Normally sensible Peter Martin has penned a spurious piece today throwing his support behind ‘shared equity’ mortgages. Let’s examine his key arguments:

The critics leapt on the weekend announcement of a (small) pilot program in which the [Victorian] government would take an equity share in private homes, saying it would “drive up prices” and force homeowners to borrow from both a bank and the government.

Yet if it’s such a bad idea (socialist, even) why was it first proposed by the Liberal Party-aligned Menzies Research Centre, why did Prime Minister John Howard commend it to his home ownership task force, why have both Malcolm Turnbull and Scott Morrison championed it, and why was Tony Abbott an early adopter?..

The answer is pretty obvious, Peter. Governments of all persuasion are more interested in providing the illusion that they care about housing affordability, rather than taking genuine action. This is why we constantly see self-defeating policies and proposals like first home buyer (FHB) grants and subsidies, allowing FHBs to access their superannuation to buy property (which you also support), as well as shared equity schemes. The hidden goal of all of these schemes is not to improve housing affordability, but to boost FHB demand and support housing values.

Back to the article:

Private home ownership is relatively new. Up until the late 19th century most families rented from wealthy landlords… The federal government chipped in with grants to help cover deposits and also instructed the Commonwealth Bank (then part of the Reserve Bank) to lend to homebuyers itself and make sure the private banks did. By the time Robert Menzies stepped down as prime minister in 1966 Australia was said to be the biggest home-owning nation in the world…

It’s the same with the next revolution, from the mid-1990s. Securitisation allowed non-bank lenders to offer much cheaper loans using funds predominantly sourced from overseas. It made home-owning easier once again, and probably also helped push up prices…

Now Morrison and Turnbull are drawing up a budget with access to housing as its centrepiece. If they make it a Commonwealth scheme, the Commonwealth could hang on to the equity in each house for only a short time before on-selling it. It would signal that the scheme’s legit.

Like each of the revolutions before it, it runs the risk of pushing up prices, although only to the extent that it makes housing more attainable. But it would get people into housing and break the historically unusual and unhealthy nexus between investment and roofs over our heads.

Sure, the early creation of a mortgage market did make housing more attainable for Australians. This is hardly a surprise.

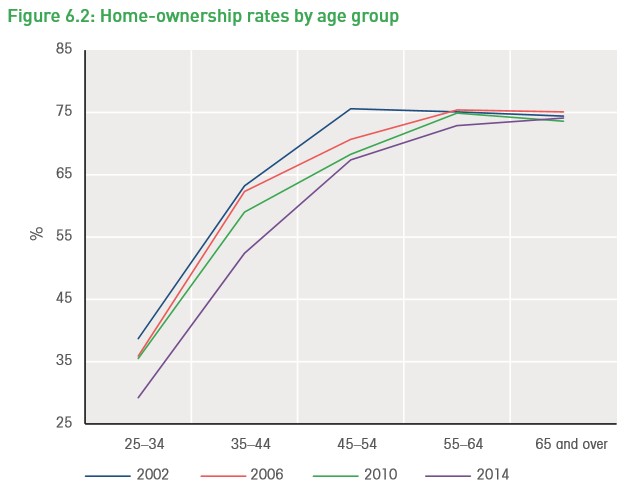

But why has Martin ignored the simple fact that home ownership rates have fallen for decades despite financial deregulation in the early-1980s, securitisation in the 1990s, various FHB subsidies, the cratering of mortgage rates, etc?

With the most significant falls in home ownership experienced by the younger FHB-aged cohorts?

What does this tell you about the argument that increasing mortgage availability necessarily increases home ownership, as well as the likely success of shared equity schemes?

The fact of the matter is that shared equity schemes will very likely increase housing demand and therefore prices (other things equal), thus becoming self-defeating from a housing affordability perspective. This is because:

- A new pool of lower income buyers that would not qualify for a conventional mortgage would suddenly be able to enter the market and bid up prices; and

- Buyers that do already qualify for, say, a $400,000 conventional mortgage may choose to take advantage of a shared equity scheme so that they can purchase a more expensive home than they could otherwise afford.

Thus, shared equity arrangements would further fuel price rises in the housing market, resulting in further reductions in home affordability (other things equal).

Another important drawback is that private sector proposals for shared equity arrangements – as favoured by Scott Morrison – are likely to involve the equity provider sharing a disproportionately high share of any capital gains, and a disproportionately low share of capital losses (if any).

Thus, such shared equity schemes will at best erode the value of the home as a store of household wealth, and at worst in a declining market increase the likelihood of home owners holding significant negative equity in their home.

Ultimately, housing affordability cannot be improved by pumping yet more buyers and credit into the system. Moreover, the last thing the nation needs is to miss-allocate more of of the country’s capital into an already overheated and overvalued housing market.

Housing affordability can only be improved my implementing measures that either reduce demand or increase supply, including:

- Slashing immigration to sensible and sustainable levels [reduces demand];

- Undertaking tax reforms like unwinding negative gearing and the CGT discount [reduces speculative demand];

- Tightening rules and enforcement on foreign ownership [reduces foreign demand];

- Extending anti-money laundering rules to real estate gatekeepers [reduces foreign demand]; and

- Providing the states with incentive payments to:

- undertake land-use and planning reforms [boosts supply];

- swap stamp duties for land taxes [boosts effective supply]; and

- reform rental tenancy laws to give greater security of tenure [reduces demand for home ownership].

Sadly, Peter Martin has already revealed that he is an avid fan of mass immigration and a ‘Big Australia’. Now he has also shown that he supports self-defeating schemes like allowing FHBs to access their superannuation to purchase a home as well as shared equity mortgages.