Via SCMP:

The Chinese central government has added a new line in the final version of its annual work report, pledging to curb surging property prices in big cities, as home prices in central Beijing rise to levels on par with Hong Kong.

A day after the revised government work report was published, the Beijing municipal government announced new measures to discourage home buying, including raising down payments for most property deals for second home purchases to an unprecedented 80 per cent.

The added pledge to curb housing prices was one of 78 revisions to the final version of the government work report since Chinese Premier Li Keqiang read the initial version to the National People’s Congress two weeks ago.

“Containing excessive home price rises in hot cities” is listed as one of the key tasks this year, according to the finalised document released by Xinhua on Thursday. The document will serve as a guideline for the central government this year.

The way that this usually works is that the bubble just keeps running right through buyer curbs until monetary policy gets serious. This time, however, the buyer curbs have been monetary for the first time so have had a much more material impact.

I have thought for some time that the Chinese are aiming for a different cycle this time. Given mortgage and household debt is very low, it is an obvious lever to pull to keep growth high while it seeks to restructure other over-leveraged parts of the economy like SOEs. The growth impacts of keeping property ticking over are obvious, via Deutsche:

- The property and construction sectors accounted for 33% and 15% of local government tax revenue growth between 2010 and 2015. They contributed 43% of local government tax revenue in 2015, compared to 11% from manufacturing (Figure C3). Besides taxes, local governments also heavily rely on land sales to finance infrastructure projects

.

- Banks, developers, urban property owners, and government all benefited tremendously from the property sector so far. This makes it difficult for the government to tighten monetary policy or roll out straightforward measures such as property tax to contain the bubble. The reluctance to prick the bubble only makes it larger.

- The government may have the confidence that they can avoid a property bubble burst. It does appear that China has a stronger control over property prices than other countries, because it has a closed capital account, high saving rate, low CPI inflation, high level of reserves, a current account surplus, monopolized land supply, and a financial system largely controlled by the government. Some may argue “why can’t Beijing and Shanghai become Hong Kong?”

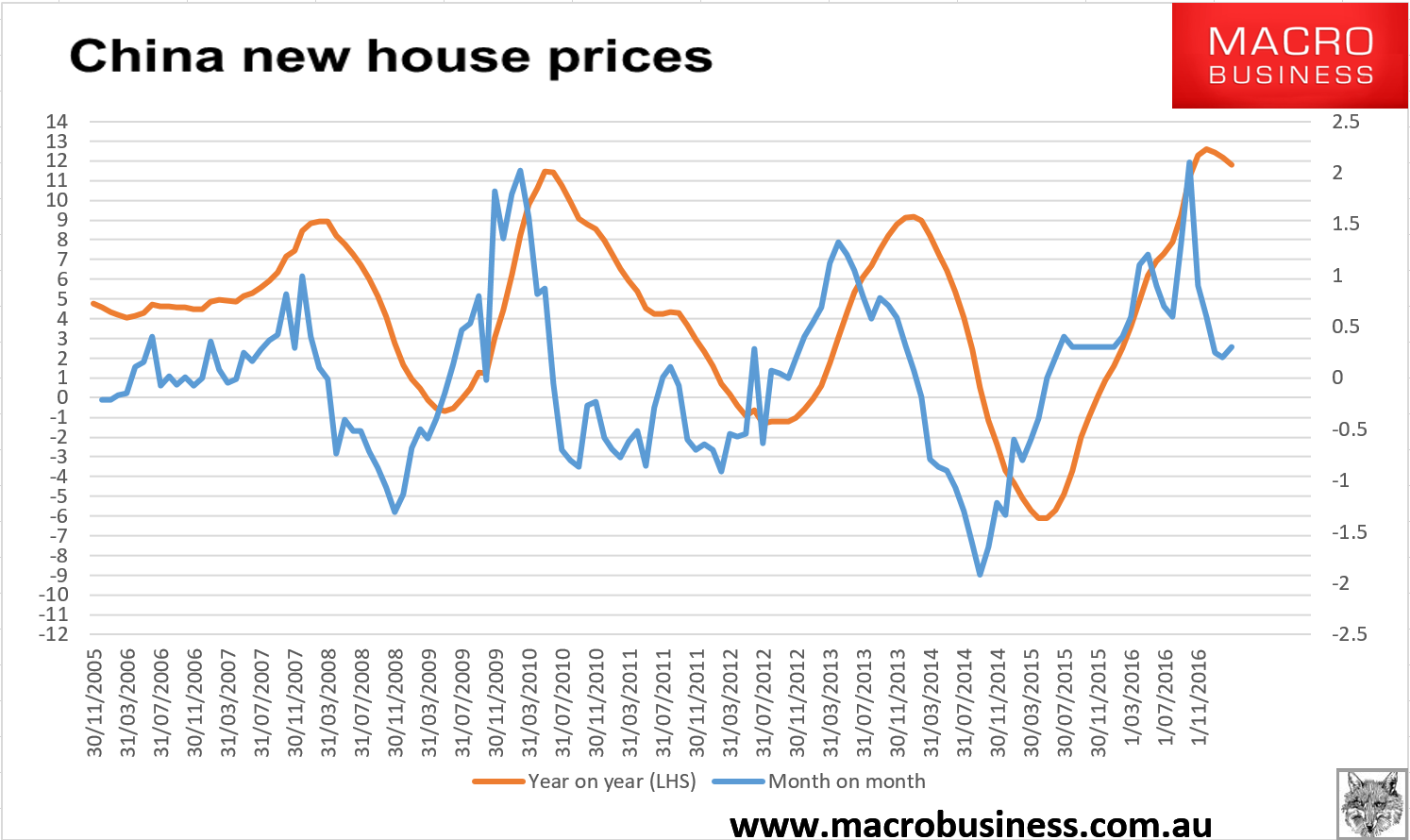

Thus my base case has been a slow slowing not a repeat of the 2015 bust. So far the evidence suggests that they’re succeeding with prices coming off only in tier one and two cities. February data was released over the weekend and showed the first acceleration in national prices in six months, up 0.3% in the month from 0.2% in February. Year on year gains fell to 11.8%:

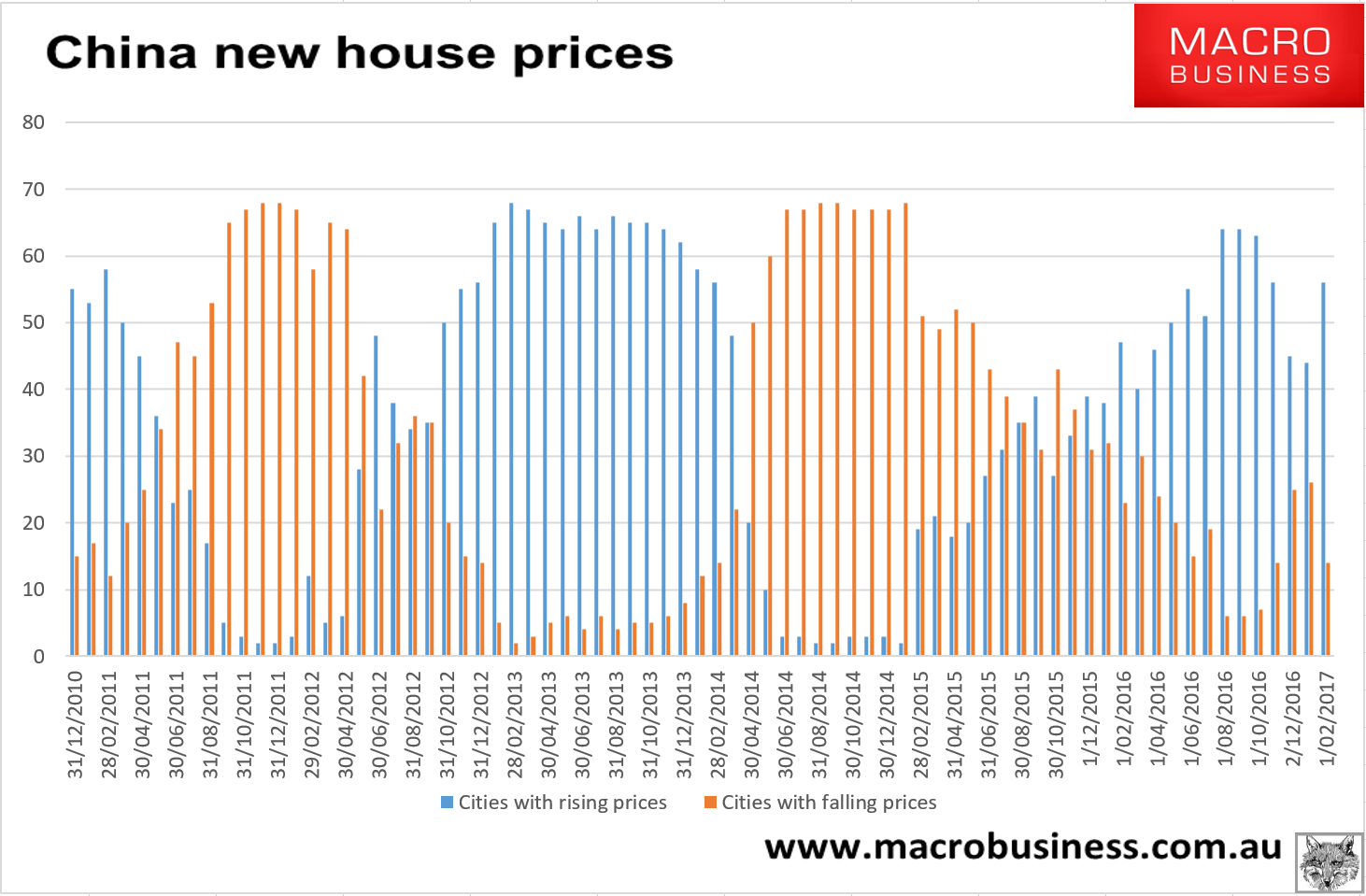

The spread of gains and losses turned bullish with 56 cities rising and only 14 falling:

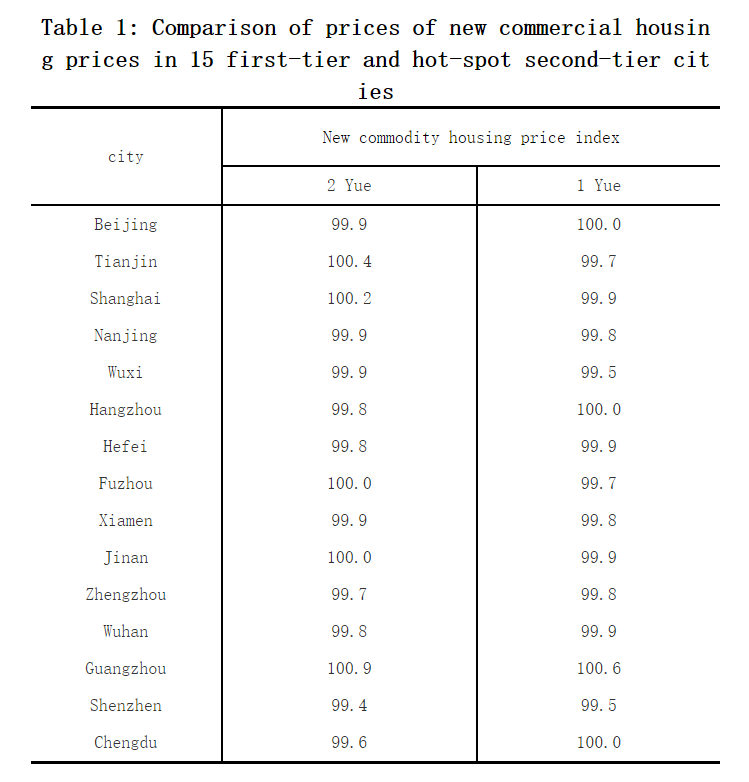

However that was perhaps exaggerated as the recently tightened first and second tier city prices are bouncing in and out of negative:

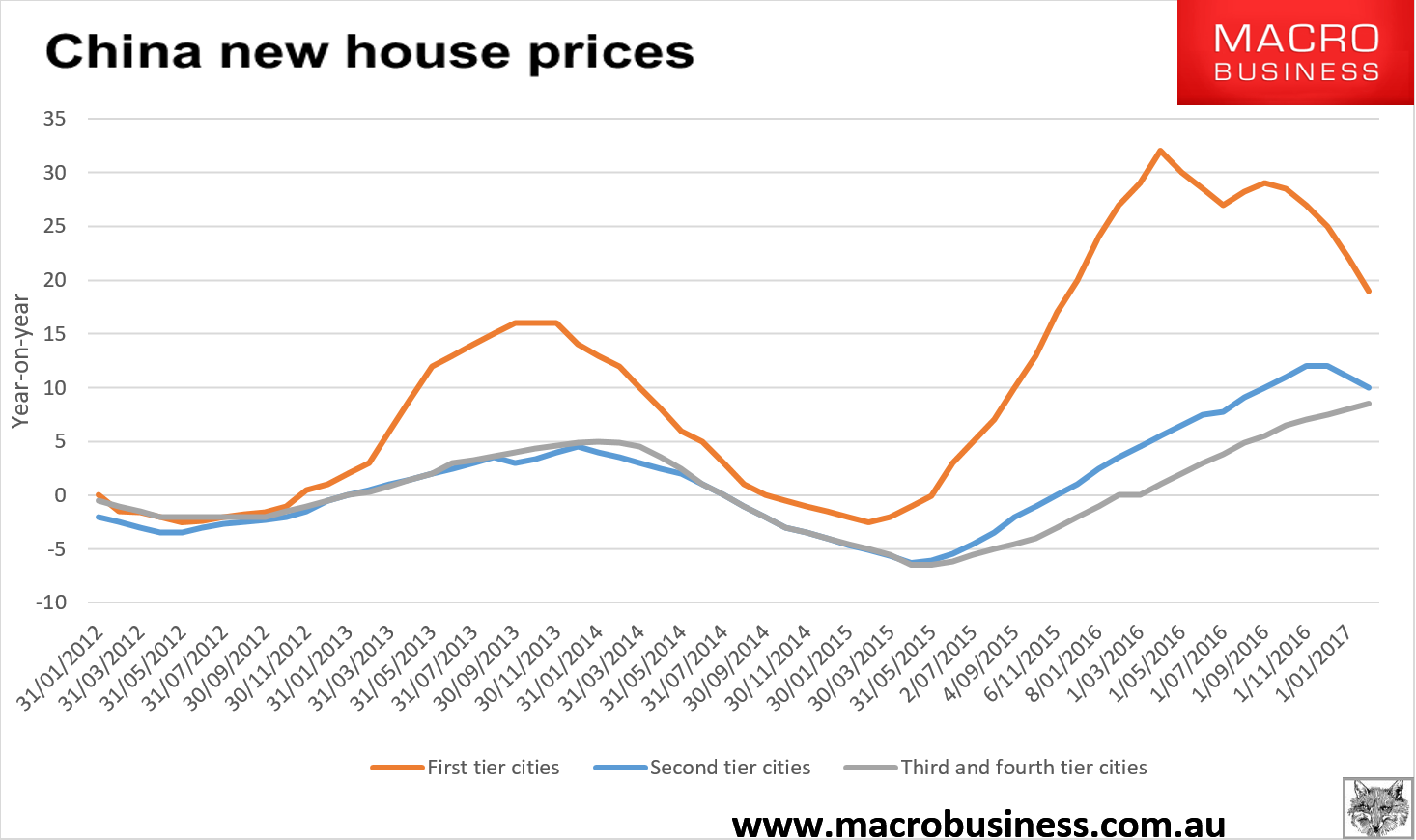

The mix continues to see top tiers pulling back fast, second tier slowing and those below traveling fine:

Going forward it’s possible that top tier cities bust and drag down the whole market. Or, like Australia, that they rebound and force still stronger curbs that risk a bust a little later. Or, it ends with sustainable bifurcation.

The jury is out.