ACCC: Energy crisis enters “worst-case scenario”

Via The Australian:

Australian Competition & Consumer Commission chairman Rod Sims said yesterday the situation in the east-coast gas market had deteriorated in the past year, leaving businesses faced with a “worst-case scenario’’.

Mr Sims told The Australian the study commissioned by Malcolm Turnbull this week, after the gas industry failed to offer its own solution to tight markets, was as important as any the ACCC had undertaken.

“We think there is a crisis in the gas market, particularly in relation to industry that needs gas, either as a feedstock or a source of energy,” Mr Sims said. “I do think companies will go out of business because of this and I think that will be a crying shame.”

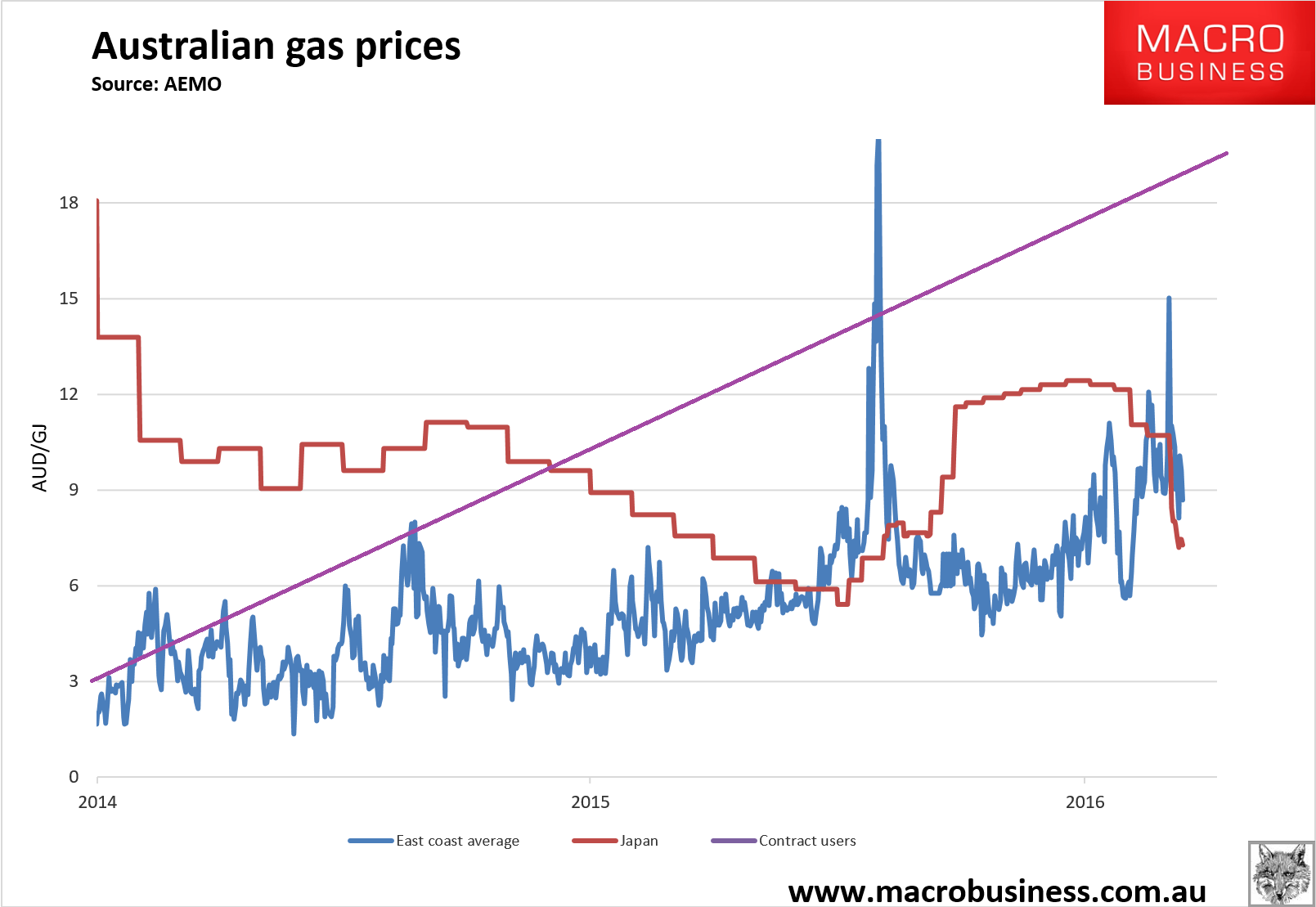

Domestic gas prices have leapt fourfold in some cases as $80 billion of liquefied natural gas export plants at Gladstone ramp up, rapidly tripling demand in the pipeline-connected east-coast states without providing enough new gas supply to feed them.

“We thought the market was going to get tight but this is worse than we expected,” Mr Sims said. “This is sort of the worst-case scenario.”

Mr Sims said the ACCC’s special powers would be needed to find out whether gas exporters were making good on pledges to support reasonably priced domestic supply. “The only way you can determine whether that is happening is if we are in there with our confidential information-gathering powers making sure that it happens,” he said. “This is as important as any study as we’ve ever been asked to do.”

He said the inquiry in itself was likely to help promote more supply, as occurred during the last one. “The fact they could see we were watching and could look at their documents, meant that more gas was available,” he said. “I except that will happen again.”

More from Matthew Stevens:

We asked Sims what a reasonable price for domestically contracted gas might be. He thought that an interesting question but suggested that, for want of any more specific guidance from government, then export parity pricing “is an appropriate starting point”.

Conveniently enough the Santos quarterly that was released just hours before our chat announced what that starting point might be right now. Santos earned an average $US7.09mmBTU for its LNG sales through the March quarter. That translates roughly to about $10.70 a gigajoule of gas. And that is nothing like the price that big gas users are paying for contracted gas.

…”Back in 2015 we took a snapshot of the market that meant, at a single point in time, we had a deeply informed view of the state and conduct of the market,” said Sims. “As I said, we found that gas demand really was not being met. Just in taking a look at the market we found that behaviour improved.

“What we will be in a position to do for the next three years is build a richer and evolving set of data and then find a routine way of announcing our findings to the market. We will be able to show in great detail if there is a problem. It will then be in the government’s hands to work out whether there needs to be a structural response to what we find.

“Then the second big piece here is that we have been told to work with Mike [Vertigan] once we get under way so that when we finish in three years we will be in a position to help define the automatic mechanism needed to keep the market transparent and informed,

“I am very excited,” Sims finished. Doubtless not everyone in the gas industry will be quite so enthused.

Why should they be? In three years many will be out of business. We already know the price gouge is happening:

To reach export net-back we’ll need to see prices fall from $15-20Gj to $8Gj.

And how is that going to happen when this is?:

The Santos-led Gladstone LNG export plant is buying more than half its gas from third parties, rather than producing from its own coal seam gas fields, despite lifting its own production in the March quarter, Santos has revealed.

In its first quarter report, Santos said GLNG, in which Santos has a 30 per cent stake, produced only 43 per cent of the 1.4 million tonnes of LNG exported from Gladstone during the quarter from its own fields.

But, thanks to a boost in production from GLNG’s Queensland coal seam gas fields, this is more than in the December quarter, when GLNG provided just 38 per cent of its own gas.

It is the first time Santos has clearly broken out third-party gas volumes for GLNG, whose market purchases for export are in the spotlight as east coast gas markets tighten and prices rise.

Versus what it said during development:

“You’ve got to be absolutely confident when you sanction trains that you’ve got the full gas supply to meet your contractual obligations that you’ve signed out with the buyers,” Mr Knox told investors in August 2010 when asked why the plan was to sanction just one train first up.

“In order to do it (approve the second train) we need to have absolute confidence ourselves that we’ve got all the molecules in order to fill that second train.”

But in the months ahead, things changed. In January, 2011, the Peter Coates-chaired Santos board approved a $US16 billion plan to go ahead with two LNG trains from the beginning….as a result of the decision and a series of other factors, GLNG last quarter had to buy more than half the gas it exported from other parties.

…In hindsight, assumptions that gave Santos confidence it could find the gas to support two LNG trains, and which were gradually revealed to investors as the project progressed, look more like leaps of faith.

…When GLNG was approved as a two-train project, Mr Knox assuredly answered questions about gas reserves.

“We have plenty of gas,” he told investors. “We have the reserves we require, which is why we’ve not been participating in acquisitions in Queensland of late — we have the reserves, we’re very confident of that.”

And the obvious solution, via Credit Suisse:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31.

The ACCC inquiry is a fig leaf for the gas gouge to proceed unhindered.