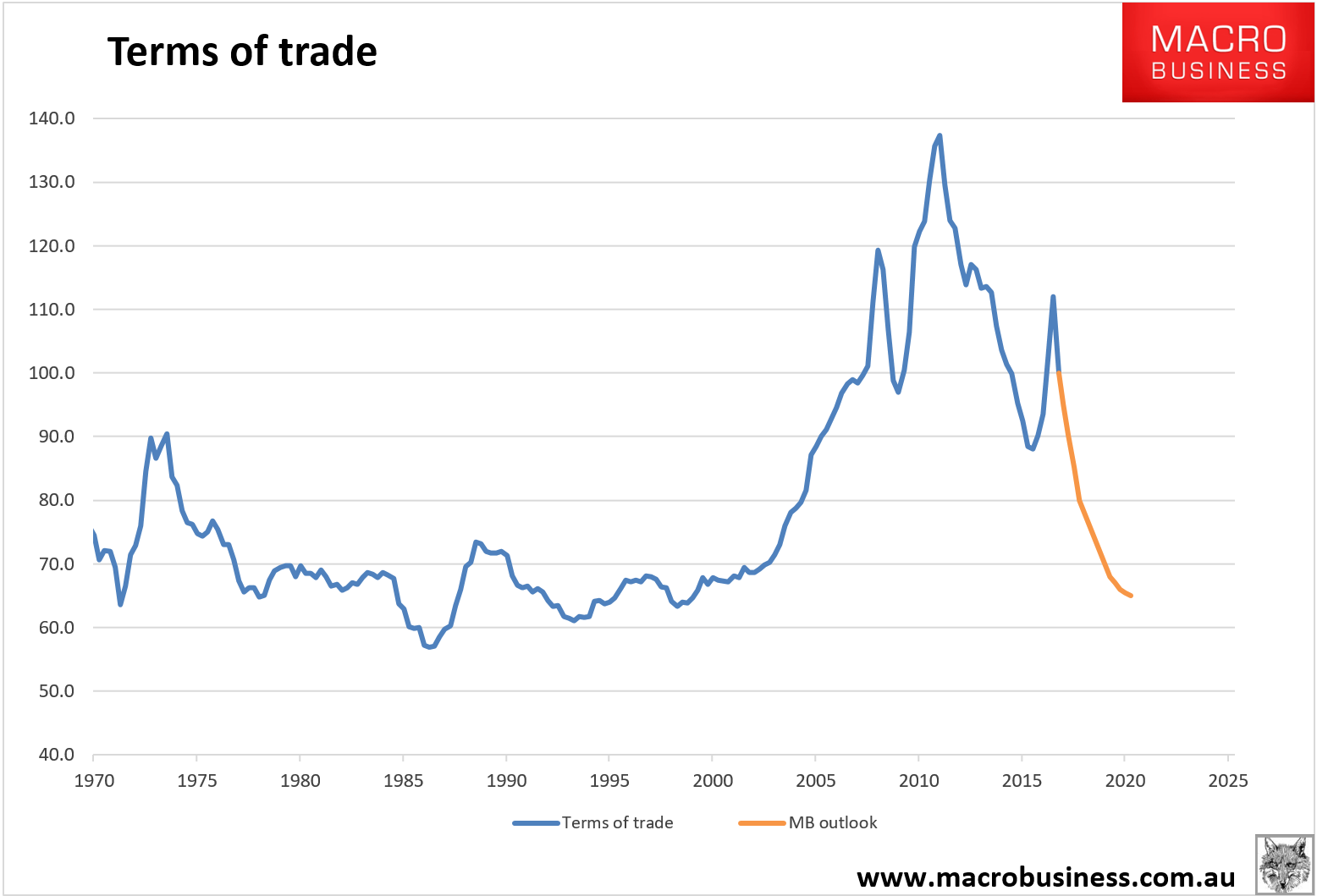

The next big shock in Australia’s lost decade is rolling down the pipe. It’s one we’re quite familiar with since it’s the same one that hammered the economy in 2015. It’s more terms of trade carnage as the iron ore and coal boomlets go comprehensively bust.

Let’s figure out where we are today in the great terms of trade bear market. With contracts lagging spot we can already estimate both the March and June quarters which will show an huge spike and then bust quarter to quarter:

From the June quarter it is all down hill again. Why?

Advertisement