Total housing finance (ex-refinancing) up 1.3% mom in January (+15.6% yoy), driven by a 4.2% mom surge in investor commitments Investor housing finance commitments have surged 27.5% over the past year, with a dramatic turnaround in trends here evident following the RBA’s two rate cuts last year (with investor finance, for example, having fallen 25.3% over the year to April 2016, I.e. the month before the RBA’s first cut in 2016). On the owner occupied side (excluding refinancing) new housing finance commitments fell 1.5% mom in January after three solid increases to be 5.6% higher over the year.

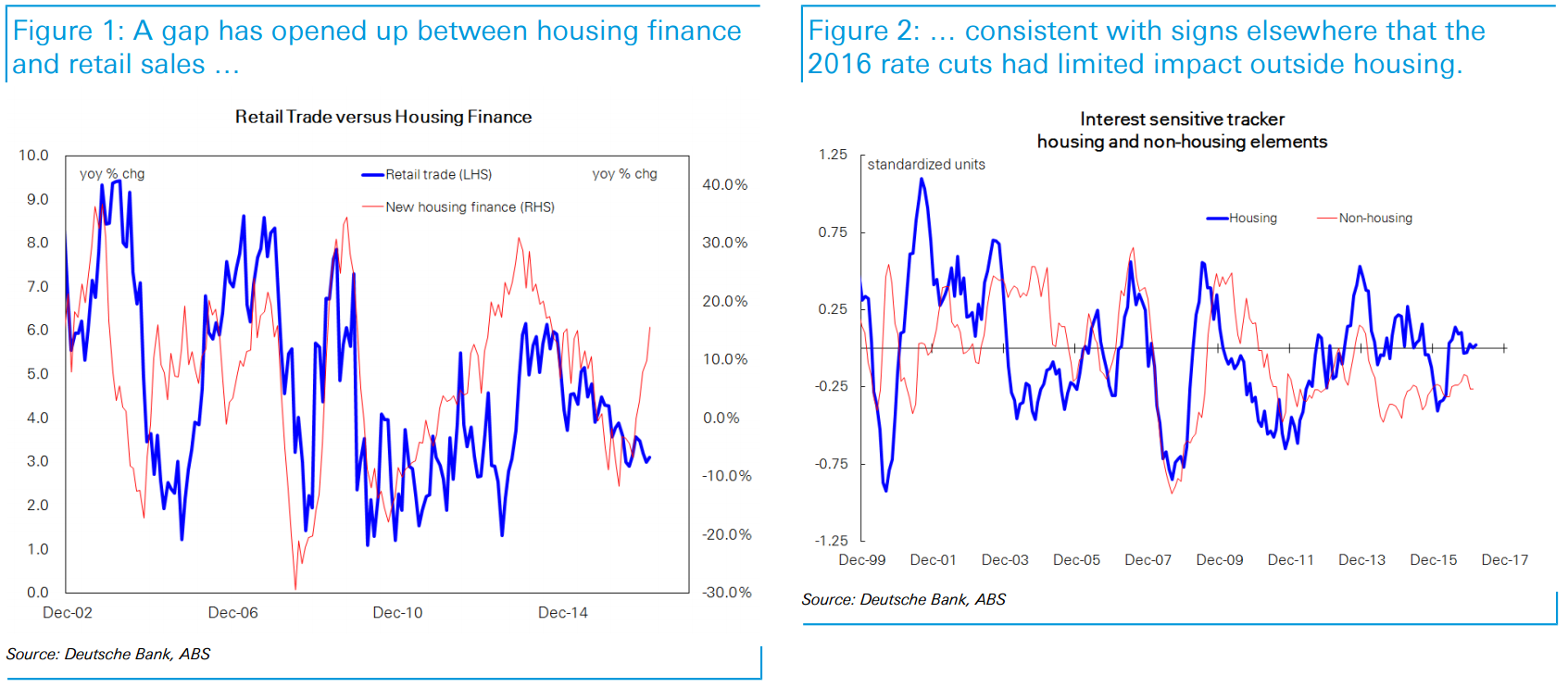

Interestingly there is a reasonable disconnect between the housing finance data and retail sales (see the first chart over). While trends in retail can sometimes lag trends in housing, we suspect very weak growth in wages and household incomes may see the gap persist; before growth in housing finance commitments moderates some as we move past the most recent rate cut. (There is also an expectation on our part of additional regulatory ‘pressure’ on lenders should growth in investor commitments fail to slow.) The disconnect between trends in retail and housing finance is also reflected more broadly in the persistent gap between the housing and non housing series that make up our interest sensitive tracker (second chart, with charts accessible via the url link above).

Put simply, it is hard to find much evidence that the two rate cuts last year did much apart from give parts of the housing market/sector another leg up. With the RBA now apparently more concerned about trends in housing and household sector leverage than was the case a year ago, we adjusted our cash rate forecasts earlier in the week to have the RBA on hold over 2017 and 2018 (we previously looked for a cut this year).

That’s shrinkfaltion at work: house prices so high that a paralysed community won’t transact and deal volume falls kill off economic spillovers.

But it’s not fair to say that the RBA cuts did nothing for the economy. Amid the terms of trade rebound had the RBA not cut, the dollar would have rocketed to 85 cents, smashing everything in its path.

Anyway, given higher house prices will only make shrinkflation worse, there is no point trading that for clear financial stability risk right around the corner.

Advertisement

There is no reason for the RBA to tighten vis inflation or economic strength so APRA needs to lower the investor speed limit to 5% right away. With three-quarters of investor lending pouring into Sydney and Melbourne it will be implicitly targeted geographically. The RBA can then cut again and the dollar will sink like a stone into the 50s cents. That will prevent any bust and accelerate the real exchange rate adjustment that we need, less credit and more tradables. At a 5% ceiling for every bank, specufestors will be unable to drive another round of speculation.

The only other targeted option is fiscal tightening, like cuts to capital gains or negative gearing tax concessions. Perhaps APRA is waiting for the Budget. It shouldn’t. The signs are clear that it will not be enough.

The alternatives are clearly worse. If the RBA is forced to tighten until the bubble pops then we’ll very likely see a recession. The 2002 double-hike combined with house price jawboning hammered Sydney house prices. Doing that as the dwelling boom comes off will be seriously pro-cyclical in 2018.

Advertisement

Sitting around doing nothing is absurd. The bubble will just run. That is the financial stability worst case.

If APRA will not move then the RBA must order it to. Excuses about division of responsibility around prudential versus monetary management are the worst kind of bureaucratic arse-covering.

Get on the phone and get it done. You’re supposed to be a balance sheet hawk, Phil Lowe.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.