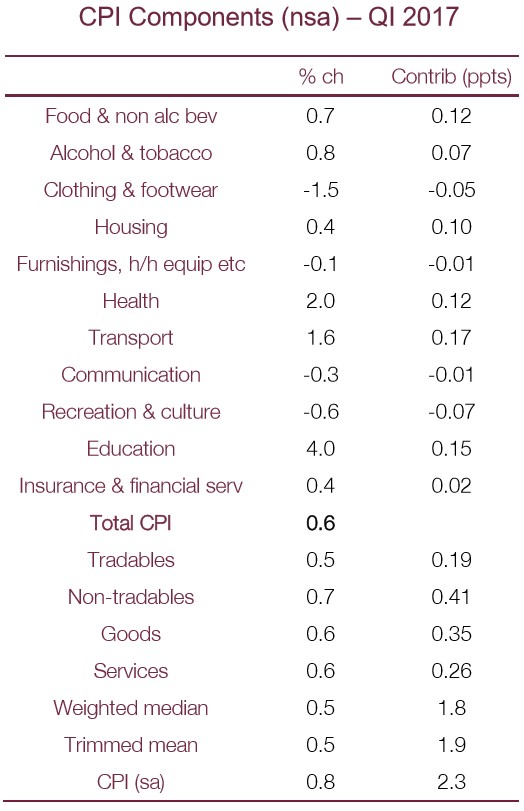

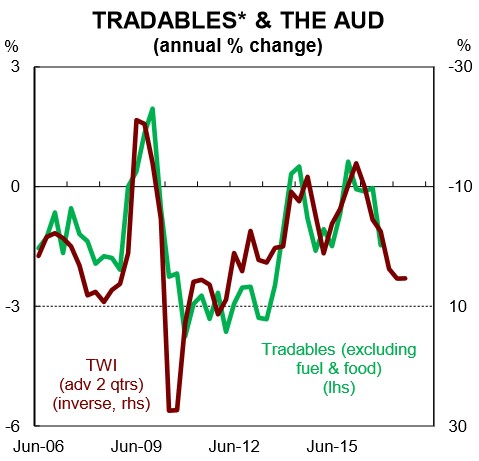

Domestically generated inflation (i.e. non-tradables) is forecast to lift by a modest 0.5%. Wages are the primary driver of non-tradables inflation and on both the WPI and AWE measures wages growth in Australia is incredibly weak. Imported inflation (i.e. tradables) is anticipated to rise by 0.7% over QI with higher petrol prices making a solid contribution to growth. Ex-fuel, tradables inflation is soft, in part because the AUD has firmed through the year (6½% higher on a TWI basis) putting downward pressure on import prices.

Cyclone Debbie will have no impact on QI CPI. Some modest upward pressure to headline QII CPI is probable (though much less than the impact of Cyclone Yasi in 2011).

Underlying

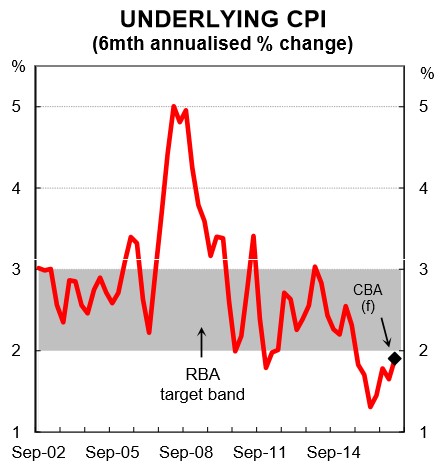

The policy-relevant underlying measures of inflation should print a little lower than the headline rate. We expect the average of the RBA’s preferred statistical measures to lift by 0.5% in QI which would push annual growth up to 1.8%. On a six-month ended basis that smooths out quarterly volatility, some figuring shows:

- an underlying CPI of 0.4%, the same as in QIV, would see rates anchored around 1.7%pa (~30bps below the bottom of the target band); and

- it would take a rise of at least 0.6% to get underlying inflation back to the bottom of the target band.

The model

A top-down modelling approach to CPI forecasting shows only a modest contribution from unit labour costs, consistent with the weak wages backdrop. The inflation restraint from the output gap continues while the AUD is putting a dampener on import price growth through the year, notwithstanding higher oil prices.

The RBA runs a Phillips curve inflation model that uses unemployment as a measure of resource utilisation. This model has overestimated inflation recently. Our re-estimation of the model using labour market underutilisation rather than unemployment improves the fit. The re-estimated RBA model points to a QI trimmed mean print of ½%, in line with our forecasts.

The detail

The volatile items that can have a large influence on headline outcomes will be a net boost on CPI growth over QI.

- Petrol prices rose by 6.0% over QI (after a 6.7% increase in QIV) and should add 0.17ppts to CPI growth.

- Fruit & veg prices rose at the wholesale level and are estimated to add a small 0.07ppts to CPI growth.

These two volatile items account for most of the gap between underlying and headline inflation forecasts.

Tobacco prices will continue to rise due to the effects of the excise increase while strength in utilities prices are expected to be partially offset by softness in rents for the housing group. The ABS will include a price index for attached dwellings in the QI CPI which will put some soft downward pressure on CPI growth at the margin.

Seasonals

We expect seasonally large increases in health (particularly pharmaceuticals), and education and childcare (annual fees). Holiday travel and accommodation costs typically fall over QI. And post-Christmas sales normally mean seasonally low outcomes for clothing and a range of consumer durables.

We have the seasonally adjusted CPI rising by 0.8% in QI so seasonal price moves should have a negative influence on headline inflation.

QI 2016 & the risks

It’s worth keeping in mind that the QI 2016 CPI shocked significantly to the downside. The headline CPI fell by 0.2% q/q and underlying inflation printed at just +0.2% q/q. The RBA responded by cutting the cash rate a few weeks later. The result was attributable to not just lower petrol prices, but broad-based discounting by retailers and softer-than-usual price rises for the seasonal components. Health and education, for example, had relatively low QI rises (1.9% and 3.1% respectively).

On balance, the risks to our call are to the downside given falling wages growth and persistent discounting in the retail sector.

Monetary policy implications

If QI CPI prints in line with our expectations then a rate cut is off the table in May. Very strong dwelling price growth and growing concerns around the level of household debt mean that the cash rate is unlikely go lower unless there is a sustained loss of momentum in job creation and/or dwelling prices fall materially. Neither outcome is in our central scenario and as such, we see the RBA on hold over 2017 and well into 2018.