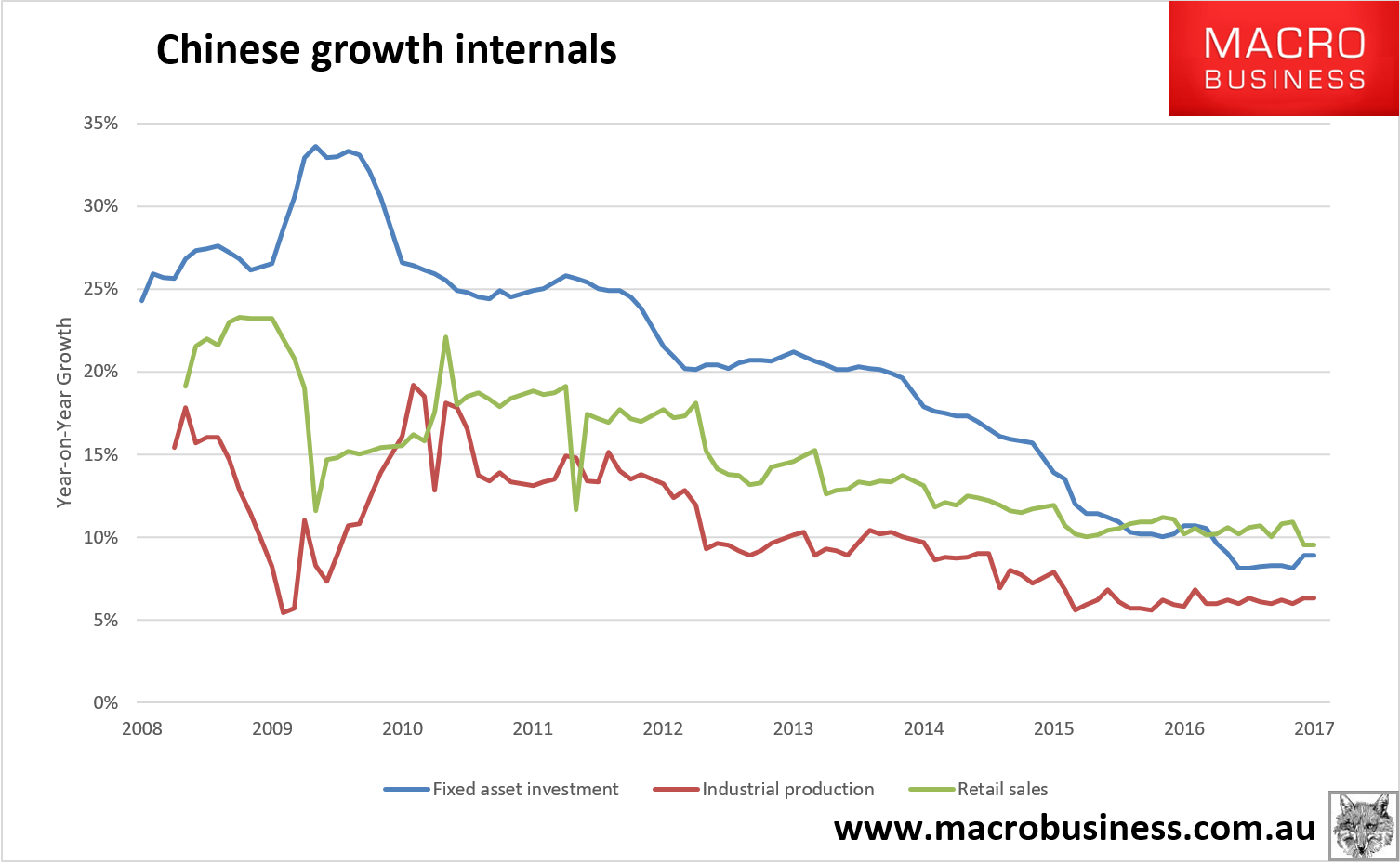

China’s January/February data is still cruising with industrial production in at 6.3%, fixed asset investment 8.9% and retails sales 9.5%:

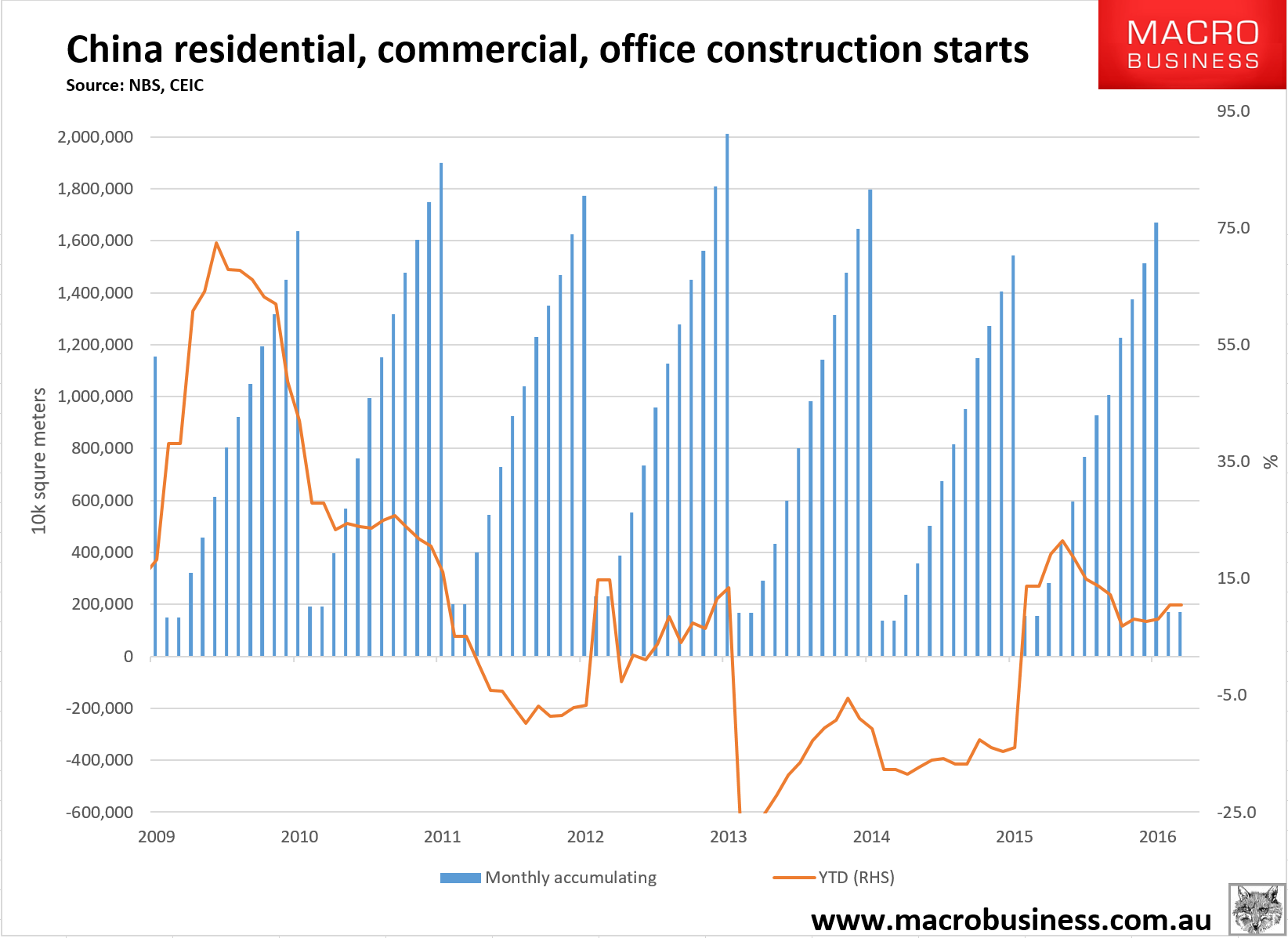

All important construction starts were solid up 10.4% year to date:

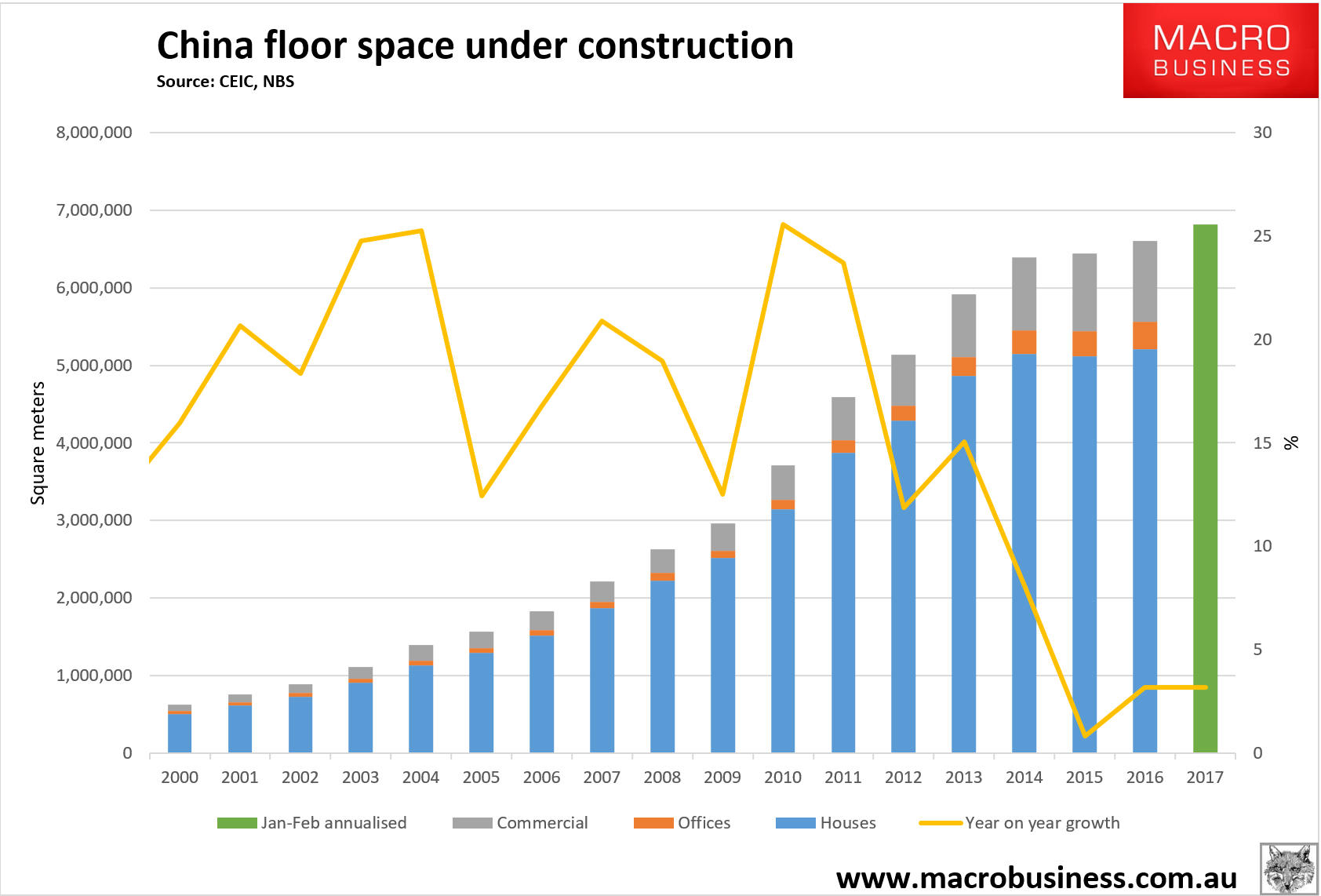

And floor area under construction began the year solidly up 3.2% year to date, the same as the 2016 full year:

However, both floor area figures are much lower growth rates than the comparable months in 2016 so there is a clear deceleration in the rate of change. This suggests that we’ll probably be looking at down a little for the full year in ten months time.

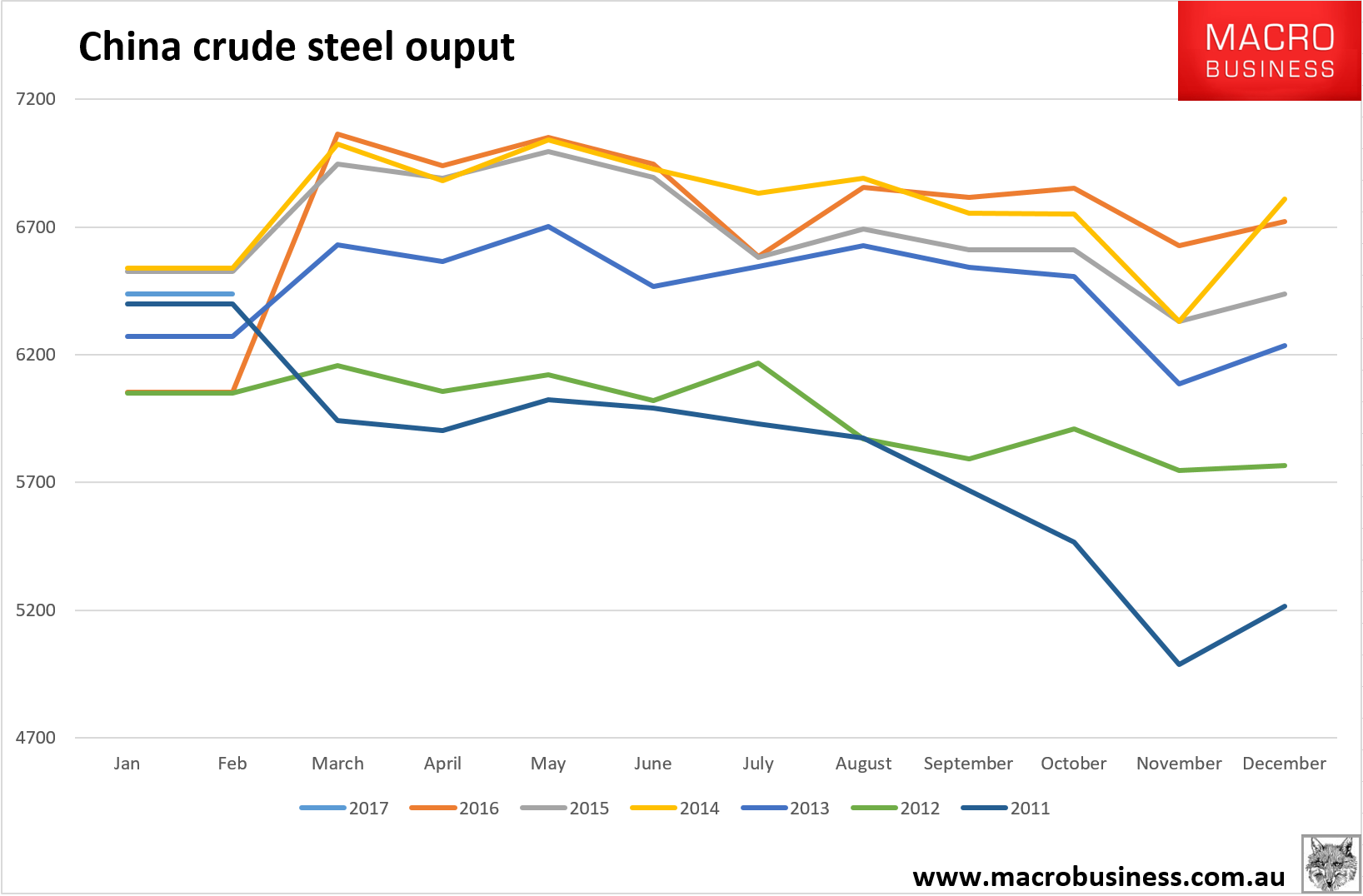

Turning to steel, the numbers were surprisingly weak at 128.77mt for the two months. That’s up 5.8% on last year’s very weak start but a decent fall from last year’s second half printing repeated record months:

I expect we’ll the year up a little but see a fade in H2.

Nothing here to change my view on anything. China still sailing along fine and the pipeline is full enough but the stimulus impact is waning in second derivative terms and I expect it to continue to do so through H2.

The usual Q1 caution applies.