By Gareth Aird, senior economist at the CBA:

Key Points

- The RBA Board Minutes confirm that policy is on hold over the near term.

- Strong dwelling price growth and concerns around the further build-up of debt in the household sector mean that rate cuts are off the table.

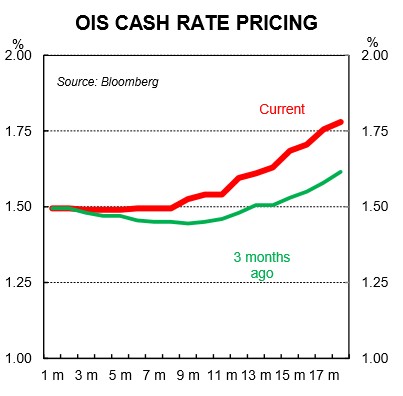

- Market pricing implies very little chance of another rate cut while a 60% chance of a rate hike over the next year is priced.

- We expect the cash rate to stay on hold over 2017 and well into 2018.

The Minutes

Today’s Minutes are yet further evidence that the RBA is firmly on hold. The Board have retained a relatively optimistic view of the global and domestic economies. And concerns around household debt and dwelling prices were once again aired. This time, however, the Board was more explicit on housing-related risks by noting that, “recent data continued to suggest that there had been a build-up of risks associated with the housing market.”

On the international economy, the Board sounds relatively upbeat on recent developments. In particular, it was noted that, “a number of indicators, including growth in global industrial production, global trade volumes and business sentiment, had improved.” And more importantly for monetary policy, “recent data had also confirmed the pick-up in global inflation.”

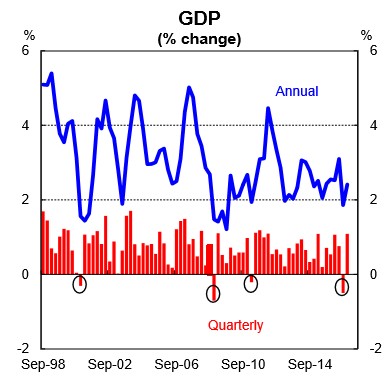

The solid 1.1% lift in real GDP in the December quarter backed up the Board’s view that the weakness in the September quarter was temporary. Indeed, the Minutes note that growth over QIV had been, “above expectations”. The RBA continue to expect growth to pick up above its potential rate over the forecast period. This is clearly a best case scenario with the risk that growth outcomes undershoot the Bank’s expectation.

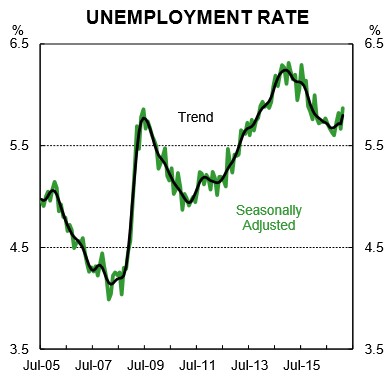

The Board continues to lack conviction in its assessment on the labour market, noting that it, “remained difficult to assess”. The RBA expects spare capacity to “decline slowly.” Here we note that the Minutes predate the February employment report (published last week) which showed employment contracted over the month and the unemployment rate lifted to 5.9%. Another weak employment report would see the RBA’s forecasts for employment and wages growth tested.

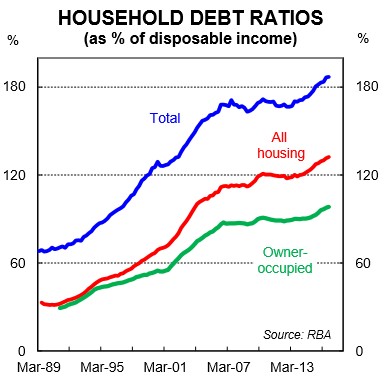

On housing, the Board has upped its rhetoric around the build-up of risks. The Minutes note that, “borrowing for housing by investors had picked up over recent months and growth in household debt had been faster than that in household income”. These comments coupled with the RBA’s acknowledgment that, “there had been a build-up of risks associated with the housing market” could be interpreted as the Bank calling on APRA to further place restrictions on lending to investors. In other words, watch this space.

On the AUD, the Board notes that, “an appreciating exchange rate would complicate the adjustment of the economy”. We suspect that the RBA would have been expecting a March Fed rate hike to take some pressure off the AUD. But the currency has strengthened since the Fed tightened policy and is edging further away from where we think the RBA views the sweet spot (low USD0.70s). The RBA’s well telegraphed reluctance to take the cash rate any lower has put more upward pressure on the AUD than would otherwise have been the case.

The Outlook

We see little chance of further policy easing despite core inflation running below target and the unemployment rate being above the level associated with full employment. The consistent message from the RBA over the last six weeks has been that rate cuts are off the table.

When Governor Lowe appeared before the House of Representatives Standing Committee on Economics in late February he stated that, “the market pricing is for interest rates to be constant right through this year. That seems a reasonable proposition to me.” He further added that, “the main effect (of another rate cut) would be more borrowing for housing, pushing up housing prices.” This is clearly undesirable.

In our view, it would take a sustained loss of momentum in job creation or a fall in dwelling prices for Lowe to entertain the idea of taking the policy rate lower. Neither outcome is in our central scenario and as such, we see the RBA on hold over 2017 and well into 2018.