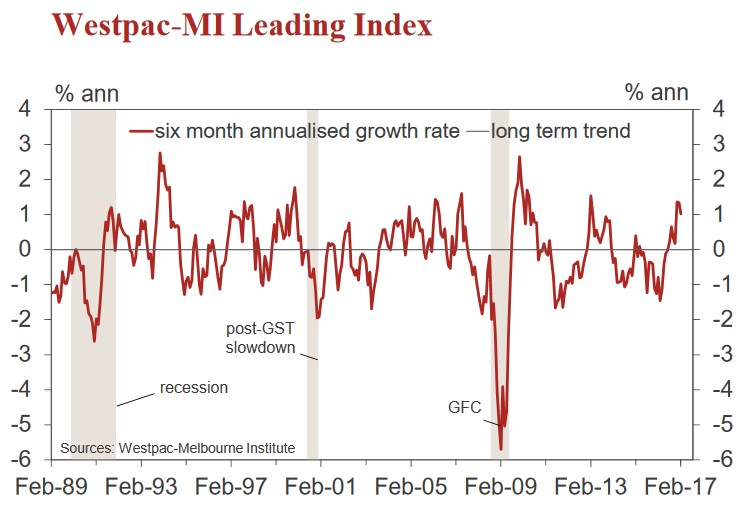

The six month annualised growth rate in the Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, fell from 1.34% in January to 1.02% in February.

The Leading Index continues to point to above trend growth momentum, albeit with the pace moderating since the start of the year.

February marks the seventh consecutive month where the growth rate in the Index has been at or above trend. This follows fifteen consecutive months where the growth rate had been below trend. That earlier period of weak reads foreshadowed the softer economic conditions through the middle of 2016. The improved momentum in the Index since then is also now evident in the economic data with the December quarter national accounts confirming a solid 1.1% rebound in GDP from a 0.5% contraction in the September quarter.

The latest reads point to above trend momentum carrying through the middle of2017 consistent with Westpac’s forecast for 3% growth for the full year.

The Leading Index growth rate has lifted over the last six months from 0.22% in August to the current 1.02%. The main components driving the improvement have been: commodity prices, in AUD terms (+0.74ppts); the yield spread (+0.46ppts); and a reduced drag from hours worked (+0.17ppts).

These have been partially offset by an increased drag from: dwelling approvals (–0.4ppts) and weaker reads from the S&P/ASX 200 (–0.17ppts); and the Westpac-MI UE index (–0.12ppts).

The component breakdown does provide something of a warning about the extent to which current above trend momentum can be sustained. So far the bulk of the uplift is coming from two external factors: commodity prices and the yield spread (the latter being driven by the rise in long term bond rates globally).

The pulse from commodity price gains is already starting to dissipate and may turn negative if prices retrace. Similarly, the big moves in the yield spread have probably been and gone. Meanwhile other components are showing less convincing momentum.

The Reserve Bank Board meets on April 4. Yesterday’s minutes for the March meeting were a little more downbeat. Although the central view is still constructive on global and local growth prospects, the commentary placed more emphasis on weaknesses in labour markets and household incomes, tending to downplay the potential boosts from rising commodity prices. The commentary also sounded a touch more urgent around risks in the housing market.

On balance, the commentary points to interest rates remaining firmly on hold, the Bank possibly mulling other policy measures to manage risks in the housing market. Westpac expects the cash rate to remain on hold throughout 2017 and 2018.