A quick, chart-heavy recap of the main data points we’re watching, key shifts in views and Aussie relevant insights from our global teams.

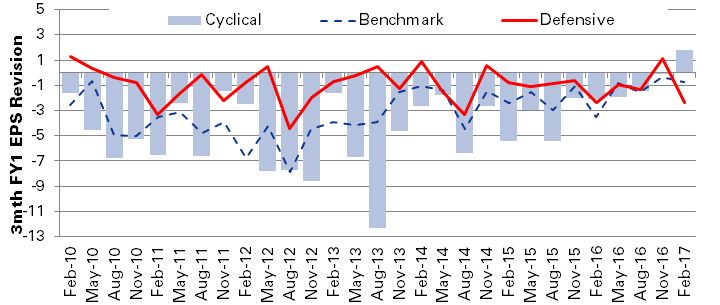

The macro continues to point to improving momentum. We continue to position for further rotation into value/cyclicals: The Australian economy continues to improve, house prices and investor credit continue to rise sharply, and with the RBA more focused on financial stability risks we now see a November 2017 rate hike (only 2/24 economists calling for a 2017 hike). 1H earnings provided just enough optimism to support the ongoing rotation with cyclical stocks seeing positive earnings revisions for the first time since the GFC.

Exhibit 1: Earnings revisions for cyclical stocks are positive for the first time since the GFC

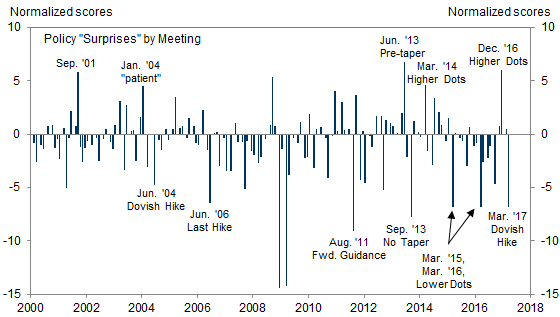

Despite only minor changes to FOMC projections, financial markets took the meeting as a large dovish surprise—the third-largest at an FOMC meeting since 2000 (outside the GFC). Our FCI eased sharply, by the equivalent of almost a full cut in the cash rate.

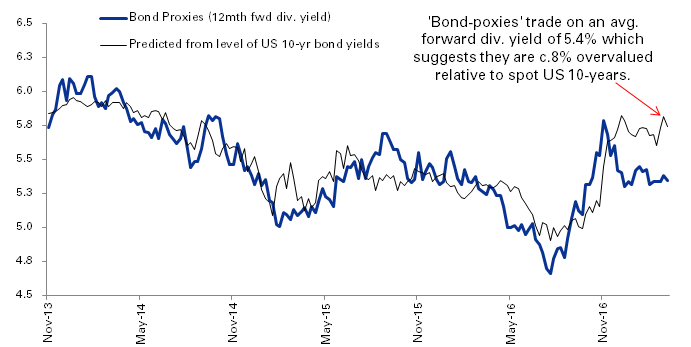

With interest rates moving higher, bond-proxies now look more expensive relative to rates: ‘Bond proxies’ appear c.8% overvalued given the recent move higher in US bond yields (c.25% downside to this basket if 10-yrs mean revert to the 20-yr avg). In a rising rate environment, we believe active AREITs (Buy PLG (CL), HPI, MGR) and infrastructure names with organic growth (Buy SYD) are best placed.

Exhibit 3: The basket of ‘bond proxies’ we track appears c.8% overvalued given the recent move higher in US bond yields.

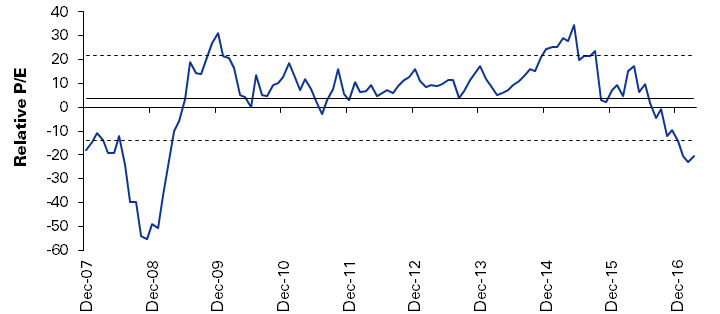

Retail: The market is significantly undervaluing Bunnings – Buy WES: With WES trading at its largest discount to WOW since the GFC, Adam Alexander recently re-iterated his Buy. The closure of Masters leaves Bunnings poised to deliver strong sales growth, margin expansion and acceleration of store roll-outs. Despite these positive tailwinds, our SOTP valuation (see p.6) implies Bunnings trades at a P/E of only 12.4x FY18E (a 30% discount to the ASX 200 Industrial average). Further, the recent investor tour of their new UK assets gave us increased confidence in this expansion strategy.

Exhibit 5: WES is trading at a 21% discount to WOW. Assuming Coles trades at the same P/E as Woolwooths, implies Bunnings trades at only 12.5x FY18.

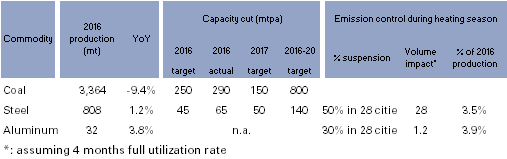

Resources – China’s production cuts are a positive for commodity prices…

Over the past decade China has emerged as a major producer of metals (now for c. 20% of global supply). With supply-side reforms continuing, we assert that China’s government will curtail capacity considerably and that oversupply should be much more limited than widely perceived. We see supply curtailments as most positive for AWC, S32, RIO & BSL.

Exhibit 6: Key Policies in 2017

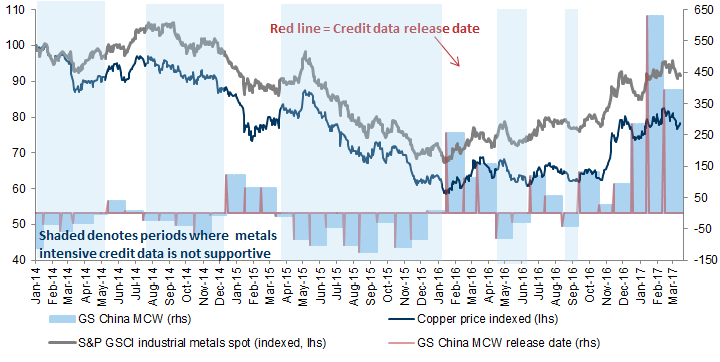

…. as is the strong credit demanded by China’s metals intensive ‘old-economy’

Exhibit 8: China’s ‘old economy’ credit, as measured by our GS China Metals Credit Wave tracker is still supportive for pricing

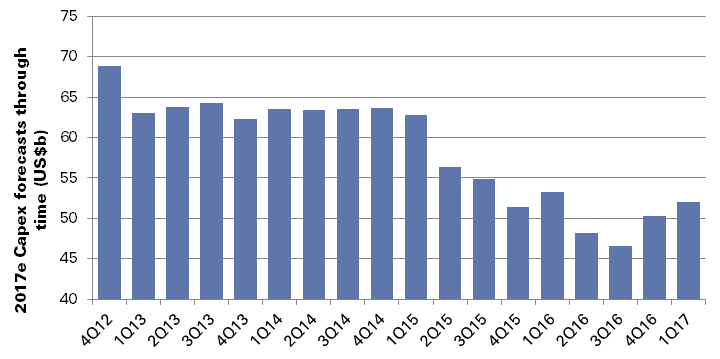

…But improved cash flow is slowly finding its way back to rising capex spend: On the back of strong commodity prices, Craig Sainsbury highlighted how 35% of companies raised capex spend during the recent reporting season suggesting the global cut in mining capex is over (down c.60% from the 2012 peak). In the past six months, we have raised our forecasts of 2017 capex spend by US$5bn (+8%).

Exhibit 9: Momentum in mining capex appears to have turned

Quarterly capex levels for the top 10 mining companies

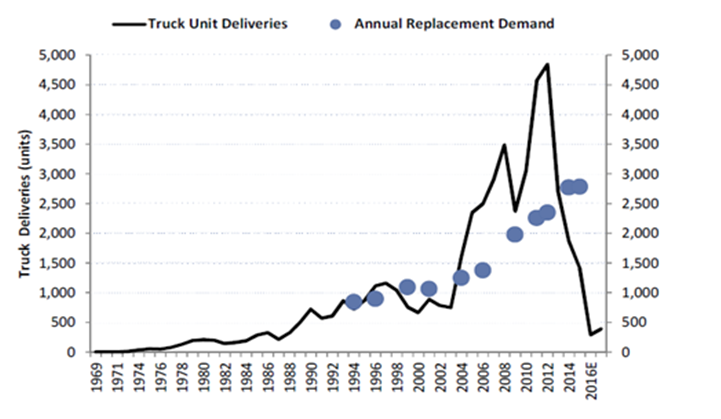

Looking to play the capex recovery? Nathan Reilly believes Seven Group (SVW.AX, Buy) is best positioned with the normalisation of mining capex and machinery investment, driving a significant surge in activity for CAT dealers like WesTrac.

Exhibit 10: Truck deliveries are currently well below replacement demand (assuming 15yr life)

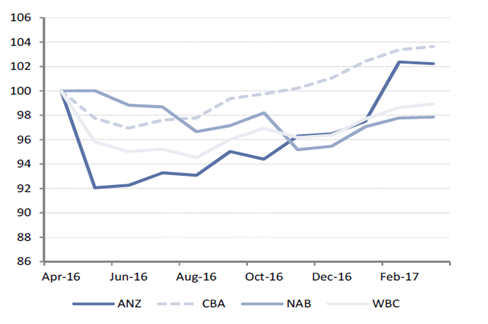

CBA’s 1H17 returns (ROTE) expanded sequentially for the first time in seven halves, driven by a combination of improving operating profitability (expenses) and asset quality. Andrew Lyons does not believe that this stabilizing returns outlook is reflected in valuations; CBA’s P/E is close to its 5-yr low relative to the sector despite its better EPS trajectory.

Exhibit 11: Major bank 12-mo forward EPS trajectory

A few thoughts:

there is only one way that the RBA will hike rates by year end and that is if the Do-nothing Government stimulates a final mad dash into housing and prices give it no choice. In that event I would be using the blowoff to exit the country anyway;

bond proxies are a bad bet as rates rise, yes, regardless of what happens here;

supply side reform is all well and good but iron ore and coal market dynamics mean that prices are going to fall anyway before long. Inventories are the key to prices now and at their current rate of accumulation ports will be full by October. Coal consolidation is clearly paused to let prices settle. The base case for iron ore in H2 is $60 which would only meet the Budget outlook so offers little upside to anything but big miner profits;

yes, Chinese credit is still supportive but is slowly slowing;

we’re in a secular cost-out phase for mining capex. A bit of a bump now the is immaterial not an investment case. There is no major new investment coming;

Wesfarmers is exposed to shrinkflation;

CBA deserved to lose its premium owing to WA over-exposure and its regulatory woes. Does it now deserve it back?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.