Today’s jobs numbers surprised the market to downside, with employment falling by -6k jobs in February (market had 16k) and the unemployment rate rising to 5.9% (market had 5.7%). Once again, the official labour force survey is not aligning very well with the other indicators of employment or the broader economy. In particular, the official survey shows much weaker jobs growth than implied by the business surveys and job advertisements, which both look positive. Given the various measurement issues in the official survey we have tended to put more weight on the other surveys of labour market conditions in recent years. Nonetheless, with the official labour market numbers clearly showing that there remains spare capacity in the labour market, talk of RBA rate hikes any time soon seems premature. We see the RBA on hold in 2017 and lifting its cash rate in Q1 2018.

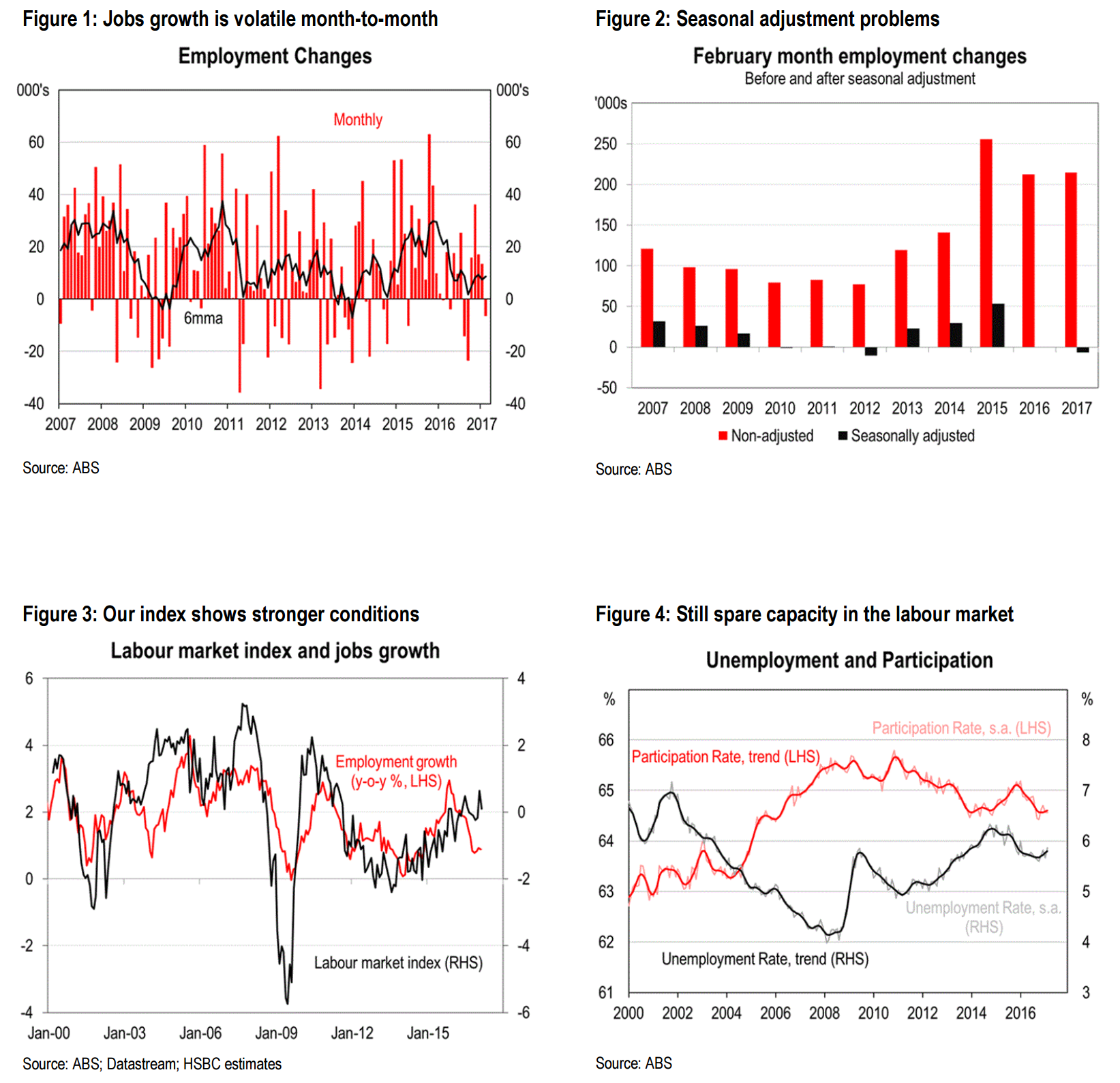

The Australian labour force survey has had measurement issues for quite some time now and today’s print, once again, highlights some of these. Given our concerns about the official survey we have, in recent years, put more focus on other surveys of the labour market. These other surveys are currently showing more favourable labour market conditions than the official survey. To start with, it is worth pointing out that the official survey has always been volatile (Chart 1). Employment growth in the Australian labour force survey is far more volatile than the US payrolls survey, for example. Over recent years, however, problems with seasonal adjustment have made the numbers even more unreliable. Of particular concern in today’s numbers was that the nonseasonally adjusted employment figure for February was the second strongest in the history of the numbers and yet the seasonally adjusted number showed a fall (Chart 2). Our own index of labour market conditions – which aggregates the survey of job advertisements, the NAB survey’s employment conditions component and the unemployment expectations component from the monthly consumer sentiment survey – shows a very different trend to the official numbers (Chart 3). Our index shows a gradual and continued improvement in the labour market over the past year, while the official survey shows a significant cycle.

Nonetheless, we agree that the labour market still has spare capacity. This is made clear by the unemployment rate having broadly tracked sideways over the past year (Chart 4). It is also evident in the weak wages growth. However, consistent with our labour market index we see spare capacity gradually being absorbed and expect that this will provide support for wages growth over coming quarters. The RBA has already noted that its own liaison program suggests that wages growth is stabilising. We also see it as likely that some part of the sharp rise in national incomes, which has been driven by higher commodity prices, will gradually feed through to household incomes over coming quarters.

The last three years appear consistent in seasonal adjustments but not before that. If the switch in method has now washed through the annual result then its a non-issue. Good luck with those wage rises.

JP Morgan’s Tom Kennedy calls it an “unambiguously weak” report:

Importantly, the unemployment rate is now just 0.1 [percentage point] below the upper end of the RBA’s forecast range, meaning any increases from here will likely cause the RBA to rethink their outlook for monetary policy

The weakness in annual full-time employment growth continues to be borne out in the underemployment rate (the number of underemployed workers expressed as a percentage of the labour force), which popped higher in February and is now tracking at all-time highs again. As we have previously mentioned, wage growth since 2013 has held a strong negative relationship with the underemployment rate, so today’s pop higher makes the RBA’s objective of engineering a sustained up-tick in core inflation all the more difficult.

We still see the cash rate biased lower in Australia. While this might take some time to play out, today’s data are a salient reminder that underlying fundamentals in the Australian economy are certainly not consistent with higher rates anytime soon.

On a similar line, Citi’s Josh Williamson writes that labour market weakness is “a warning to RBA hawks”:

Ongoing spare capacity in the labour market portends continuing sub-trend wages growth. The February data keeps the rolling average three-month unemployment rate around 5¾%. This is about 0.75ppt above what the RBA views as full employment.

Reducing the gap requires a pick-up in GDP growth. However, GDP growth is not strong enough to lift employment growth to a speed that will do so. Furthermore, the earlier pick-up in yearly employment growth now looks out of place.

Market pricing for RBA rate hikes needs to be pushed well into [2018], in our view.

ANZ economist Felicity Emmett writes:

The February labour market report disappointed, with a fall of 6.4k jobs and a rise in the unemployment rate to 5.9%. The detail was slightly more positive than the headline with full-time jobs rebounding after the previous month’s sharp fall. The weakness in the report is at odds with still solid business conditions and ongoing gains in ANZ job ads, and in our view some improvement is likely over coming months.

UBS’s George Tharenou agrees that lead indicators suggest employment could improve in coming months:

Overall, the trends in the labour market over recent months show ongoing modest jobs growth. However, the unemployment rate jumped to 5.9%, which combined with weak hours, saw the broader underutilisation rate surge to only just below a 2-decade high, indicating significant labour market slack, consistent with our view of low inflation & wages.

That said, lead indicators of employment still suggest better jobs growth over coming months (~1½ – 2% y/y). Nonetheless, for now, the labour market data strongly argues against growing calls for the RBA to hike (UBS’s forecast if for rates on hold ahead).

Capital Economics’s Kate Hickie:

While we are wary about reading too much into a single monthly move, given that the fall in employment followed only modest gains in December and January, it sends a worrying signal about the current momentum in the labour market.

What’s more, although full-time jobs rose by 27,100 in February, that wasn’t enough to reverse the sizeable 44,100 fall in January. Indeed, it is still true that on net all of the jobs created in the past year have been part-time ones.

All told, it is clear that there is still plenty of slack in the labour market, which supports our view that wage growth will remain subdued for a few years yet. · Looking ahead, we expect employment growth to remain modest and the unemployment rate to remain around 6.0% this year. That said, in this low underlying inflation environment, if the unemployment rate were to rise notably this could be enough to prompt a further rate cut by the RBA, particularly if concerns about financial stability ease.

Westpac’s Justin Smirk:

This is a much weaker than expected result and we would argue confirms that the labour market, as reported by the labour force survey, is on a much softer than expected trend. Business surveys have continue to strengthen in 2017, an observation supported by the robust update from the Q1 Australian Chamber/Westpac Industry Trends survey released this morning, and are pointing jobs growth of around 2%yr currently potentially accelerating to 2¾% by Q3. The –6.4k print in February left the annual pace of employment growth flat at 0.9%yr.

Some may be tempted to make a positive spin on the +27.1k jump in full-time employment. However, we would rather not make too much of the extreme switching between full-time/part-time you can get from month to month. Instead, we highlight the 1.2% monthly decline in hours worked (–0.5%yr) to argue this is a soft update.

By state there was a big jump in unemployment in Vic (6.1 from 5.8%), Qld (6.7% from 6.3%) while there was a modest lift in NSW (5.2% from 5.1%). The unemployment rate did fall in WA but given that total employment also fell (5.5k) the fall in unemployment is more about declining participation than a stronger than expected labour market.

A full Economic Bulletin will follow shortly. At this stage we see the February Labour Force Survey confirming that the labour market continues to underperform relative to other labour market indicators and is, at least for now, set to remain a drag household incomes.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.