Via UBS on the relative uselessness of the NAB survey right now:

Mar biz conditions rebound to booming ~decade high +14.2 (after +9.3)

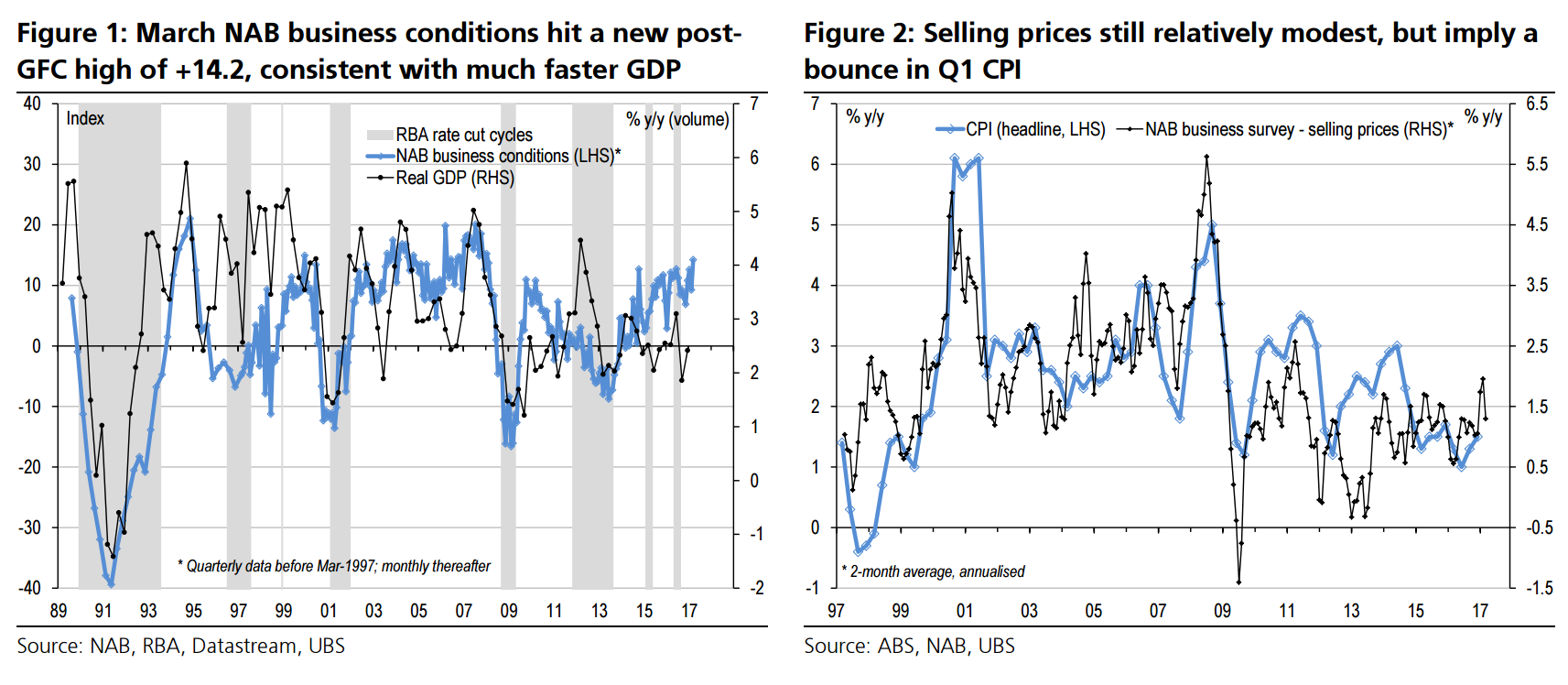

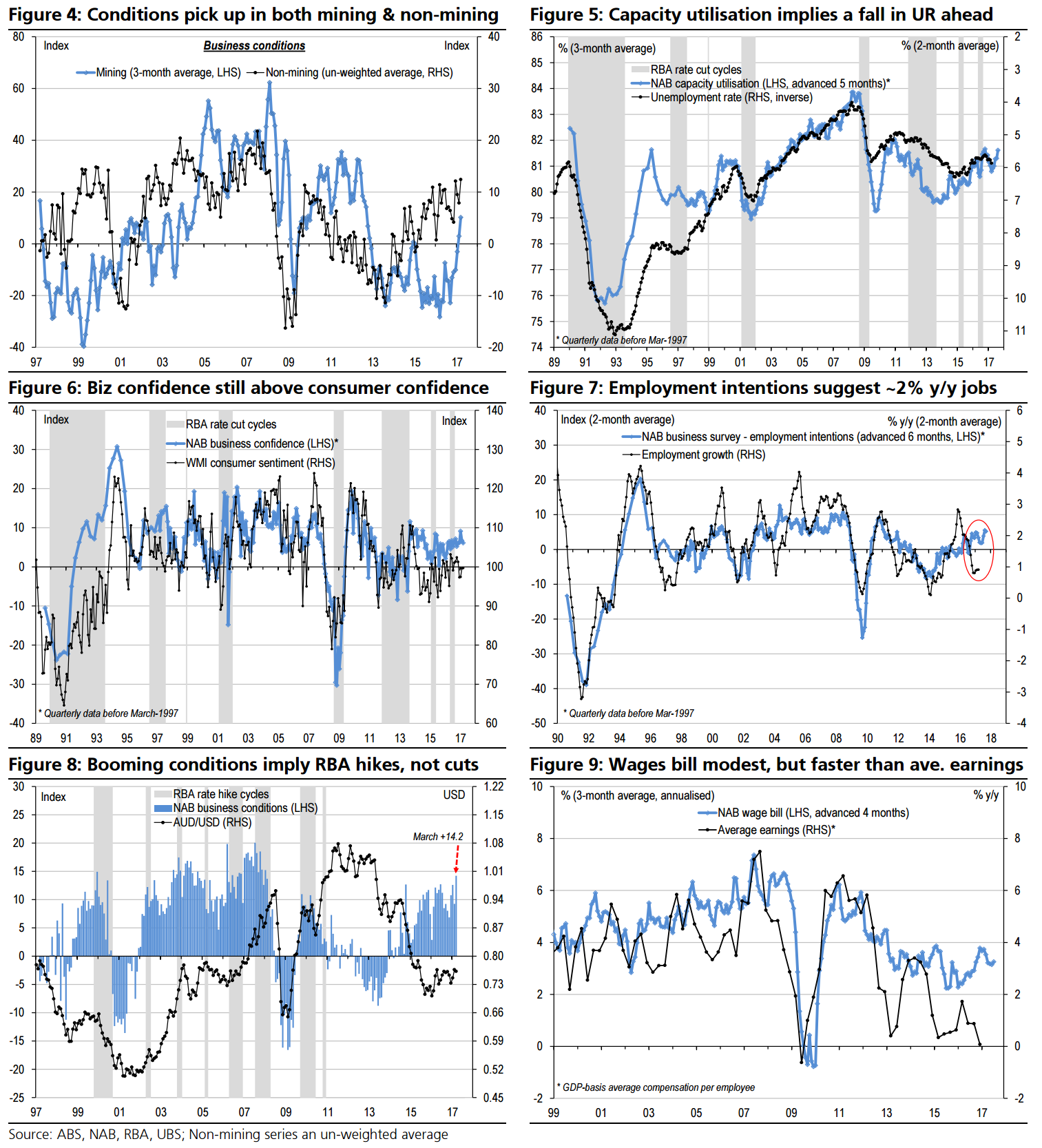

NAB’s survey of business conditions rebounded sharply in Mar-17 to a booming level of +14.2 (UBS: ‘steady’, mkt: nf), the highest since the GFC started to hit in early 2008 (after +9.3 in Feb-17). Conditions remain well above average (+5.0 since 1997). By industry, mining spiked again (+18, after +11) following the surge of commodity prices over the last year; but non-mining (un-weighted average) also jumped to a near decade high (+12.4, after +7.9), to now be well above average and its prior trend.

Employment intentions were ~unchanged m/m, but remain positive, and consistent with faster jobs growth (closer to ~2% y/y). Capacity utilisation edged up to marginally above average. This contrasts the recent spike in unemployment. Importantly, selling prices remain within their prior modest range, albeit the trend is broadly consistent with our forecast for higher Q1 headline CPI. The wages bill remained relatively subdued, consistent with our view of low inflation feeding into weak wages (albeit GDP-basis average earnings are already noticeably weaker around flat).

Business confidence relatively ~steady at +6.1, holding around average

Elsewhere, business confidence remained relatively more stable at +6.1 in Mar-17 (UBS: ‘steady’, mkt: nf, pre: +6.7), still holding around average (+5.8 since 1997).

Implications: biz conditions in RBA hike territory, but hard data needs to follow

Overall, NAB’s business survey showed another spike of business conditions in March, with the ~decade high level (and rising trend across recent months) suggesting a much better GDP growth outlook ahead. Hence, business conditions are arguably in RBA rate hike territory (see Figure 8). However, as Figure 1 shows, the ‘soft data’ of business conditions have been average or above for the last 2 years, yet the ‘hard data’ of real GDP growth has been stuck trending around a relatively moderate 2½% y/y. Indeed, much better reported business conditions have also yet to translate into inflation indicators to the same extent, and hence we still see the RBA on hold ahead.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.