From late 2011, MB warned the RBA and Treasury against its wrong-headed plan to catapult the Australian economy over the mining bust by blowing a new housing bubble. One of the reasons for our caution was the fear that authorities may be forced to tighten into the bubble before the mining bust was over, and so it is proving to be.

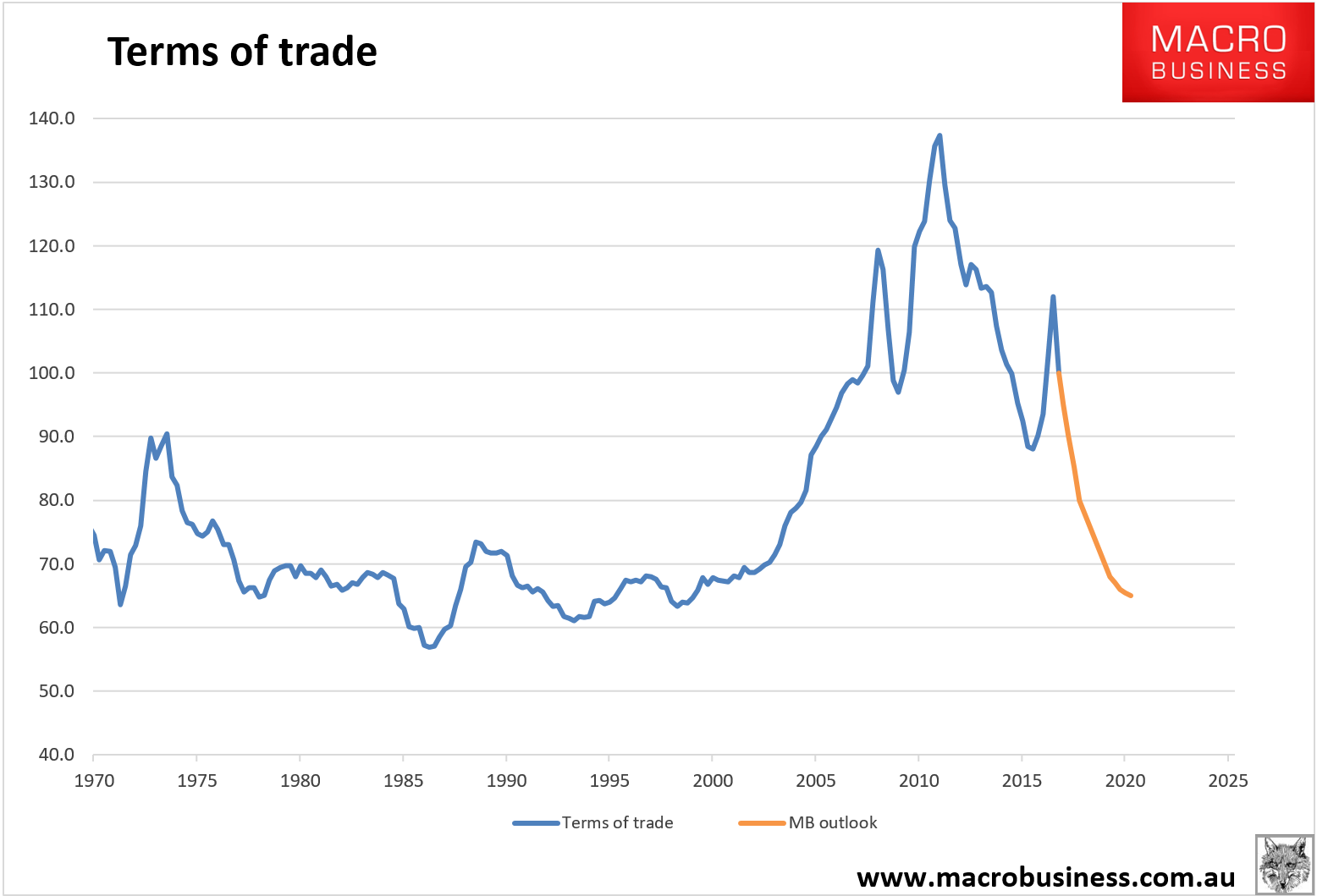

While most media and forecasters are busy mulling rate hikes following macroprudential to contain the housing bubble, the resurgent terms of trade shock is building into monstrous proportions. Iron ore is now down one third from its highs and, although coking coal has rebounded temporarily on Cyclone Debbie, it will halve again soon and then keep falling. By year end I expect to see iron ore at new lows in its great correction and coking coal at $100 or lower. As this flows through to contract prices, within a year Australia’s terms of trade will fall by 25-30% and be at new correction lows as well:

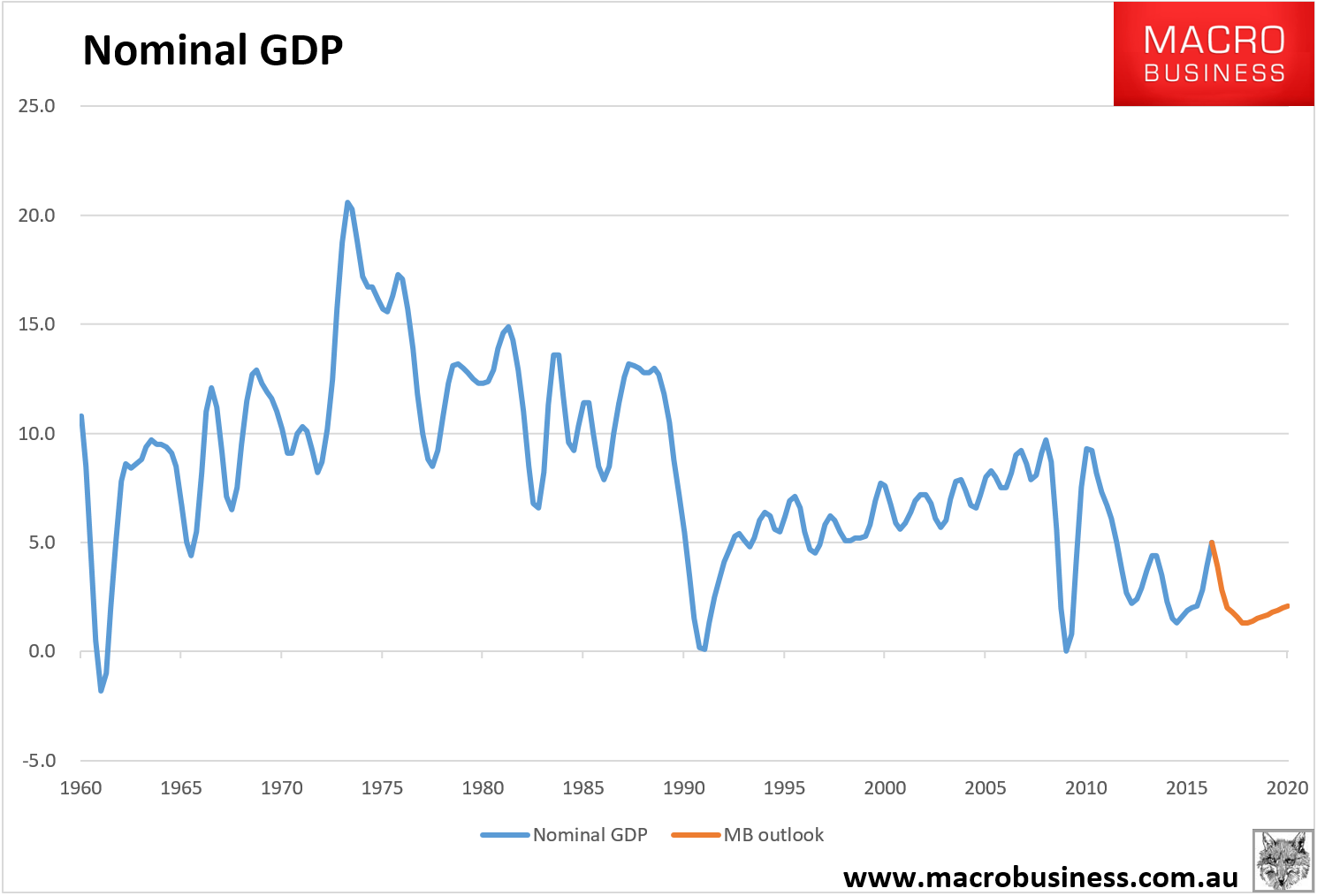

Nominal growth will plunge again: