For an inflation-targeting central bank, wages growth matters. Indeed, the two key empirical models that the RBA uses for forecasting inflation both have wages and the labour market as key inputs. The first is a ‘Phillips’ curve’ model, which suggests that as the unemployment rate falls, and spare capacity in the labour market is reduced, wages and inflation rise, as workers are able to demand greater pay. Second is the ‘mark-up’ model which suggests that prices are set as a mark-up over costs. In this model, unit labour costs (productivity-adjusted wages growth) are a key input.

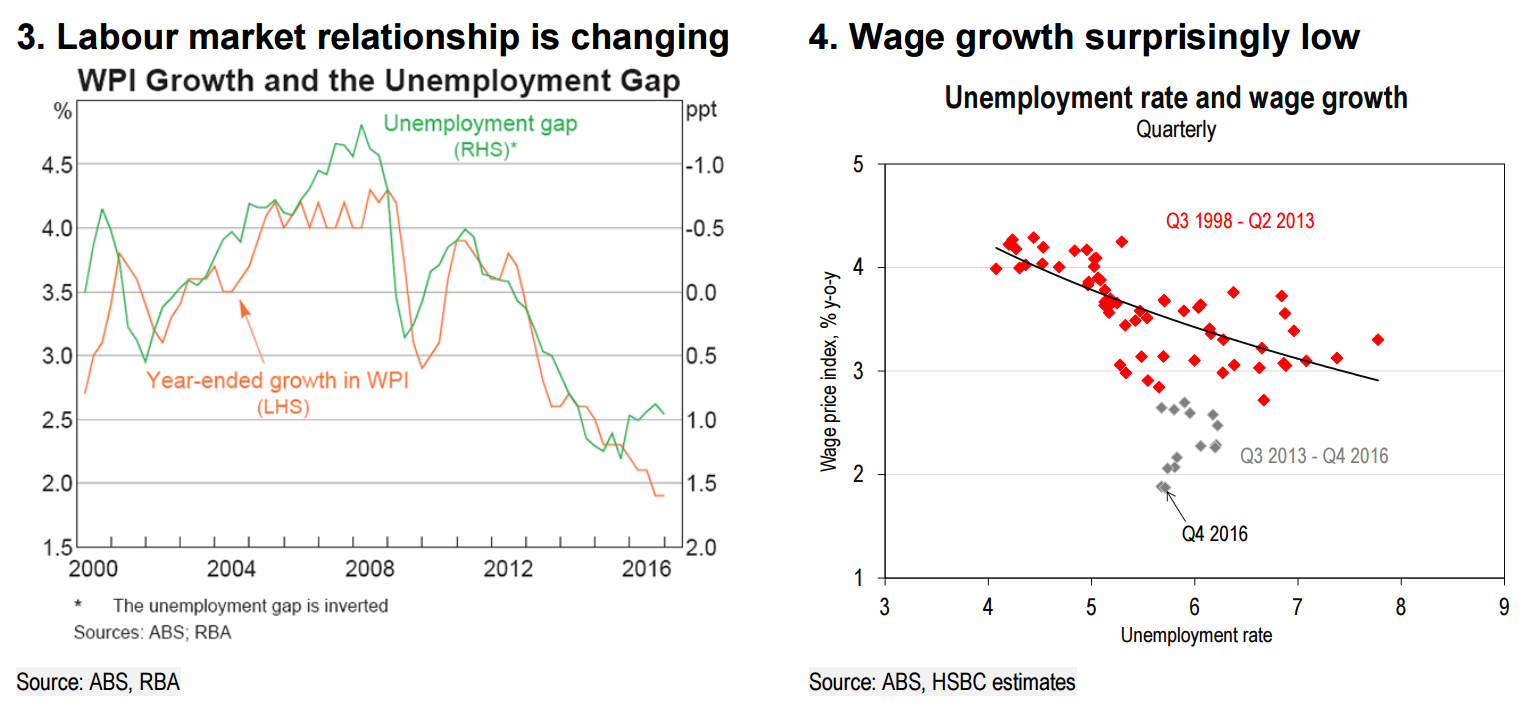

However, structural change in the labour market and measurement issues are making these relationships more complicated. In particular, the measures of wages growth, which are at their lowest levels in multiple decades, are much lower than the historical relationship with the unemployment rate would imply.

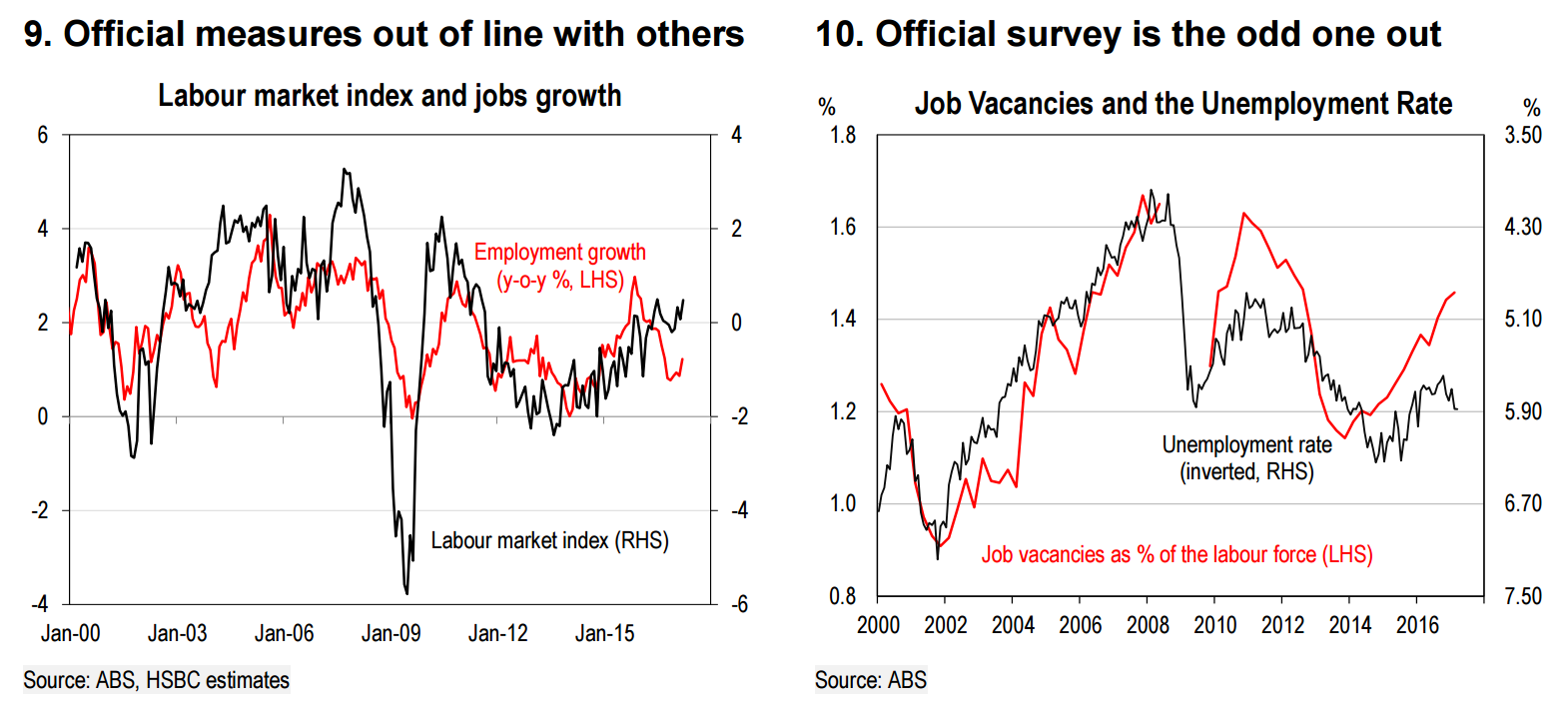

There are many possible explanations. It could reflect underemployment, with the broader measures of spare capacity less positive than the headline unemployment rate. This could reflect a shift to more part-time jobs, reducing the bargaining power of workers. It could be the result of technology, globalisation and structural factors, which are making it harder for workers to demand wage rises. Another factor may be that the very large cycle in commodity prices and national income in recent years has affected wage settings. Importantly, measurement issues in the official labour market statistics have been further complicating any assessment. Job vacancy, job advertisements and business surveys all show stronger labour market conditions than the official statistics.

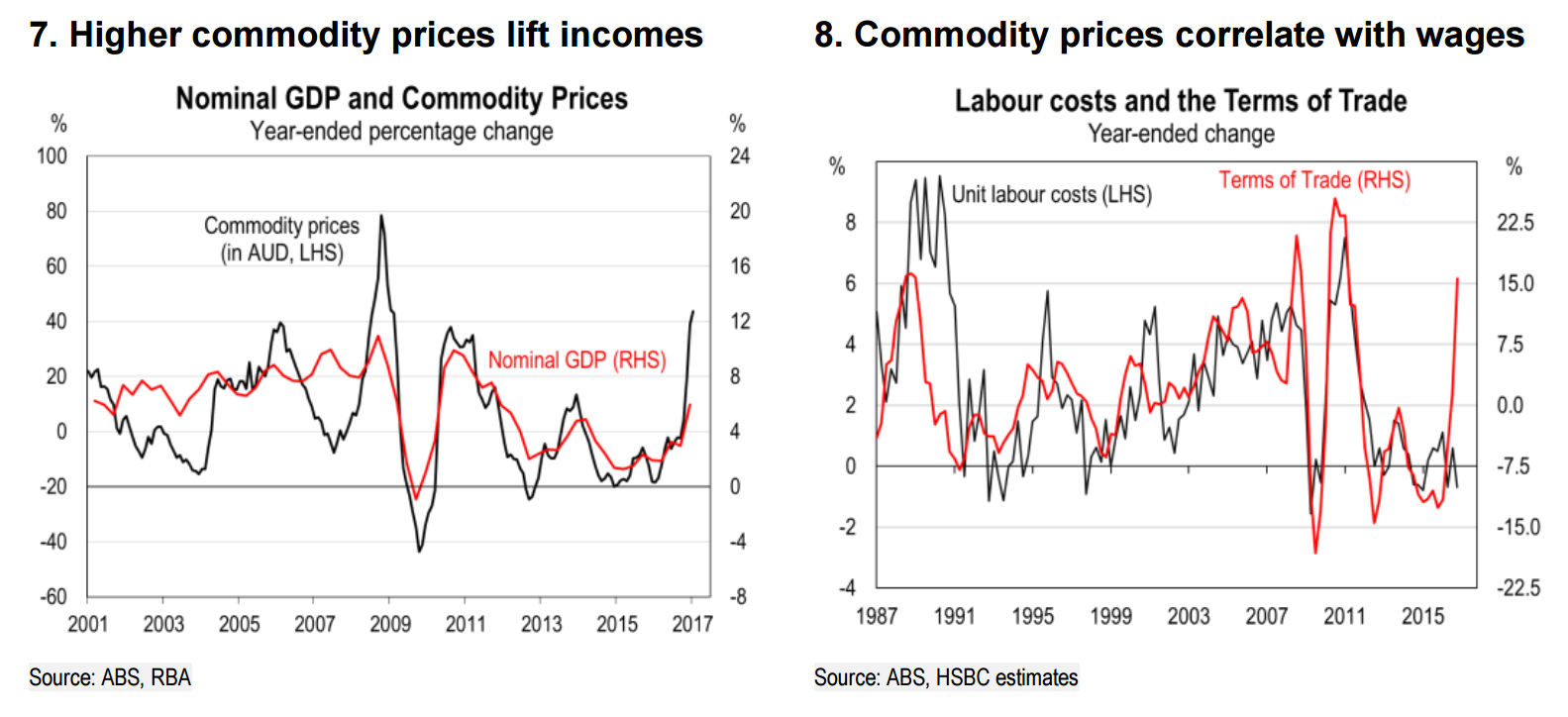

We see the RBA as unlikely to cut interest rates any further, given concerns about the housing price and credit boom in Sydney and Melbourne. With no cuts likely, the key question is: When might the RBA start to lift the cash rate? For this to happen we believe the central bank would need to be convinced that wages growth is picking up. There is considerable uncertainty about when this will happen. However, our view is that the recent lift in commodity prices, and the boost it has delivered to national income, should deliver some support for wages growth. History shows a strong positive correlation between Australia’s wages growth and commodity prices.

As I said yesterday, there’s really no point in any of this if you’re not focused 100% upon the ferrous market. So long as we have no productivity to speak of, it is all that matters to income. The terms of trade (ToT) is collapsing before our very eyes so why put out a report arguing it’s about to trigger wage and rate hikes? Bloody daft!

Once coking coal collapses in the next month, the ToT will be down an astonishing 20% in the quarter, roughly flat year on year. Then there’ll be more bulk bleeding over Q3-4 as China slows (not crashes) and the ferrous bubble is worked off and new lows for the terms of trade shifting into 2018.

Still, the report contains some good stuff on the labour market so is worth a glance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.