Morrison cheerleads investor bubble as regulators snore

From the real estate Treasurer, Scott Morrison, at Bloomie yesterday:

Some quotes:

In Australia our prices may be high, particularly in Sydney and Melbourne, but they’re real.

The issue on housing affordability and prices in Australia is the mismatch between supply and demand.

It’s not the function of any sort of investor credit bubble or anything like this.

They’re real prices, they’re real values, and what we’re working as a government to do is put downward pressure on those rising prices by addressing the supply challenges that are out there and working with state governments to achieve that.

As we’ve pointed many times, supply constrained markets do not prevent bubbles, they create them, along with greater volatility. Such a situation can be explained using basic supply and demand analysis, as shown in Figure 1.

Q0 and P0 represent the initial equilibrium situation in the housing market. Initial demand is provided by D0, whereas supply is shown as either SR (restricted) or SU(unrestricted), depending on whether land supply constraints exist.

Following an increase in demand, such as a surge of investors following changes to tax rules (e.g. Australia’s CGT reduction in 1999), the demand curve shifts outwards from D0 to D1. When land supply is restricted, house prices rise sharply from P0 to PR. By contrast, when supply is unrestricted, prices rise more gradually from P0 to PU.

The situation works the same way in reverse. For example, if there was a sharp fall in demand following a contraction in credit availability or a sharp decrease in Australia’s Terms of Trade, causing demand to fall from D1 to D0, then prices fall much further when land supply is constrained.

The key point of this analysis is to show that price bubbles are in fact a feature of supply-constrained housing markets.

He also stressed the efficacy of previous macroprudential measures. I can’t tell if that means more or less of it.

So now we know that the Council of Financial Regulators met with Morrison last week. What did they discuss if not further tightening to address this:

And this:

The RBA can’t tighten because inflation and economic strength are weak. So APRA needs to lower the investor speed limit to 5% right away. With three-quarters of investor lending pouring into Sydney and Melbourne it will be implicitly targeted geographically. The RBA can then cut again and the dollar will sink like a stone into the 50s cents. That will prevent any bust and accelerate the real exchange rate adjustment that we need, less credit and more tradables. At a 5% ceiling for every bank, specufestors will be unable to drive another round of speculation.

The only other targeted option is fiscal tightening, like cuts to capital gains or negative gearing tax concessions. Perhaps APRA is waiting for the Budget. It shouldn’t. The signs are clear that it will not be enough and might even add more fuel to the fire.

The alternatives are clearly worse. If the RBA is forced to tighten until the bubble pops then we’ll very likely see a recession. The 2002 double-hike combined with house price jawboning hammered Sydney house prices. Doing that as the dwelling boom comes off will be seriously pro-cyclical in 2018.

Sitting around doing nothing is absurd. The bubble will just run. That is the financial stability worst case.

If APRA will not move then the RBA must order it to. Excuses about division of responsibility around prudential versus monetary management are the worst kind of bureaucratic arse-covering.

I continue to reckon that further action is forthcoming. Anything else would be openly insane, even in Australian terms. UBS agrees:

But as Tharenou points out, that measure of affordability heads to the “worst on record” if mortgage rates rise just 100 basis points from their current low level.

The high level of household debt is the major reason the RBA would prefer to keep official interest rates on hold for as long as possible while the Australian Prudential Regulation Authority does more work to take the sting out of the property market by targeting property investors.

After all, that’s where all the growth is.

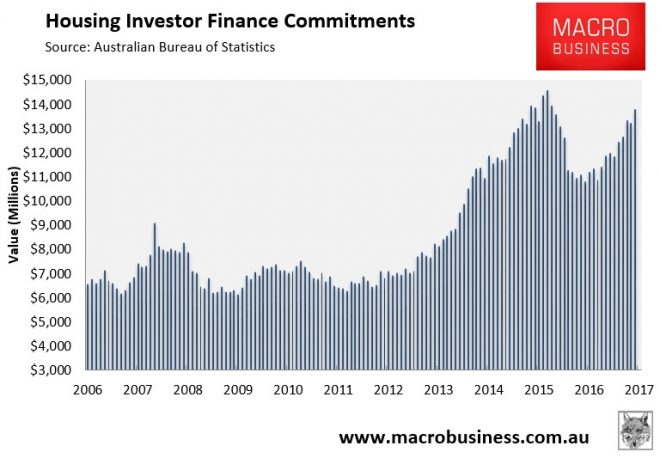

Investor loans are growing at 27 per cent per compared with just over 5 per cent for loans to owner-occupiers, despite the banks hiking mortgage rates for investor loans in 2016 and leaving home owners relatively untouched.

Already there is talk that APRA could lower the threshold for total lending to property investors to 7 per cent year on year from 10 per cent at present.

If the accompanying statement from last week’s RBA meeting is any guide, the bank thinks more needs to be done to curb lending standards when it comes to the rampant housing market.

If APRA does more on that front it allows the bank to keep the official cash rate low while the inflation rate remains so far below its target rate.

7%. Chinese water torture.