In this note I apply elementary statistical analysis to squeeze historic wholesale price data to see if they will offer a confession on why Victoria’s demand-weighted average wholesale electricity market price rose by 46% in 2016, compared to 2015.

A common technique I apply in analysing historic wholesale price data is to split the average annual wholesale price into a component that measures the average of the prices in the 72 most expensive half-hourly Settlement Periods in the year, and a second component which measures the average price in the remaining 99.6% of Settlement Periods in the year.

This allows me to see how average annual prices have been affected by the prices in the few extremely high-priced Settlement Periods in the year. The result of this dissection is shown in the table below.

Victoria ($/MWh)

2015

2016

Demand-weighted average price

$36

$52

Demand-weighted average price excluding top 72 settlement periods

$35

$49

Demand-weighted average price top 72 settlement periods

$268

$714

The table shows that the demand-weighted average price in the highest priced 72 settlement periods in each year was higher in 2016 than 2015 (the last row of the table) but then when you compare the second and third rows of the table you will see that the effect of these higher prices in 2016 was $3/MWh ($52-$49) and in 2015 it was just $1/MWh ($36-$35). Of itself this is not nearly enough to explain the much higher prices in 2016. And casting back to 2007, the 2016 result in Victoria is not exceptional. Putting the point more generally, higher market volatility in 2016 can not explain higher average prices.

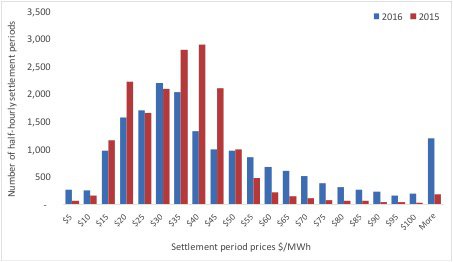

The figure below extends the comparison of the 2015 and 2016 wholesale prices in a histogram of all the half-hourly settlement prices in each of these two years. The X-axis shows the price bands that form the buckets of the histogram, and the Y-axis measures the number of Settlement Periods whose prices fall into each bucket.

It is striking in this figure that in 2016 there were much fewer instances when prices ranged between $35 and $45/MWh, and much more instances when prices were above $55/MWh. Effectively there was a step change in the distribution of prices in 2016, compared to 2015, when Settlement Period prices were above $30/MWh. Why?

Well, what happened in 2016 is that gas prices, as measured by the average quarterly prices in the Victoria Gas Market, rose 69% from $4.12 to $6.69 per GJ. The price of gas-fired generation that sets the wholesale market price in South Australia almost all of the time, in Queensland often and in New South Wales and Victoria sometimes, inevitably took a big leap up to reflect these higher gas prices.

Since the NEM is an interconnected electricity market that has unconstrained interconnectors for the vast majority of the Settlement Periods, the prices in one regional market flow through into the next. And thus we see how higher gas prices have flowed through into higher wholesale electricity prices.

I have replicated this analysis in the other regions of the National Electricity Market and see the same thing, although there are additional effects related to the exercise of market power in the highly concentrated Queensland and South Australia markets.

So what role has renewables played then? Well if you live in South Australia, on a sufficiently sunny and windy day it will be renewable generation that is producing almost all the electricity. Gas generators will often offer to pay the market for the privilege of continuing to produce electricity so that they continue to be dispatched and thereby avoid the higher losses they would otherwise incur if they were to to shut down and later have to restart their plant when the renewable production diminishes or demand rises. Amazingly these negative prices occurred for 196 hours in 2016.

Renewable generation in SA has depressed wholesale prices compared to what they otherwise would have been, just as has occurred in various European countries and states in the United States where renewable capacity has expanded to become a significant proportion of the generation mix.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.