The Australian understands that after the Coalition’s decision to rule out an emissions intensity scheme, which puts a price on carbon in the electricity market to encourage investment in renewables, the government is warming to an alternative market signal that would put in place a 50-year rule for Australia’s fleet of coal-fired power stations.

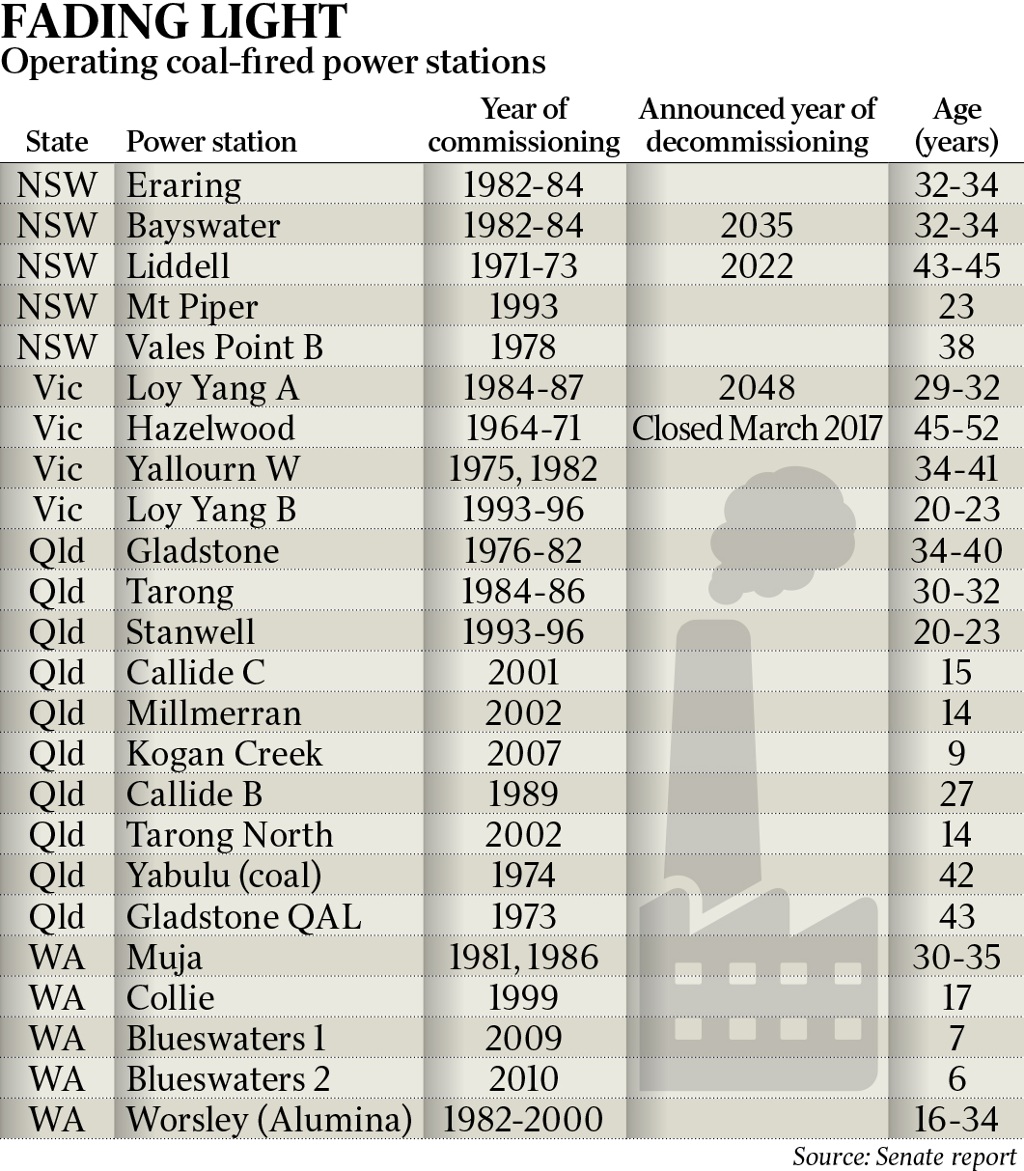

This would prevent the need for multiple closures of coal-fired generators in the Latrobe Valley, where emissions from brown coal are highest, while also ensuring the transition to higher renewables does not lead to instability in the grid. A new 50-year rule based on a coal-fired power station’s “end of technical life” would be coupled with a new national interest test three years before the scheduled shutdown to give the government the option of extending the plant’s lifetime.

A 50-year rule would either dictate that coal-fired power stations have to modernise or close their operations after 50 years or else set a cap on the emissions a power station could generate based on an expected 50-year lifespan, creating an incentive for it to improve its carbon efficiency.

The fifty year rule is an anti-carbon price. It will offer an invisible shield for coal-powered generators against having to any install any carbon capture technology for the life of the plant until it can die of old age. The three year notice on closures is simply a trigger for government to pour tax-payer’s money down the coal drain. The irony is that Canada’s 50 year rule is designed to close coal-fired power. Instead, here, it will keep it open.

Domainfax continues its post-journalism reliance on rent-seekers to provide coverage of the issue at all as AGL’s Andy Vesey goes the gouge:

Advertisement

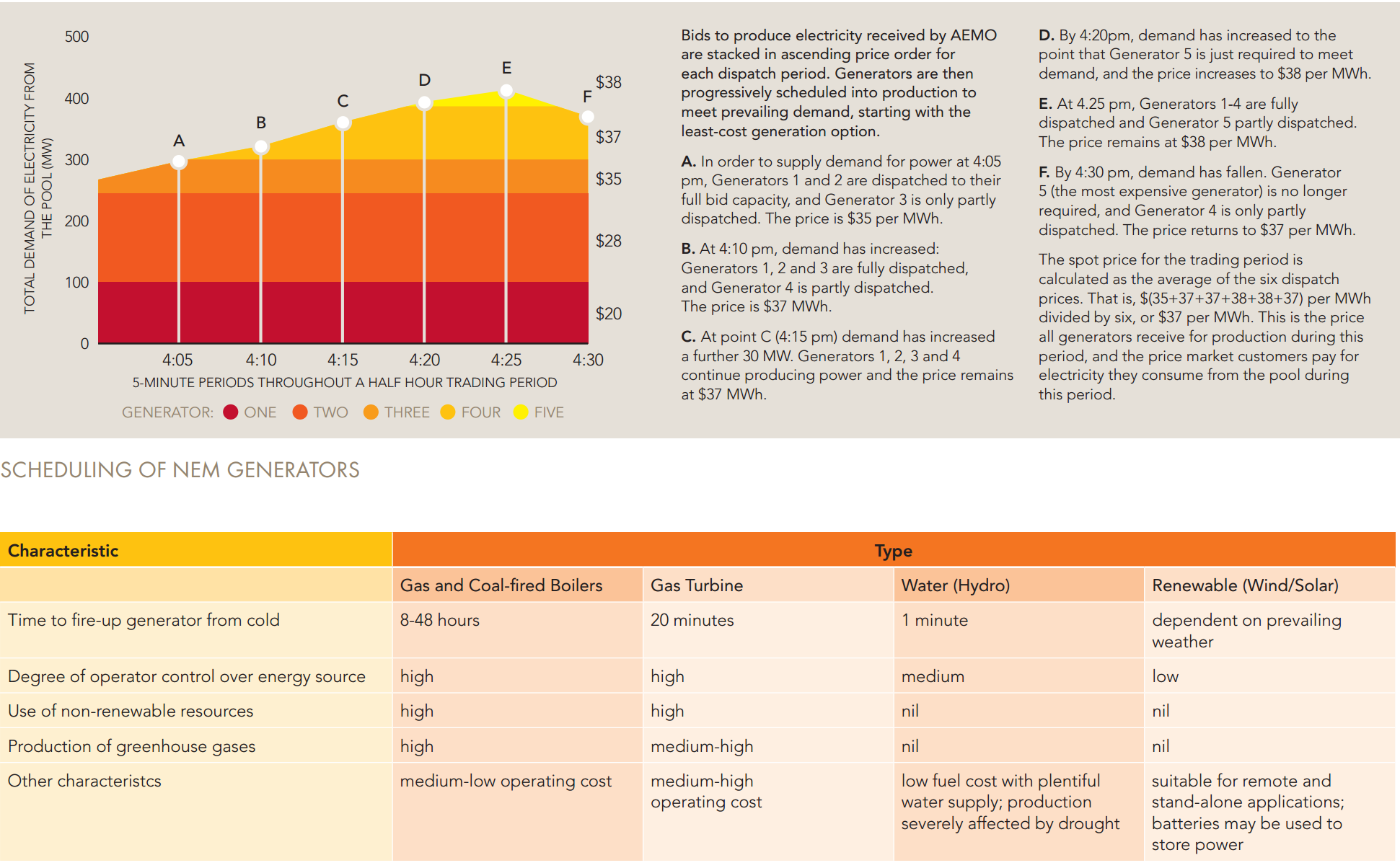

Our problem today is not technology or cost, it is the lack of integration of our policies to introduce renewables and the design of our energy markets. This issue can be corrected by requiring renewable generation to offer “firm” energy supply – through partnering with storage or conventional generation. This way renewable generators can become full participants in the energy market and contribute to more competition and better outcomes for consumers in the retail market.

The closure of Hazelwood power station in Victoria with only five months’ notice highlights another design flaw. It takes many years to plan, finance, approve and build a new power station. Yet the energy market only had limited notice that Hazelwood would close. As a result, the impact on pricing in the market has been dramatic.

To address this the government should consider a critical intervention, that is, a notification requirement, at least three years in advance of the closure of major power stations. Telegraphing closure years in advance will enable the necessary investment to come forward with confidence.

For example, an age-based rule may apply (similar to what is implemented in Canada) where power stations are required to close after 50 years, unless they convert to new low carbon technology.

Hazelwood has not caused the power price spikes. Coal is not even the issue. Renewables are not the issue, either. It’s gas that’s the problem. AGL doesn’t want it fixed because while gas elevates the electricity price traditional thermal generators are creaming it.

It’s gas that sets the marginal cost of electricity in the National Electricity Market (NEM) not coal nor renewables, owing to where it sits in the wholesale electricity market bid stack. See Australian Energy Market Operator description below:

Advertisement

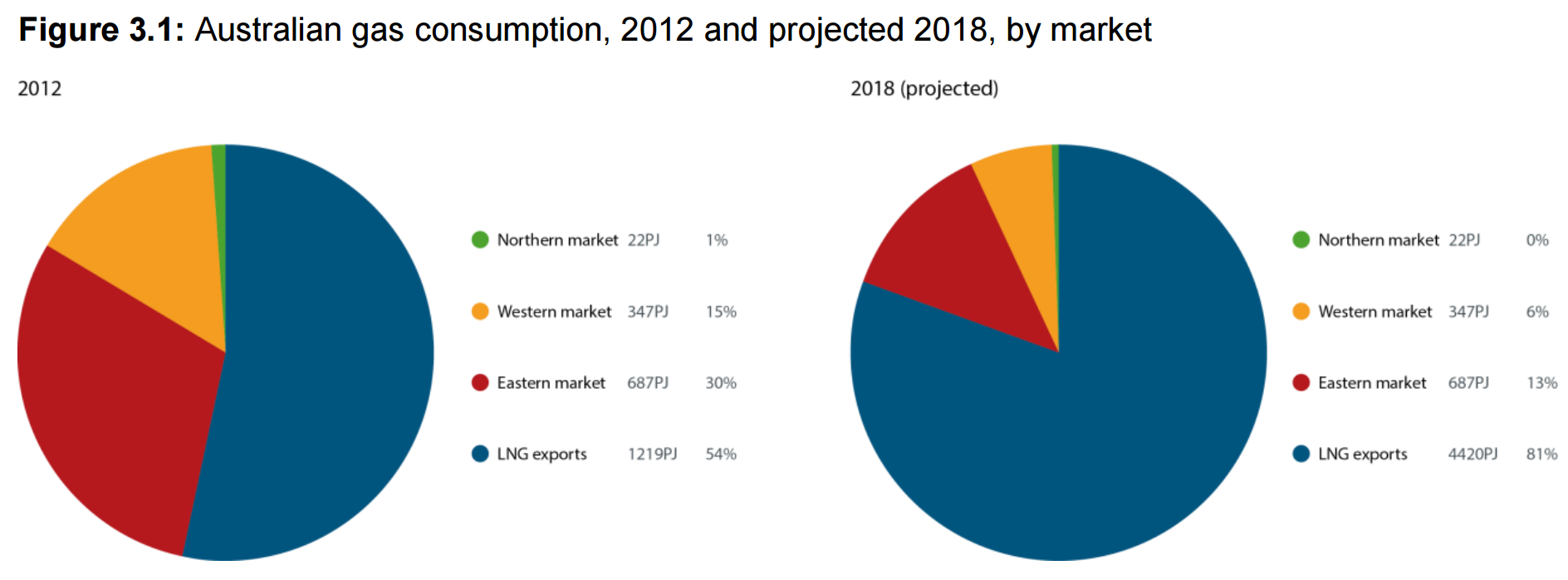

The gas price has been spiked by the huge export white elephants on QLD’s Curtis Island. All told, Australia is about export 80% of its gas output:

Advertisement

And we’ve left ourselves 200Pj short domestically to power our energy transition. The gas price has thus launched and dragged electricity prices up with it.

The answer is not to marry coal, which will do nothing to lower electricity prices, as Credit Suisse has argued, the cheapest and quickest solution is to bring down the price of gas:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31.

Advertisement

Banning third party exports of gas will instantly free it up for domestic use. By next year it will only be 3.6% of total exports that we’ve held back. But that will be enough to fire up idled gas power plants and drop electricity prices.

We need cheaper gas and stable carbon pricing policy. Then all of the problems will go away at once and we’ll have time to decarbonise the network with longer term battery and other storage options to stabilise renewables. This was always the national plan, such as it was, that gas would be the transitional fuel as we move steadily from coal power to renewables.

This debate is now being sucked deeper and deeper into the giant Australian rent-seeking vortex from which good policy rarely returns.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.