From Macquarie comes analysis much along the lines of my regarding the Chinese trade data:

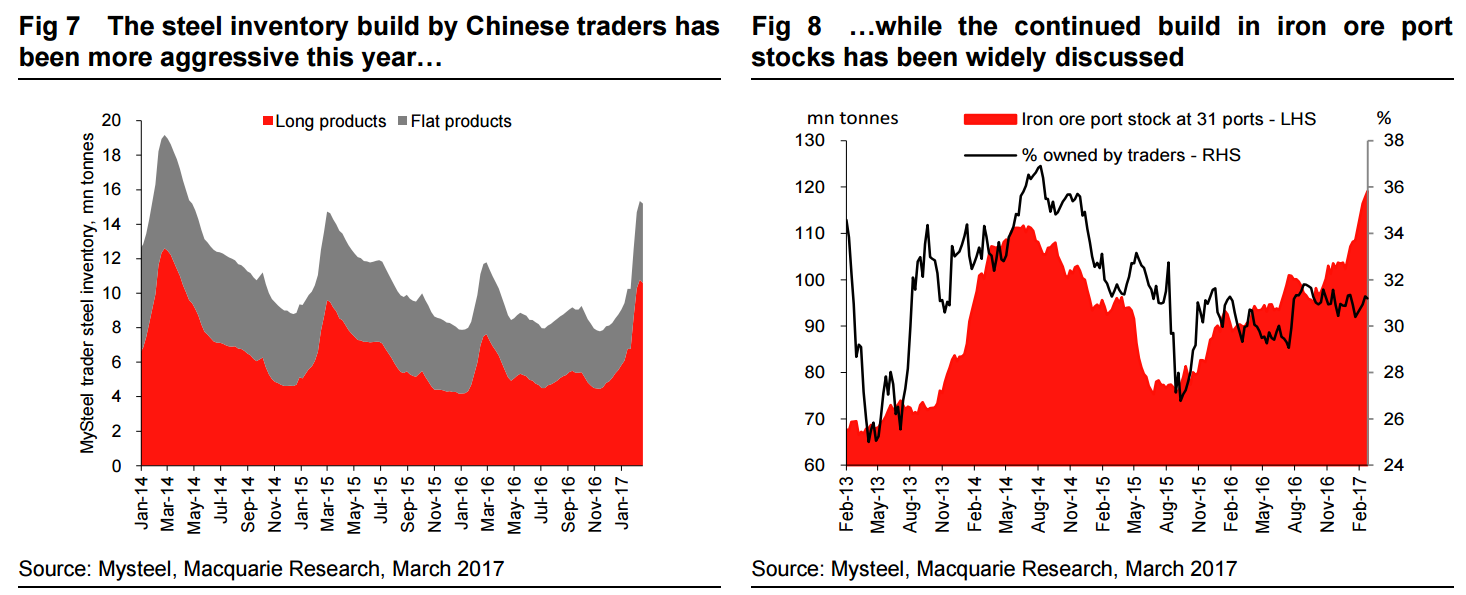

Much the same is true in steel [as aluminium], where trader inventories have accelerated quickly since the start of the year and have now surpassed peak levels seen in both 2015 and 2016. This reflects a high degree of confidence, as evidenced by our steel survey, of continued order strength in the coming months. This is essentially pure physical speculation, but has certainly been helped by more ready availability of credit than in past years. As a result, Chinese steel output accelerated strongly in early February. Meanwhile, some of the strong iron ore imports have been evidenced in port inventory gains as widely discussed by market participants. In our view, this reflects an efficient market where marginal supply has reacted to price prompts. But in any case this increased volume has found purchasers with no discernible impact of price (certainly until this week).

High Chinese refined exports are of course typically a source of deflationary pressures to global markets. The recent pullback has certainly eased these pressures. This comes at a time where developed world demand growth continues to recover. As our Global Macro team has noted, we are is now 15 months past the nadir of the global industrial production cycle and the OECD LI is now in positive territory. Indicators from metals markets continue to suggest reasonable developed world demand growth at the present time.

This combination of events should see wider reference price gains across commodities, helping the reflationary trend. And certainly, over the past few months aluminium, steel, stainless steel and other metal prices have trended higher. Given output levels are high, we reiterate that supply curtailments have not been the key reason (these will become more important from Q4 2017), but rather that apparent demand (whether through real demand or inventory build) has picked up. We would note however that, despite the sequentially weaker February data, the WSD World Steel Export HRC price actually fell in the month. To us, this highlights that two-tier commodity pricing via protectionist policy is already coming through in steel, with domestic prices generally outperforming still oversupplied export markets, despite China’s pullback. This should be somewhat of a red flag for steel producers exposed to the export market.

Given the level of inventory build in China, demand now has to pick up strongly to pull this material through the chain. However, while demand is clearly significantly better than this time last year, current indicators aren’t showing the aggression we might have expected from the strong sentiment seen over 2017 to date. Indeed, there seems an increasing chance that demand is undershooting what were admittedly high expectations. Recently, copper premiums have dropped back to minimum warehouse offering levels. Physical market prices are below SHFE in many cases, while just this week the iron ore price looks to be cracking. The argument could be made that the post-New Year end-user ordering was being delayed until after the assemblies held last weekend, but with the government clearly starting to worry more about inflation and tightening policy at the margin, sentiment is likely to be weakening. We reiterate that in the view of our Chinese Economist Larry Hu, we are passing through the peak of China’s growth cycle with headwinds likely to be seen over Q2.

When inventories are high, this situation poses a potential problem. We will be tracking how quickly visible inventories are being run down over the coming weeks as a gauge of whether demand is meeting expectations. In particular, we will be looking at the downward gradient of steel trader inventories relative to past years. If this is at normal pace, worries may again dissipate. If slower than usual, traders will stop ordering from mills, mills will shift from expecting output growth to output declines, and iron ore may suffer another of its periodical whiplashes. As always seems to be the case at this time of year, incremental Chinese commodity-related data points will be closely scrutinised for a gauge of wider economy health.

It’s really only a case of how swiftly we deflate now…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.