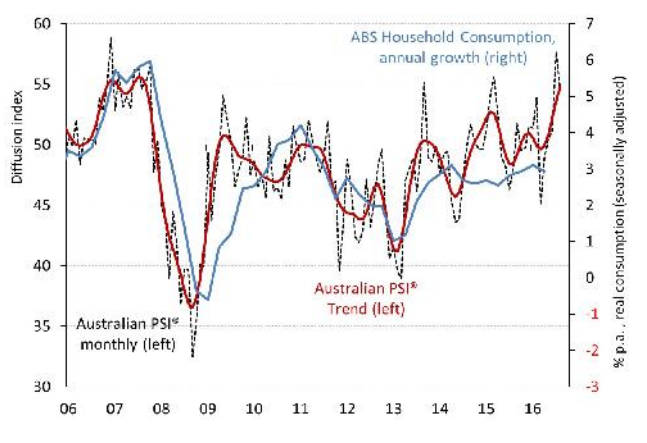

The Australian Industry Group Australian Performance of Services Index (Australian PSI® ) continued to expand in January but at a slower pace than in December, with the index dropping 3.2 points to 54.5 points (results above 50 points indicate expansion, with higher numbers indicating a stronger rate of expansion). This marks a third month of growth following three months of stability or contraction in the September quarter of last year.

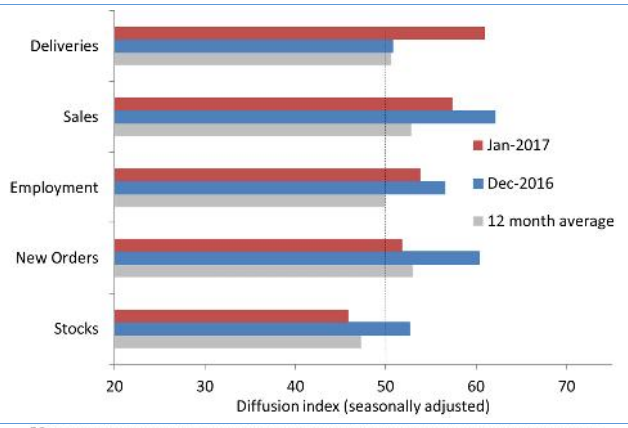

Four of the five activity sub-indexes in the Australian PSI® were above 50 points and indicated expansion in January (seasonally adjusted data). Deliveries grew strongly, lifting by 10.2 points to 61.0 points in January, the highest reading since the sub-index began. Sales continued to grow solidly in January (57.4 points), while employment continued to grow (53.8 points) although at a slower pace than in December (56.6 points). New orders remained expansionary (51.8 points) but the rate of growth slowed. Stocks fell into contractionary territory, losing 6.7 points to reach 45.9 points.

Six of the nine services sub-sectors in the Australian PSI® expanded in January (trend data). Personal and recreational services continued to grow strongly (65.0 points), while finance and insurance strengthened (62.7 points). Retail trade and wholesale trade both improved (55.6 points and 58.2 points respectively). Property and business services grew at a slightly faster pace (54.0 points), as did transport and storage (51.6 points and the first time the sub-sector has grown since September 2011). Health and community services was stable in January (50.8 points). Communication services contracted for a fourth month (47.4 points), while the hospitality sub-sector (accommodation, cafes and restaurants) shrank for a thirteenth month (43.9 points).

A number of regional respondents to the Australian PSI® noted that a good agricultural season (crops and prices) are having a positive impact on some services sectors. Positive factors for others include better customer confidence and demand and the relatively low Australian dollar in January. Problems included the cost of utilities, lack of disposable income, auto industry closures and lower demand from mining businesses.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.