Financial imbalances in the Australian economy—in particular, acceleration in prices and speculative activity in the property sector—have intensified, and the RBA’s new Governor has confirmed a shift in the Bank’s reaction function to be both more responsive to these imbalances and less sensitive to low inflation. To date, several years of macroprudential initiatives have been the “first line of defence” against these imbalances and further action on this front is quite possible. However, Governor Lowe is on record cautioning that macroprudential approaches “may be less than fully satisfactory” and historically has been a strong proponent of an alternative approach “using higher interest rates to help contain financial excesses”.

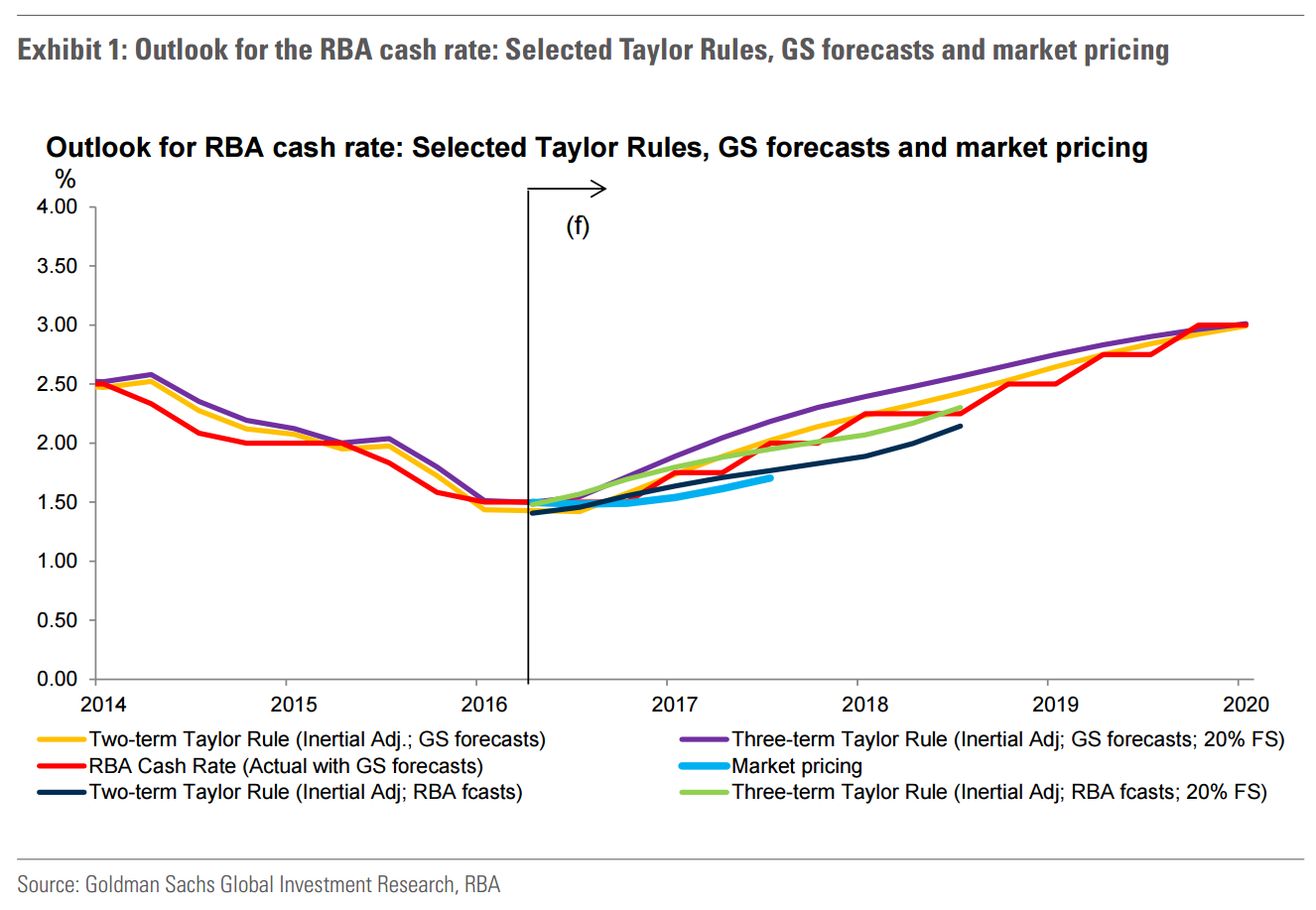

In this note, we consider the “modification to the prevailing monetary framework” Lowe championed earlier in his career and which recent communications suggest he still has sympathy with. Specifically, we test a range of scenarios, varying assumptions on both the emphasis the RBA places on financial stability and also the trajectory of current imbalances. Overall, we find that this shift in the RBA’s reaction function could reasonably lead to an end-2017 cash rate ~15-25bp higher than would have been previously assessed optimal—given plausible weights which we think the RBA is placing on financial stability.

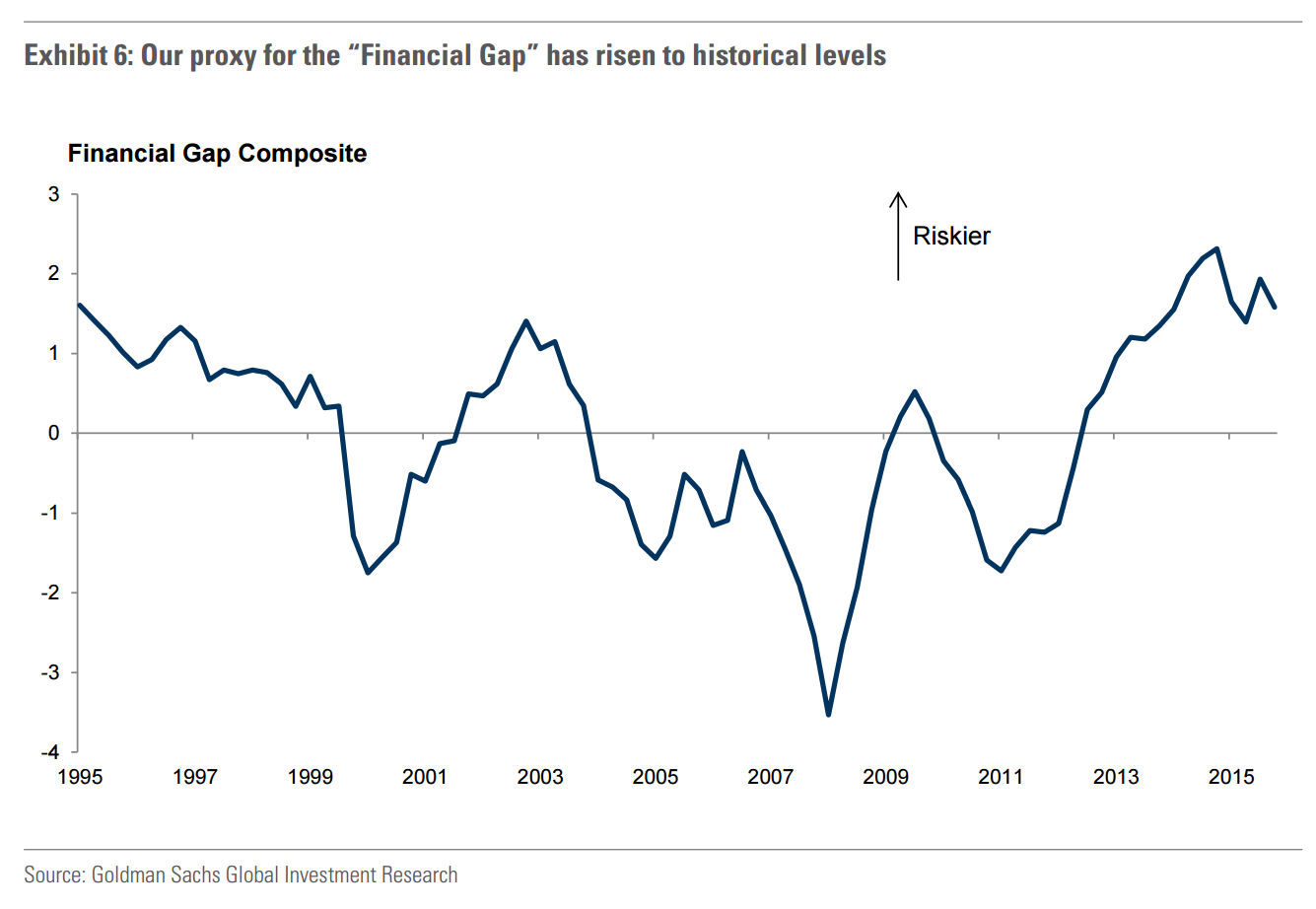

We conduct our analysis through the prism of a Taylor rule framework (inertialadjusted)—adding an additional variable on top of inflation and output to incorporate policy-makers’ sensitivity to financial imbalances. This third term—the “financial gap”, a proxy for the financial cycle—is derived by extracting the first principal component from a range of variables measuring credit and asset prices, and in our view adequately captures financial imbalances in the economy.

On face value, it is not obvious what the expected sign should be on the “financial gap” term in the Taylor rule. After all, the transmission mechanism of monetary policy works largely through the credit and asset price channels, and one would expect policymakers to encourage some degree of credit expansion particularly during times of subdued aggregate demand by loosening monetary policy—so, on the one hand, this argues for a neutral or slightly negative response to the “financial gap” variable. On the other hand, an excess build-up of financial imbalances can create vulnerabilities in the system especially when the economy is running hot and asset prices are already elevated, and in such times it would make sense for policymakers to “lean against the wind” by adopting a tighter policy stance—arguing for a positive sign on the “financial gap” variable. Taking a more sophisticated approach to adjust for different phases of a rate cycle, a “regime-switching” model provides some evidence that there have been periods in the past where the RBA’s reaction function has been more sensitive to financial stability (i.e., a positive coefficient)—periods which typically correspond to excesses in our proxy of the “financial gap”. (To be clear, we acknowledge that the “regime-switching” approach does retain some of the limitations that we found when modelling for simpler functional forms—in part related to difficulty identifying the direction of causality between the variables.)

Given that the RBA is now explicitly elevating financial stability considerations in policy decisions, we believe a selection of constrained three-termTaylor rules provides enhanced guidance on the outlook for the cash rate. We test these rules under two scenarios: firstly, where current financial imbalances gradually diminish and, secondly, where financial imbalances persist at current elevated levels. At one extreme, adopting this latter scenario for an equally weighted three-term Taylor rule points to an end-2017 cash rate that is ~40bp higher than estimated by the conventional two-termed benchmark. Looking forward, our base case implies a more modest +15- 25bp gap, assuming an ~20% weight on the “financial gap” term and that imbalances ease gradually over time.

The conclusions from our analysis are nuanced and are not intended to be directly prescriptive. It is also true that we have been factoring financial stability concerns into our cash rate forecasts for some time. Even so, this process of formalizing the way that we think about financial imbalances and the RBA’s evolving reaction function has hawkish implications overall, and we are changing our cash rate forecasts.

Specifically, having previously described a rate hike in November 2017 as a 40% probability, we now believe a +25bp increase on this timeframe is more likely than not (60% probability). That is, we have pulled-forward our forecast start of the RBA’s tightening cycle to November 2017 (+25bp; from February 2018) and now expect two rate hikes in 2018 (May and Nov), and three subsequent increase to take the cash rate to 3.0% by 2020. Our forecast November 2017 rate hike leaves us at the hawkish extreme of consensus expectations and implies materially more tightening than is currently priced-into financial markets (+2bp).

Nothing would give me greater pleasure than to see this. But if it does then I have one word for you in 2018: duck.

I would take this more as a measure of how much pressure there is mounting on APRA to get off its fat ass.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.