The Reserve Bank Board meets next week. It is certain to keep rates on hold.

The minutes of the March board meeting were less upbeat on the economy than we had seen in previous assessments from the Governor.

While I was meeting with customers and officials in South East Asia and China, my colleagues assessed the minutes as “The overall theme is still of upside risks from global growth and commodity prices near term but a likely muted pass through to local conditions and question marks beyond 2017”.

Readers will be aware that our central theme for the Australian economy has been for slightly above trend growth in 2017, partly reflecting the boost to the terms of trade and the ongoing construction boom, to be followed by an abrupt slowdown in 2018 as construction contracts and the terms of trade reverse.

With the Reserve Bank sharing our caution around 2018, along with ample capacity in the labour market (unemployment rate is 5.9% compared to full employment rate of 5.0%) and stubbornly low wages growth, there is only scope to cut rates.

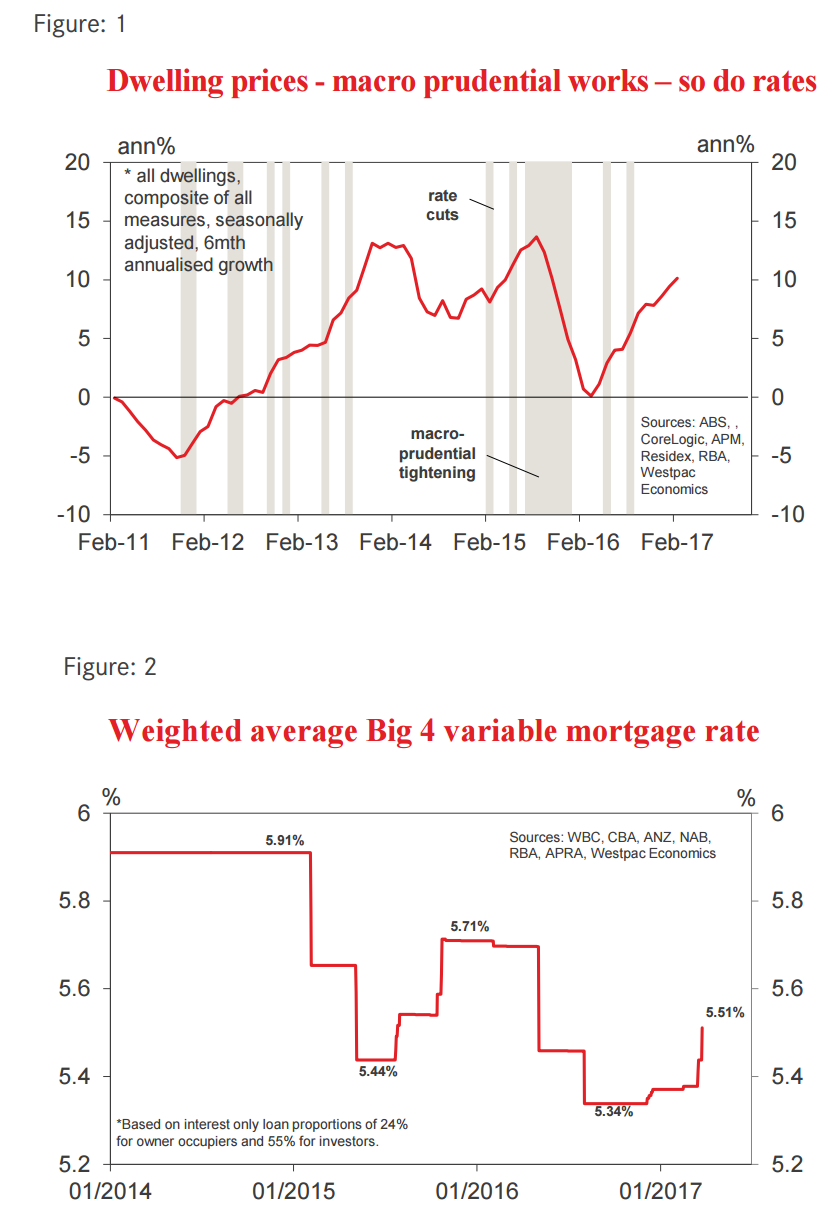

But as we have argued consistently, a resurgent housing market disallows such a policy option. Indeed, the minutes refer to “a build- up of risks associated with the housing market”.

Macro prudential policies seem imminent. The next RBA Stability Review on April 13 may provide more clarity. With the use of growth ceilings for investors proving to be a successful policy in 2015, another “round” of macro prudential policy seems highly likely. Limiting growth in the stock of investor loans to say 5% versus the current 10% guideline is a reasonable possibility (this has been recently canvassed in the media as one possible tool).

Figure1 shows how successful this policy was, being associated with a sharp slowdown in house price appreciation in 2015.

However, those direct controls on lending volumes were complemented by interest rate adjustments by the banks themselves. Figure 2 shows our estimate of the changes in the weighted average of the variable mortgage rate (including investors and owner occupiers) in 2015. We estimate that during that period, the weighted average rate lifted from 5.44% to 5.71%. Of course, that lift was more than fully offset by subsequent rate cuts by the RBA in 2016, pushing the weighted average rate down to 5.34%.

As we see in Figure1, that cut re-ignited house price growth as well as auction clearance rates and new lending.

The RBA has already been given a “start” in this current cycle, with the weighted average rate lifting from 5.34% to 5.51%, largely reflecting increases in investor rates by the four majors. Complementing these rate adjustments with a more constraining restriction on new lending to investors is likely to yield a comparable response in house prices to what we saw in 2015.

By year’s end, the RBA’s concerns with “a build- up of risks associated with the housing market” are likely to have eased.

As we move into 2018, despite ongoing rate hikes by the Federal Reserve, the Reserve Bank, troubled by low inflation; on-going spare capacity in the labour market; and weak wages growth might be tempted to ease policy further.

However, the “lessons” of 2016 will have been learnt – do not risk re-igniting house prices – and a more prudent approach will be to rely on the currency to provide the boost to activity.

From our perspective, a reversal of the commodity price boom of 2017, coupled with Australia’s cash rate falling below the US, is likely to yield a sharp lift in Australia’s competitiveness.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.