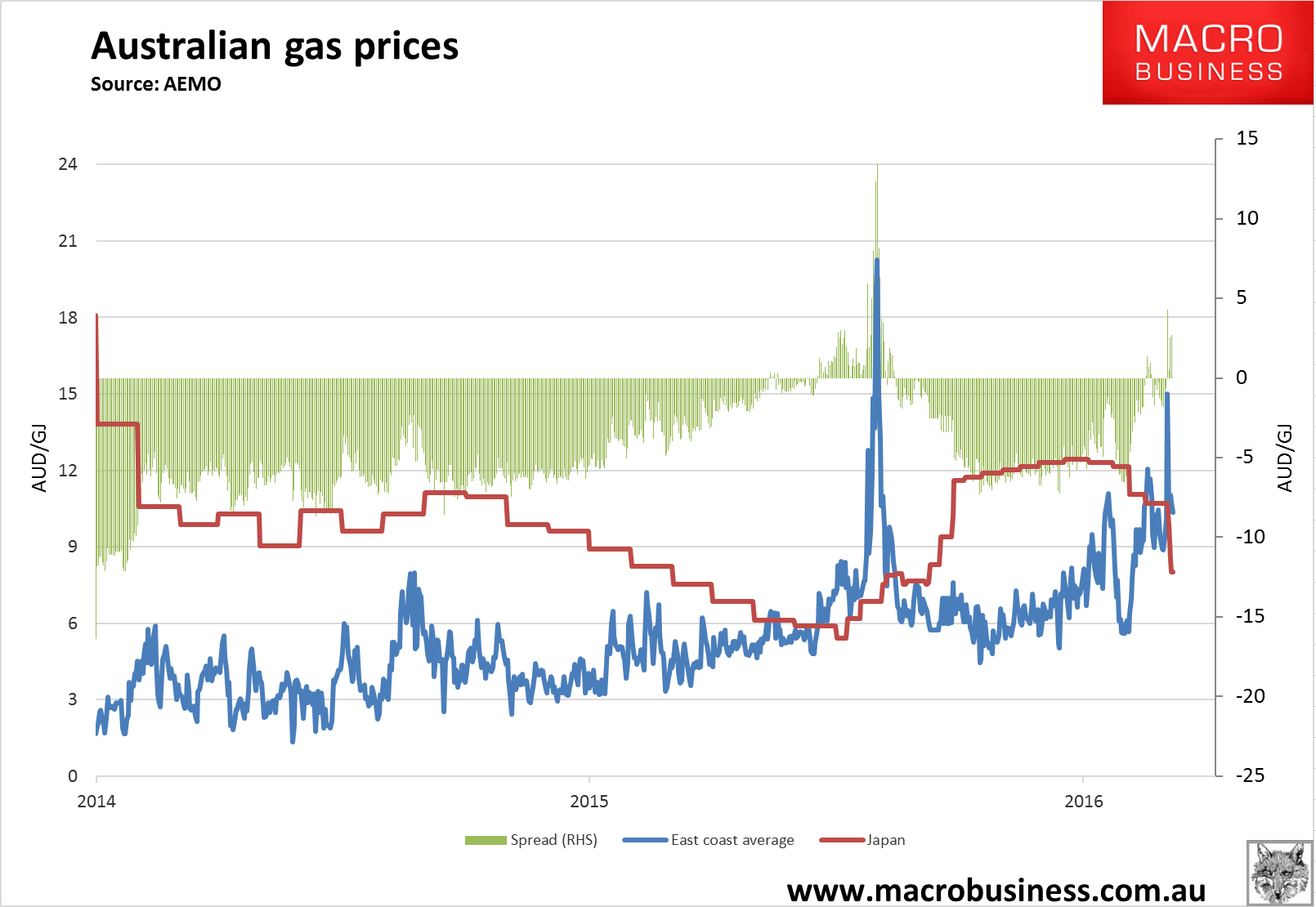

There is no relief today for gas or power prices with east coast average of the former still at $10.33Gj while in Japan exactly the same gas is available for $8.01Gj.

The gas panic is rising fast. From the AFR:

Investment in new gas production projects is “nowhere near sufficient” to ensure security of supply, posing a risk that the national gas market will unravel if states take matters into their own hands, said EnergyQuest consultant Graeme Bethune.

After analysing Queensland coal seam gas reserves and drilling results, Dr Bethune has found a risk that production won’t live up to the reserves figures and that the gas has been “oversold”.

The consultancy estimates a supply gap on the east coast of about 172 petajoules of gas by 2020, rising to 205 PJ by 2025.

Garbis Simonian, who operates a gas trading business for some industrial customers around NSW, said there was “some” gas available over the next few months but only at very high prices.

“There is some gas available, not enough to satisfy the market,” said Mr Simonian at Weston Energy. He blamed the situation on the need for some LNG ventures in Queensland, specifically Santos’s GLNG project, to buy third party gas to meet their export commitments.

…The biggest chunk of undeveloped gas on the east coast is the Arrow Energy resource jointly owned by Shell and PetroChina, but which Shell has said needs an LNG-scale market to warrant the investment to bring to the market.

Dr Bethune said Arrow gas would be enough so supply east coast demand for 15 years at current levels of demand.

That is roughly four million tonnes of LNG equivalent shortage, half of all of Santos LNG exports. It is also roughly the equivalent of third party gas that it sucks out of the eastern market that it never told anyone it would. And that still wouldn’t balance the market.

Meanwhile, at The Australian the follow-on electricity problem is also worsening fast:

Influential crossbencher Nick Xenophon has warned of “disastrous” consequences if Victoria’s Labor government follows South Australia by pursuing a state-based renewable energy target of 40 per cent by 2025 without “back-up power”.

The South Australian independent senator today said once Victoria’s coal-fired Hazelwood power station closed on March 31, the South Australian energy crisis “will be a contagion that spreads across the country”.

Senator Xenophon said a Sydney-based business had today told him its power bill was expected to increase from $50 million to $70m in the next 12 months.

…Frontier Economics managing director Danny Price said people should be very worried about the increased risk of existing power stations breaking down, as occurred last Friday at Torrens Island in South Australia, due to an increased load once Hazelwood closed.

“Over the next few weeks, as the power station shuts down, more load is going to come on the existing generators,” Mr Price said.

…“If you put more pressure on power stations they break more.”

Mr Price said there needed to be bipartisan political support for “some form of carbon pricing scheme”.

This comes a day after South Australian Labor Premier Jay Weatherill said he had written to Malcolm Turnbull urging the Prime Minister to reconsider an emissions intensity scheme and put it on the agenda for the next Council of Australian Governments meeting in June.

AN EIS has won the backing of more of Australia’s biggest energy producers and consumers, including BHP Billiton, EnergyAustralia, Origin Energy and the National Farmer’s Federation.

More from the AFR:

Senate powerbroker Nick Xenophon says he will not negotiate over passage of company tax cuts until the government deals with an energy crisis, which new forecasts show will see a national power crisis by the end of next year.

“In terms of priority I would have thought if you want to give relief to businesses and ensure productivity you have to deal with power prices,” Senator Xenophon – who holds three crucial votes in the upper house – said at The Australian Financial Review Business Summit on Wednesday.

“If by holding off discussions with the government on company tax cuts until the issue of power is dealt with substantially sharpens their thinking and a gives them a greater sense of priority to deal with the power crisis then so be it.”

His comments came as the Australian Energy Market Operator sent shockwaves through the government by warning of a shortfall in gas-fired electricity generation in NSW, Victoria and South Australia by the summer of 2018-19 unless new supply is brought on-line as soon as possible.

The closure of Hazelwood is a problem. Victoria and NSW have much more spare capacity than the peripheries of SA and QLD but most of it is gas-powered which can’t be obtained at viable prices, and some of it is old as well so the more pressure it is under the more breakdowns we’ll see. Load shedding may well spread to Victoria during bad weather events.

The fix remains twofold. Short term, the gas cartel must be broken to drop prices to release idled gas-powered peaking electricity supply. Plus Arrow must be force developed. Longer term, the NEM requires reform to bring it into line with new power sources. And a bipartisan emissions trading scheme would dramatically accelerate gas and storage investment to bring to bear as further peaking power solutions.

On the first, rather than break the cartel, the Do-nothing Government is busy instead trying to tax the gas sector via reform to the PRRT. That’s going to backfire horribly as higher taxes will be immediately passed on to customers. Credit Suisse has already shown it what it should be doing instead:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31

■ If these contracts were then all diverted domestically, at US$65/bbl oil, they should deliver gas at Wallumbilla at $7.50 gj. This is highly competitive gas in the current environment we think and should certainly not be considered unreasonable by domestic buyers

■ Importing LNG: AGL has now very publically disclosed its plans to look at using floating regas to import LNG into Australia. Whilst many believe this is just a negotiating tactic with buyers, we are less convinced. That said, with AGL rightly unlikely to want to take price risk, this might be more about targeting seasonal markets than providing 10-year supply agreements with industrial buyers. Even if one contracted off Henry Hub and used a long-run price of US$3/mmbtu, it would be landing in Australia at >A$10/GJ. Post transportation costs this could again be unmanageable for many domestic buyers of flat, term contracts. Importing LNG could be key in targeting seasonal (winter) spikes though

■ Reducing red tape, lifting moratoriums and stricter use it or lose it policies: Policy has an enormous role to play, partially short term, but in particular long term. Projects need to be made cheaper and quicker to bring to market and companies need to be forced not to sit on assets

■ The ultimate aim, from a national perspective, has to be to get the domestic market in surplus again. As witnessed in the US, the multiplier effect of having cheaper, relatively stable and plentiful gas supply has a material multiplier effect on the economy. Clearly producers would rather a tight, even undersupplied market, but with the right frame work in place (which it clearly isn’t at the moment) a more equitable and profitable industry could exist for all parties. Even with a sledge hammer, breaking the camel’s back appears the hardest thing at this stage

On the second, with the interim Finkel Report already backing an EIS, the government is itself starting to look awfully isolated in its bizarre attack on renewables and love of coal. The final report will very likely come out with similar very shortly, and if so, will also recommend reform to the National Energy Market (NEM) over any push backwards in time.

Thus Do-nothing Malcolm’s crazed Enron moment has once again gotten it caught on the wrong side of the politics of a major national interest issue (rather reminiscent of its negative gearing efforts). We know how its “open for business” morons are going to react to much needed domestic gas reservation (the utterances of alien anal-probing victim Resources Minister Matt Canavan are a good illustration). Moreover, the NEM is only in this position owing to the bastard politics of the Coalition’s troglodyte rump (after it trashed the carbon price and stopped investment) and it is going to have another conniption when Finkel delivers the bad news that reform is the way forward. How is Do-nothing Malcolm going to back-flip amid this? He won’t, leaving him fighting his own background, a report by his own scientist, as well as half of his party, all of the states, all of the companies and all of the people as he throws pork at Pauline Hanson’s coal. Well played, sir!

It looks like the Coalition’s power crisis, which it has created through bastard politics over two governments, is set to get materially worse before it gets better. We can perhaps take some small comfort from the fact that it will destroy it too.