Via Marty North:

Genworth released their notice of the 2017 Annual General Meeting today, to be held on 11 May 2017. They are reacting to the changing market conditions, with lower LMI volumes at lower LVR’s.

Of note is Resolution 4 which asks shareholders to approve an on-market share buy-back of up to 125 million of the Company’s issued ordinary shares, over a period of up to 12 months form the data of the 2017 AGM.

We were previously advised that the Genworth was evaluating the potential to deploy and excess capital towards profitable opportunities that would enhance the return profile of the business and in the absence of those, capital was to be returned to shareholders.

Given that the Companies regulatory solvency ratio continues to be above the board’s target capital range of 1.32 to 1,44 times the PCA, and is expected to remain so, buy-back is an option.

Shareholders are required to approve the buy-back thanks to the 10/12 rule limit. They will also have to comply with ASX listing rules and approval of APRA.

There is no guarantee the Company will buy back the full number of shares. Currently there are 509,365,050 shares.

They say excess capital may also be deployed to:

• enhance the return profile of the business;

• pay dividends in excess of profits earned;

• undertake a capital reduction;

• reduce Tier 2 capital; or

• reduce reinsurance.These alternatives will continue to be evaluated.

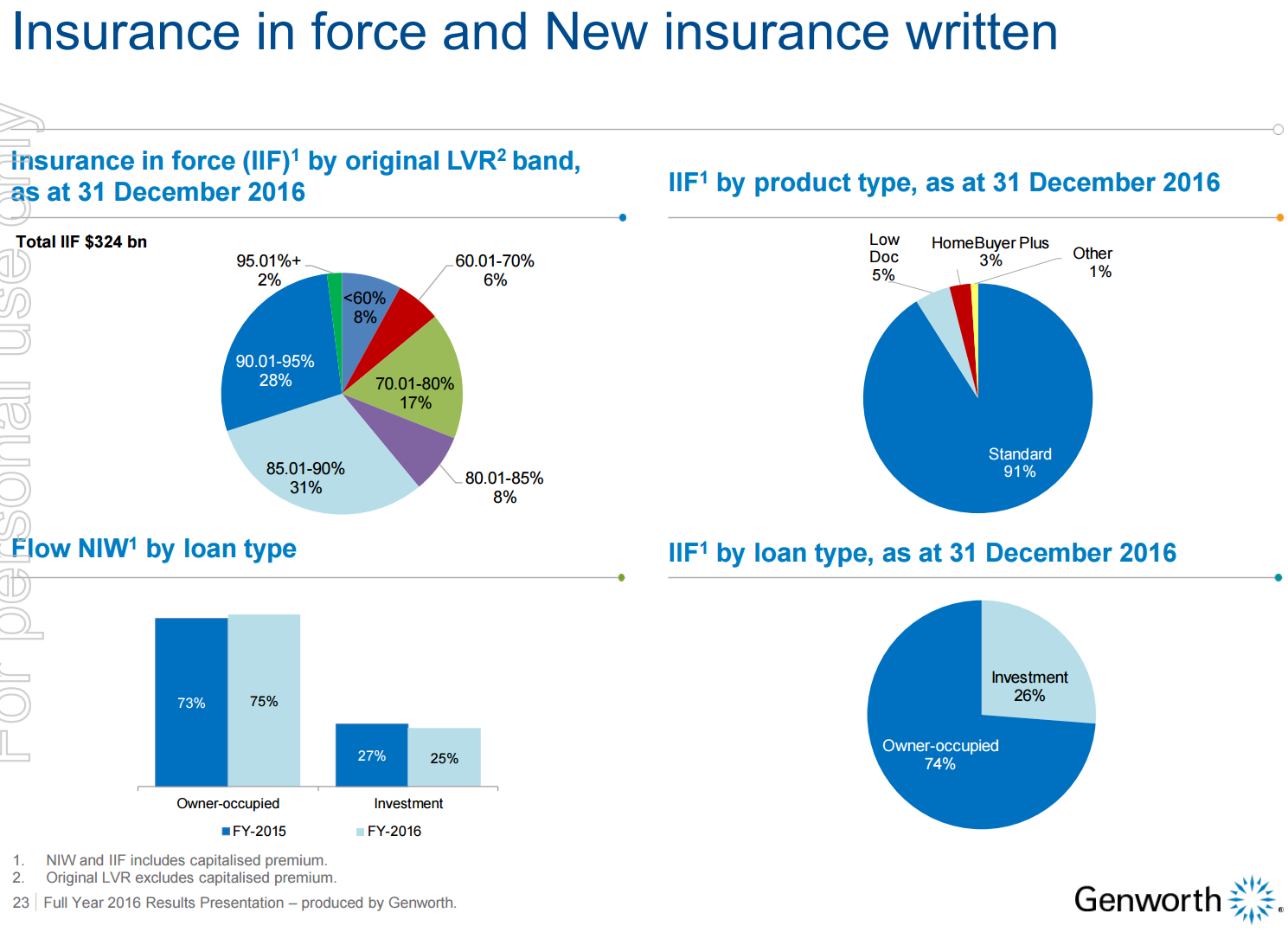

Fair dinkum, if there is one firm in Australia right now that is the walking dead trading on implicit public guarantee it is this mortgage ponzi scheme. Here’s its last reported insurance in force:

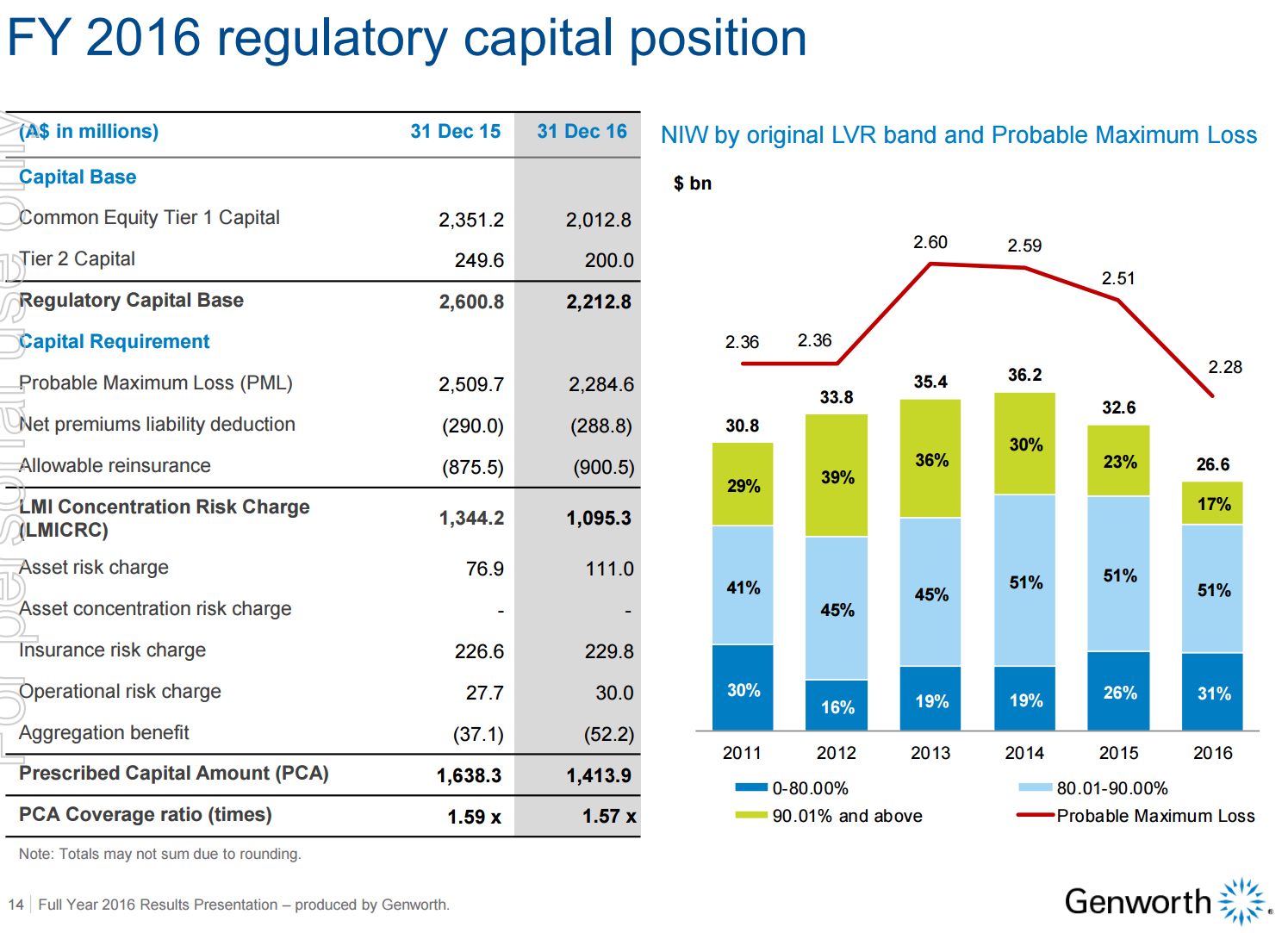

That is $324bn of high LVR mortgage insured. And its regulatory capital position:

That’s 324bn of loans insured against a capital base of $2.2bn. Which, you may feel reassured, is actually 1.57 x more than the capital it is required to hold. Hence it is mulling leveraging up by giving away some more cash.

A dead parrot can see that the moment the Aussie housing bubble pops this capital is going to evaporate overnight and, as markets refuse to cough up further equity, the taxpayer will step in and channel billions upon billions into the banks, ala AIG in the GFC.

That we can let thing throw away money now is only a measure of the lunacy of the system.

Giddy up!