As widely expected, the RBA left the cash rate unchanged at 1.5%. The accompanying meeting statement was little changed, with the exception of a few sentences:

1. The Bank notes that real GDP growth was around 2.5% in 2016, but quickly moves on from this fact.

2. There is an additional reference to at, or above average levels of confidence in the economy, implying that perhaps solid growth has continued into 2017.

3. On the flipside, officials acknowledge that the upside surprise in 4Q spending growth was funded by a sharp reduction in the saving rate in the absence of labour income growth. Uncertainties about the path of consumption growth remain.

4. The reference to an upturn in full-time employment growth was removed, as the trend has returned to negative territory following the January labour market report. Continuing the theme from previous statements, the Bank continues to believe in the global reflation story, as evidenced by:

1. Higher bond yields and the pricing out of additional monetary easing in the major economies.

2. Elevated levels of commodity prices and the boost to national income from recent gains.

Assessment

Rate hawks might be a little disappointed that the RBA chose not to make more of the recent upside surprise in real GDP growth. A cynic might argue that the recent upside surprise has not settled the Bank’s internal debate about the state of the economy. But in our view, the Bank was right not to take a victory lap, because the GDP data are backward looking. Indeed, the early signs for 2017 are not very positive:

1. There are some concerning signs for consumer spending. We are looking for slower consumption growth following the large draw down in household saving in 4Q. In this context, it is interesting to note that nominal retail sales rose by 0.4% in January, but discretionary spending data was quite mixed. Spending on electrical and electronic goods rose strongly, but apparel and department sales weakened. Over the past few months, nominal discretionary retail spending has flattened out.

2. The volume picture is not much better. According to the Melbourne Institute, CPI rose by 0.6% over the month. Even after accounting for differences between the CPI and retail price index (RPI), it appears that retail sales volumes were flat to down at the start of the year.

3. The trade balance has swung the wrong way. The trade balance fell sharply in January to $1.3 billion from $3.3 billion. Some of the deterioration may have been due to technical distortions from an early Chinese New Year (although we note that seasonally-adjusted iron ore export volumes were actually up in January, and down in February). Some of the fall also reflects weakness in spot coal prices. But notwithstanding these considerations, it appears that the trade balance has deteriorated in volume terms, because in 1Q the weighted average price of commodities has risen strongly, led by iron ore. Also, imports continue to rise, reflecting recent strength in the AUD. Deterioration in the real trade balance could mean that net exports are a drag on 1Q real GDP growth.

4. Building approvals are wobbling. Building approvals rose by 1.8% in January – but all of the growth came from the volatile apartment complex. Core housing approvals continued their recent trend decline, falling by an additional 2.2% over the month. Also, we note that non-residential building approvals have been weakening as well.

5. Median house prices are falling. According to Residex, median house prices fell in January. According to SQM, weekly asking prices for three-bedroom houses have also been falling through to early March. The data point to either outright weakness in house prices or at least, a composition shift towards cheaper housing. In our view, neither development is surprising given reduced Chinese buying interest (in the wake of more stringent capital controls) and softness in labour market conditions. We note that the median house price data are once again painting a different picture of the housing market to the widely-followed CoreLogic index, which continues to show strong gains in house prices.

In addition to these developments, we believe that government spending is likely to drag on economic growth in 1Q, because there was a pull-forward in spending in 4Q that is likely to mechanically unwind.

The main positive highlight for the economy in 2017 to date is the sharp rise in the NAB business confidence survey, and the RBA takes note of this. But even NAB admits that this increase could reflect distortions from the early Chinese New Year.

In our view, there are striking similarities between 1Q 2017, and 3Q 2016. To be sure, it is still too early to be able to quantify 1Q growth (or perhaps the lack there of) – but there is enough evidence to suggest that underlying growth is weaker than the year-to-4Q rate of 2.4%. We think that the average annualised pace of growth in 2H 2016 of only 1.2% is more representative of the economy’s pulse.

Outlook

The March meeting statement suggests that the RBA has not made any changes to its core views of the economy, notwithstanding the recent upside surprise in GDP. Prior to the GDP release, Governor Lowe made it clear that he does not see rate cuts as the best way forward for the economy. But yet, we remain of the view that the Bank will ultimately have to cut rates.

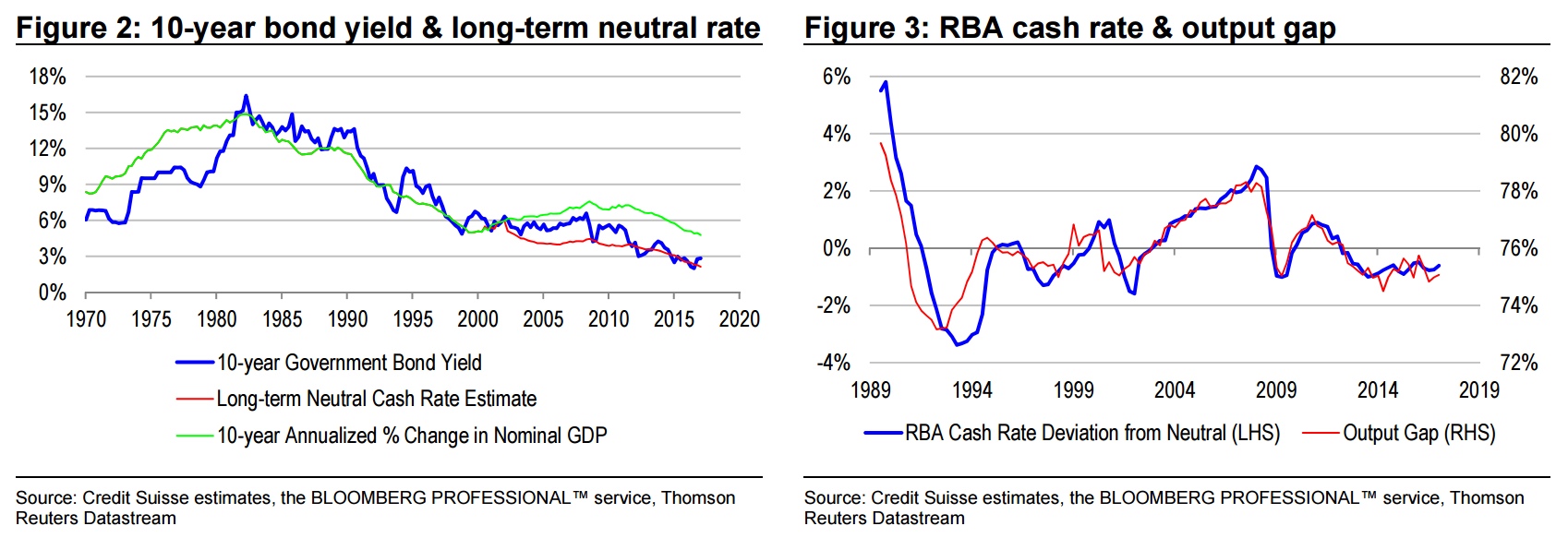

Our interest rate modeling framework estimates the short-term equilibrium value of the cash rate with reference to a long-term neutral rate, and the output gap as a proxy for how much the short-term rate should be deviating from the long-term rate. The long-term neutral rate is a function of 10-year rolling nominal GDP growth, and household gearing (specifically, an implied rate of interest that would allow overgeared households to breakeven on their cash flows).

With nominal GDP rising strongly in recent quarters on the back of sharp increases in the terms of trade, the 10-year rolling growth rate has remained high at around 4.8%. But net rental yields have fallen further below mortgage rates, making current gearing levels look more unsustainable. Hypothetically, the RBA would need to cut rates to -0.47% if it wanted to eliminate current overgearing. Our long-term neutral rate estimate lies half-way between these two views at around 2.1%.

Currently, the output gap sits at roughly 1% of GDP. Therefore, the short-term equilibrium value of the cash rate is 1% below the long-term neutral rate, or 1.1%. Our cash rate model continues to point to the need for multiple rate cuts.

But this is the starting point – not the end point. We remain of the view that the output gap will widen materially further in the next year, putting pressure on the RBA to cut rates below 1%. In this context, it is important to keep an eye on where the economy is going, and not just where it has been.

We think that the main catalyst for a change of heart from Bank officials is a credible challenge to the global reflation story. The next consideration is the direction of house prices. In our view, labour market and inflation softness are second tier, but are nonetheless still relevant in the event of large downside surprises.

The bank wants to cut. If APRA tightens it will. If APRA does not then it should be taken to the woodshed. If neither happens this is a good guide to how hard it will be for the bank to tighten at all.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.