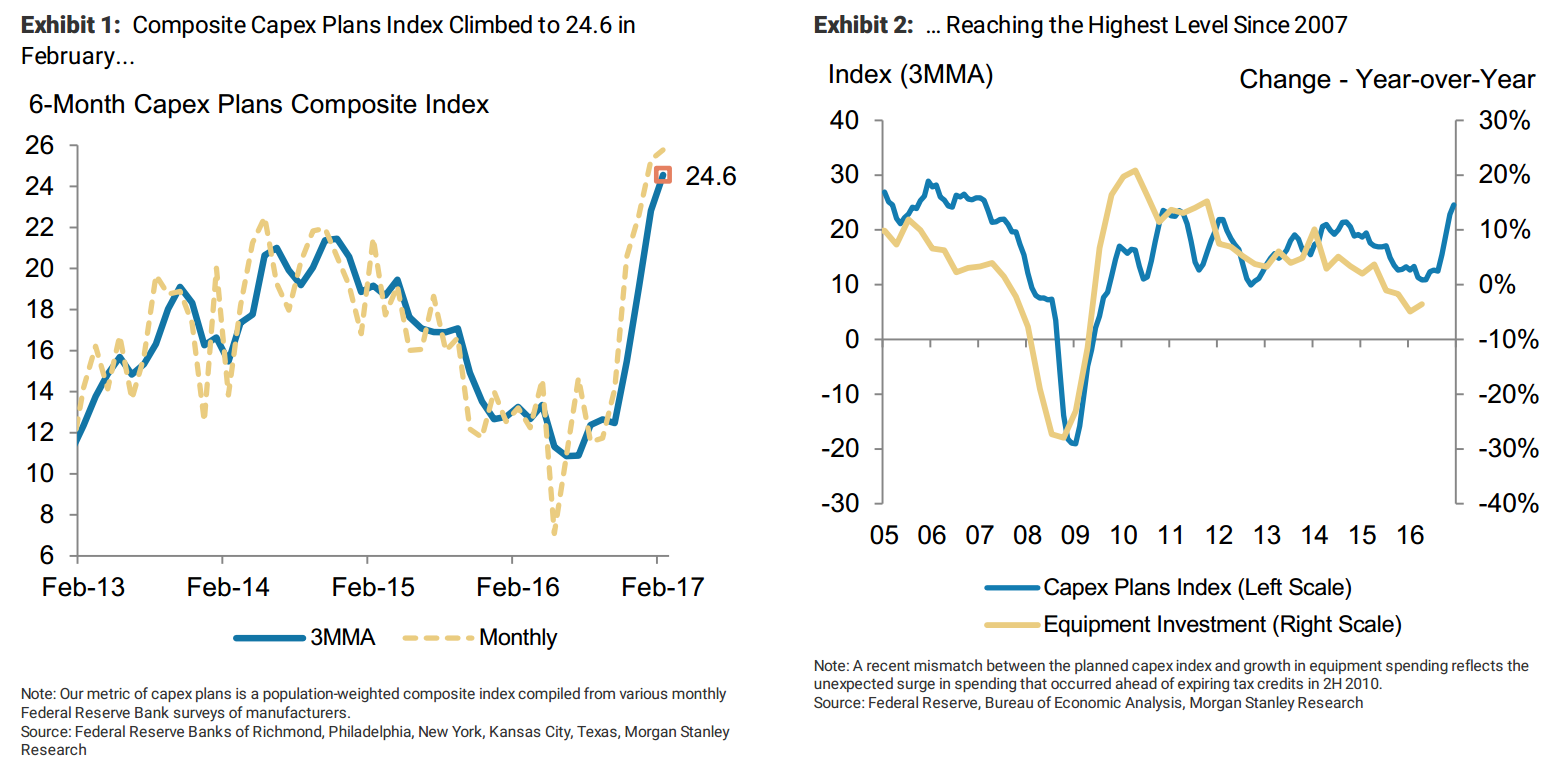

Our composite Capex Plans Index posted its fourth consecutive gain in February, climbing 1.7 points to 24.6—a post-recession high. While the recent surge in our index is promising, actual capital spending will depend largely on the evolving outlook for fiscal and regulatory policy.

Our composite Capex Plans Indexgained ground for thefourth consecutive month, climbing 1.7 points to reading of 24.6 in February—a high since 2007. Between October and February, the indexhas gained 12.1 points, representing the largest four-month gain since 2011 and matching a post-election surge in a range of business and consumer sentiment surveys (Exhibit 1).

While the recent performance of the index supports a brighter outlook for equipment investment through mid-year, comments from the regional Federal Reserve Bank surveys suggest that actual spending will depend largely on theevolving outlook for fiscal and regulatory policy.

For now,growth in equipment investment appears to be recovering, posting its first positive Q/Q reading in 4Q16 after four consecutive declines and on track for another gain in Q1 based on our current tracking (see Treasury Market Commentary:2/27). The Capex Plans Index is a three-month moving average of a population-weighted composite compiled from monthly regional Federal Reserve Bank surveys measuring 6- month capex plans and tends to lead growth in equipment investment by about 3 months (Exhibit 2). The more volatile monthly capex plans index increased 0.5 points to 25.8.

Growth was a bit lopsided in February—planned capital spendingincreased in two out of thefiveFederal Reserve Districts that compose our index. The largest gain was reported by the Kansas City Fed, which showed an 8-point jump on top of a 10-point increase in January. Capex plans were roughly steady in the Dallas, Philadelphia and Richmond Fed Districts, changing by 1, 0 and -1 points, respectively, while the New York Fed district reported a 3-point decline. Overall,gains in capex plans appear to be leveling off after having surged in November or December.

With monthly gains in capex plans leveling off, it appears that further upside—and actual spending—will largely depend on clarity around the new Administration’s fiscal and regulatory policy agenda. Comments from the regional manufacturing surveys, highlighted below, support this notion; fora number of respondents, recent increases in capex plansappear to be based on optimism rather than hard orders.

To be fair, the New Orders index in the ISM Manufacturing Reporthas gained over 6 points since October, signaling a pick-up in reported orders on an economy-wide basis.

Moving to the near-term outlook for equipment investment, the January durable goods report suggests a temporary pause within a strong recent trend. Core capital goods orders fell 0.4% in January after a 3.3% rebound over the prior three months,and shipments also declined. Nevertheless, we see equipment investment on track for a strong gain in 1Q17,and our February Capex Plans Index suggests that businesses remain poised to invest—so long as fiscal policy delivers on its promises.

Things are almost bound to fade somewhat from here given the honeymoon Trump is enjoying in markets. As well, some of this is not Trump at all, it’s the post-OPEC cuts surge in oil and gas capex.

Even so, it’s impressive and further fuel on the bullish US fire.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.