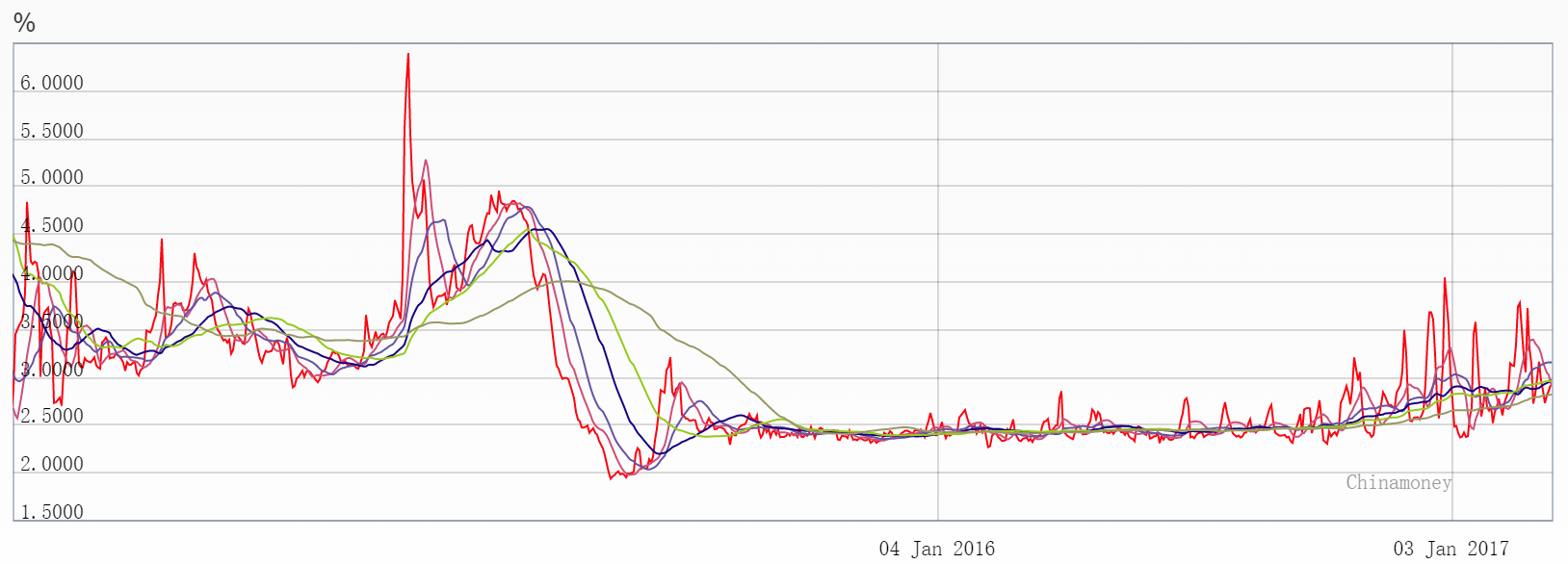

China’s central bank raised short-term interest rates on Thursday in what economists said was a bid to stave off capital outflows and keep the yuan currency stable after the Federal Reserve raised U.S. rates overnight.

The increase in short-term rates was China’s third in as many months, and came a day after the end of the annual session of parliament where leaders warned that tackling risks from a rapid build-up in debt would be a top policy priority this year.

Hours earlier, the Fed raised its benchmark policy rate, as had been widely expected, and signalled more hikes were on the way as the U.S. economy picks up steam.

“The higher U.S. rates and tightening of U.S. monetary policy could trigger further capital outflows and have some negative impact on China’s financial system,” Nomura economist Yang Zhao said.

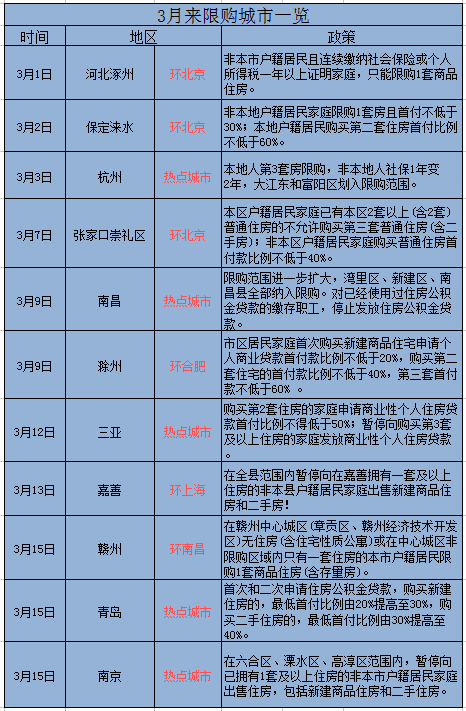

The cities are all near first-tier or second-tier “hot” cities, or second-tier cities. From top to bottom are: two Hebei cities bordering Beijing, Hangzhou, Zhangjiakou (Hebei city borders Beijing), Nanchang, a city bordering Hefei, Sanya, a city outside of Shanghai, a city outside of Nanchang, Qingdao, Nanjing.

Slowing at the margin in H2.

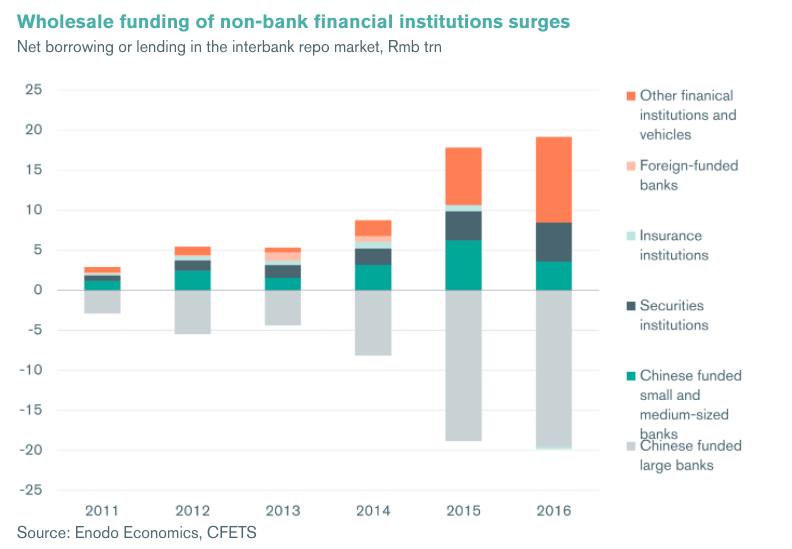

Meanwhile, another warning arrives on the debt itself, from Enodo Economics

A much bigger danger signal is the surge in interbank borrowing and lending and its dramatically changed composition. In the past two years, non-bank financial institutions (NBFIs) – such as trust and investment companies, leasing firms and asset managers – have increasingly had to fund themselves in the wholesale money markets.

NBFIs accounted for 54% of total borrowing in China’s repo market in 2016, up from just 14% three years earlier. They invest in assets that are much less liquid and often have much longer maturities.

…Even in a state-dominated financial system such as China’s, deteriorating NBFI asset quality will eventually prompt lenders to reduce risk and extend credit for ever shorter periods, heightening the danger of a mismatch of maturities. In fact, now that the authorities have managed to shift the shortage of liquidity from small and medium-sized lenders to non-bank financial firms, whose failure would carry much less systemic and reputational risk, Beijing is likely to allow more defaults. Indeed, the number of bond defaults is rising sharply, albeit from a low level.

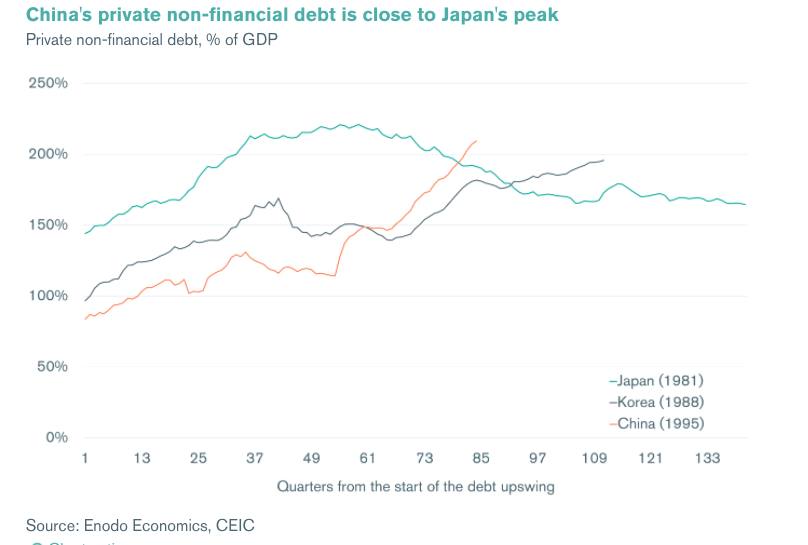

…China’s total debt has soared since the 2008 crisis as the government has poured money into unproductive investments to sustain growth. The result is that China’s non-government, non-financial debt has ballooned to an estimated 209% of GDP, almost as great as Japan’s was at its peak.

Advertisement

It can still force banks to lend to cover the gap. There will be no sudden stop to lending. There will be a progressive choking on bad loans, however.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.