… there appears to be adequate protections available to consumers afforded by the law to shield against fraud. If regulators were abiding by their mandates to protect consumers from fraud perpetrated by lenders, the risks of becoming a victim of having being sold a fraudulent financial product (i.e. a predatory and unaffordable mortgage) should be close to zero.

Unfortunately, our research into the mortgage market and banking system provides evidence to suggest many borrowers have or are at risk of becoming a victim of fraud, committed by lenders…

The reason Australians face a high risk of becoming victims of financial crime is due to the intentional disregard by our regulators to investigate and enforce the law in the case of serious instances of financial crimes committed by our politically and economically powerful lenders. Put simply, the CommInsure and BBSW scandals are the equivalents of parking tickets versus systemic, widespread fraud in our $1.6tn mortgage market.

LF Economics also provides examples of where Australia’s financial regulators have been derelict in their duties to protect consumers, and provides several recommendations:

Example 1:

Using the mortgage market as an example, we argue ASIC has deliberately refused to conduct an investigation into credible evidence gathered by Australia’s leading financial consumer activist and President of the Banking & Finance Consumers Support Association (BFCSA), Denise Brailey. The BFCSA has uncovered over a thousand loan application forms (LAFs) shown to be altered by lenders to inflate the assets and incomes of borrowers to issue predatory and unaffordable mortgages.

ASIC has also received many claims by alleged victims that lenders have fraudulently tampered with their LAFs. Unfortunately, ASIC has refused to investigate even one of these claims, let alone conducting a thorough and systemic analysis of the mortgage market…

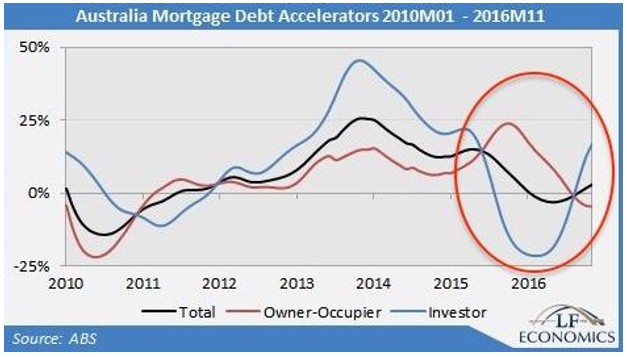

Example 2:

Following APRA’s implementation of its macro prudential control to stem the growth in property investor debt by limiting it to an annual maximum of 10 per cent, the data in the figure suggests there was an extraordinary decline in lending to property investors as lending to owner occupiers escalated.

After off-the record discussions, it was brought to our attention that lenders began to classify an increasing number of property investor loans as owner-occupier loans. Depending on the circumstances, this was done either with or without the knowledge of the property investor. It was therefore possible lenders could claim to be keeping to APRA’s limit when, in reality, lenders have intentionally mislabelled mortgages. Either lenders feel comfortable enough to lie and know APRA isn’t going to punish them or APRA is fully aware of this behaviour and has no interest in penalising lenders…

The failure of our regulators to identify, investigate and prosecute cases of fraud should be of concern to the committee and the public. It is the opinion of LF Economics the regulators have an unspoken agreement to not investigate allegations of mortgage fraud, especially those stemming from the major lenders…

Conclusion

We would like the committee to consider our recommendations in the submission to the PWCC. To conclude, our arguments are:

(1) There is the strong probability that widespread fraud is taking place in the mortgage market;

(2) There are already sufficient laws and regulations to defend consumers, borrowers and investors from fraud;

(3) The government, regulators and other relevant public organisations have been unwilling to investigate and prosecute lenders, and

(4) Under these circumstances, changing and/or adding to the regulatory framework will do little to protect consumers from the predations of lenders.Nice work boys.