From Westpac, some good material on the US consumer:

Confidence is a key factor for the underlying health of the economy and its ability to adjust to changes in the stance of monetary policy. Simply it determines households’ willingness to consume and invest as well as firms’ investment and employment decisions. Following the election of President Trump, confidence surged across the board in the US and hasn’t looked back. Herein we consider some of the underlying detail of the confidence surveys and the associated implications for policy.

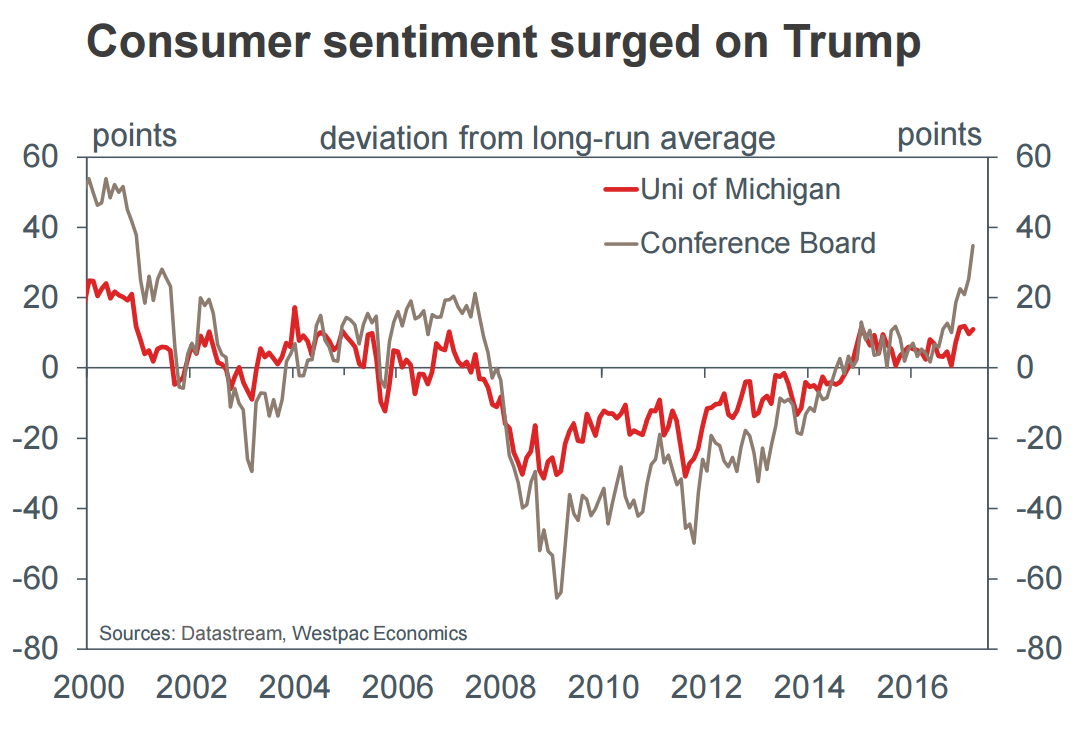

Having stabilised around its long-run average before the election, sentiment amongst US consumers is now reported as being materially above average. Indeed, the Conference Board measure of sentiment now sits at its highest level since end-2000 – a heady time of hope built on historically low unemployment; strong growth in household wealth; and belief in technological progress.

In a similar vein to that prior period, it is notable that the recent gains in headline sentiment have again been supported by a strong labour market (albeit one arguably dealing with considerably more underlying slack than in 2000) and wealth creation (S&P CoreLogic Case-Shiller house prices having regained their post-GFC losses and the stock market being at record highs) as well as belief in progress – albeit this time coming from fiscal policy rather than technology.

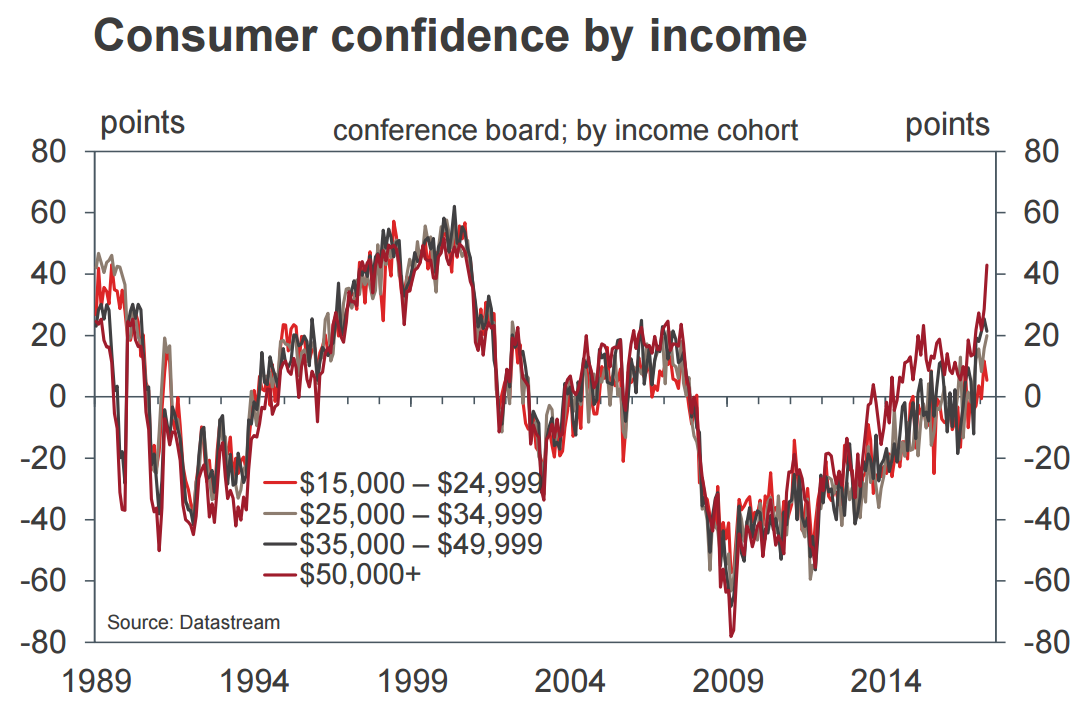

It is positive that the gains for confidence have been broad-based across income cohorts. This speaks to a belief that opportunity is being created for all. However, also evident is a historically-large deviation in confidence levels among income cohorts. To give a sense of the scale of this disparity: the confidence of those with an income of $50,000 or more is 43pts above its long-run average; in contrast, the confidence of consumers with an income of less than $25,000 is only 5pts above average. Clearly, while the labour market and asset price gains are creating opportunity for all, the benefit is not being shared equally.

Further colour is offered by the University of Michigan’s ‘Survey of Consumers’ split between Republicans and Democrats. At March, the expectations index for Democrats was just 55.3 (signalling, according to the Survey’s Chief Economist, that “a deep recession was imminent”); meanwhile among Republicans, the same component stood at 122.4 (suggesting “a new era of robust economic growth was ahead” for the US).

Arguably the disparity in sentiment amongst income cohorts and between Republicans and Democrats comes down to two key policy areas: health care and taxation. On the former, while House Republican infighting saw a vote on a replacement for Affordable Health Care delayed indefinitely, the threat of reduced care (at a higher cost) for lower and middle-income households will linger. On taxation, it is very clear that President Trump’s policies favour higher income households and, as a result, will only provide concentrated support for confidence in this segment of the population.

Given the dispersion in confidence across incomes and the political spectrum, the best expectation for consumption growth through 2017 is a continuation of the solid gains experienced over the past year, near 3%yr. An annual growth rate closer to the 1998–2000’s strong 5%yr would require a broadening of confidence and (arguably) income growth across the entire population.

For policy, to the extent that the FOMC categorise their current tightening pace as “gradual”, solid gains for consumption together with a strong labour market are enough to warrant further rate hikes.

Indeed, the strength in headline confidence gives a clear window for further progress to be made by the FOMC in their pursuit of policy normalisation. This is particularly true given the FOMC believe that the real Fed Funds Rate is currently below neutral and, on their forecasts, will remain so going forward as productivity lifts.

Previously we had a central expectation of one further hike to the end of 2017. But given the strength of confidence and the absence of a reaction from financial markets to President Trump’s health care loss, we now see there as being scope for two more hikes in 2017. We retain our call of two further hikes in 2018, leaving the Fed Funds Rate at a peak of 1.875% by the end of 2018. On our own expectations of potential growth and inflation, that would leave the stance of policy broadly neutral in real terms.

And it was the poor that voted him in. What a con!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.