by Chris Becker

A somewhat mixed session in Asia today as the poor lead from overnight markets eventually translated into some positive moods locally and in Chinese markets, while Japanese stocks retreated again on the continued run to safety on Yen.

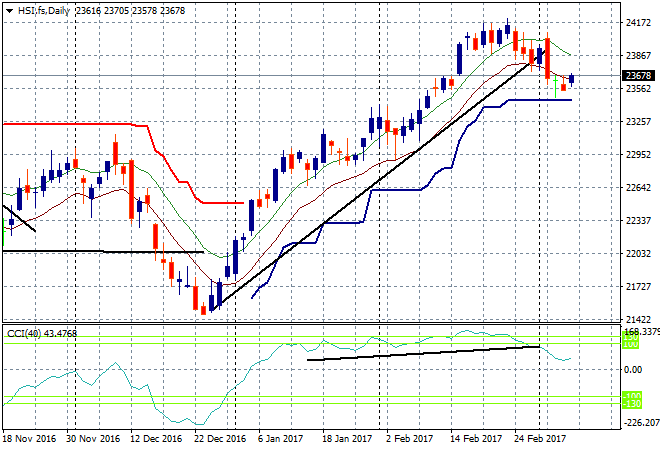

The Shanghai Composite is still in the green coming into the close, up 0.2% to 3237 points, still building above local support at 3200. The Hang Seng Index is doing somewhat better, up 0.4% to 23698, still below the 24000 points resistance level but bouncing off the prior bottom at the daily ATR support level at 23500:

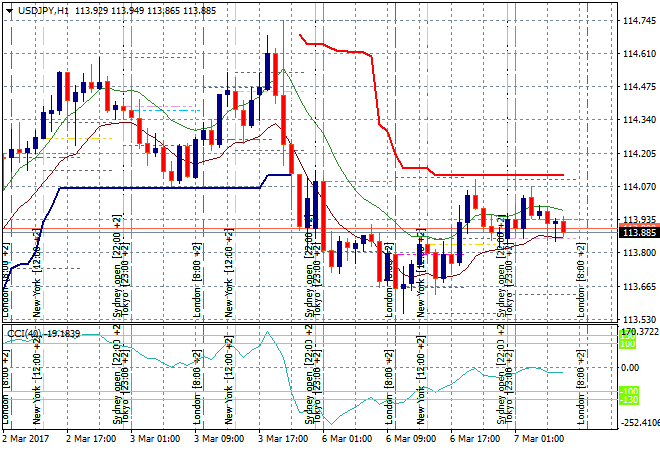

Japanese traders continue to remain cautious about regional risk with the Yen remaining strong on the safe haven bid, continuing to push local stocks lower. The Nikkei closed down 0.3% to finish at 19,326 points. The hourly chart for USDJPY shows an early attempt in the session to sell off and it reached the 114 handle twice before coming back below with Yen firming going into the London open. Resistance overhead at 114.10 or so will be key to break and for Japanese stock traders to follow through on the buy button:

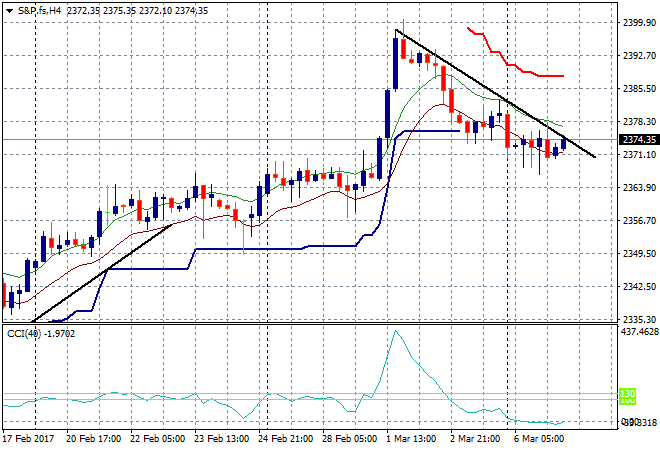

S&P futures have remained steady but the downtrend also remains intact – BTD is not yet over:

The ASX200 gapped down on the open as expected but rallied in expectation of a easier RBA, and while that didn’t come to pass it still finished up 0.3% for the day to 5761 points. BHP and RIO were the drags, both down nearly 1% alongside iron ore but it was financials that supported the market. The 5800 point resistance zone is the target to reach here.

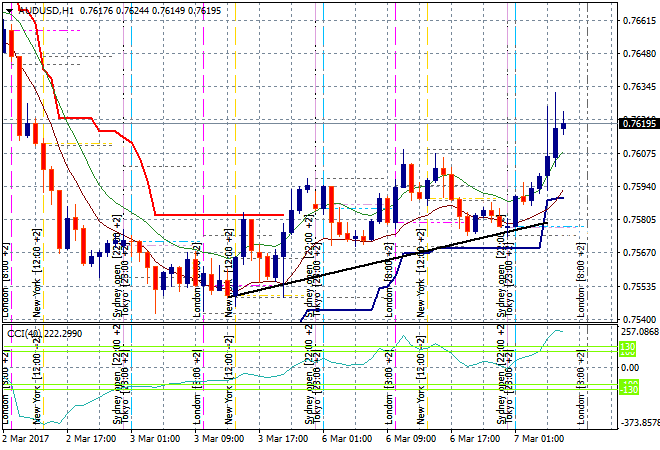

The Aussie dollar immediately found a bid on the Sydney open and lots of volume and front running buyers in the lead up to the hold decision by the RBA for some nice profits. The 76 handle was breached and looks bullish on the hourly chart, but it might be a case of too much too soon as we await the real movers in London to decide where its going:

The data calendar continues with two minor releases, namely German factory orders and US trade balance for January.