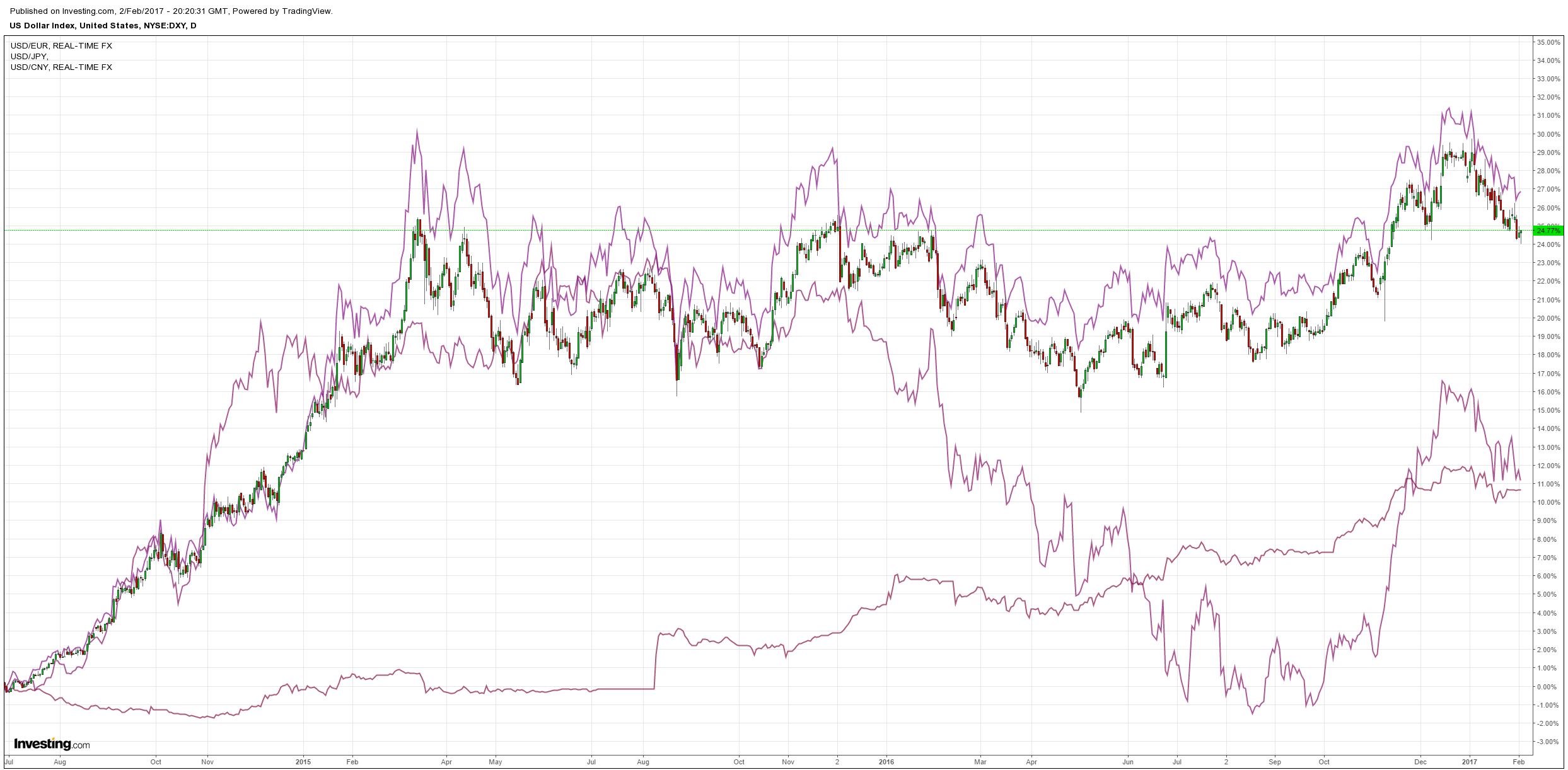

Last night the USD fell and other majors lifted:

Commodity currencies lifted, the Aussie roared:

Gold bounced again:

Oil still wants to go higher:

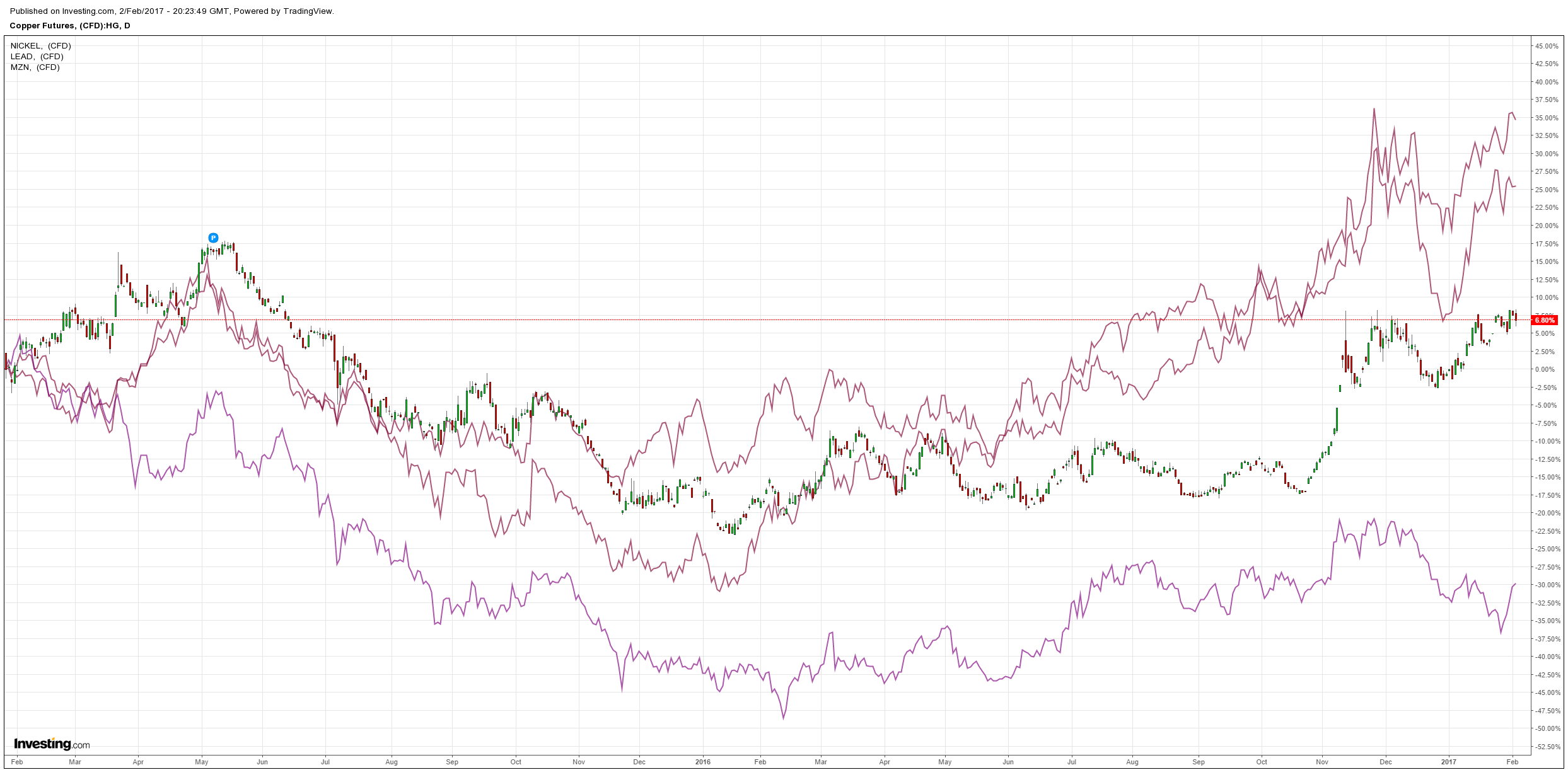

Base metals are in lock step:

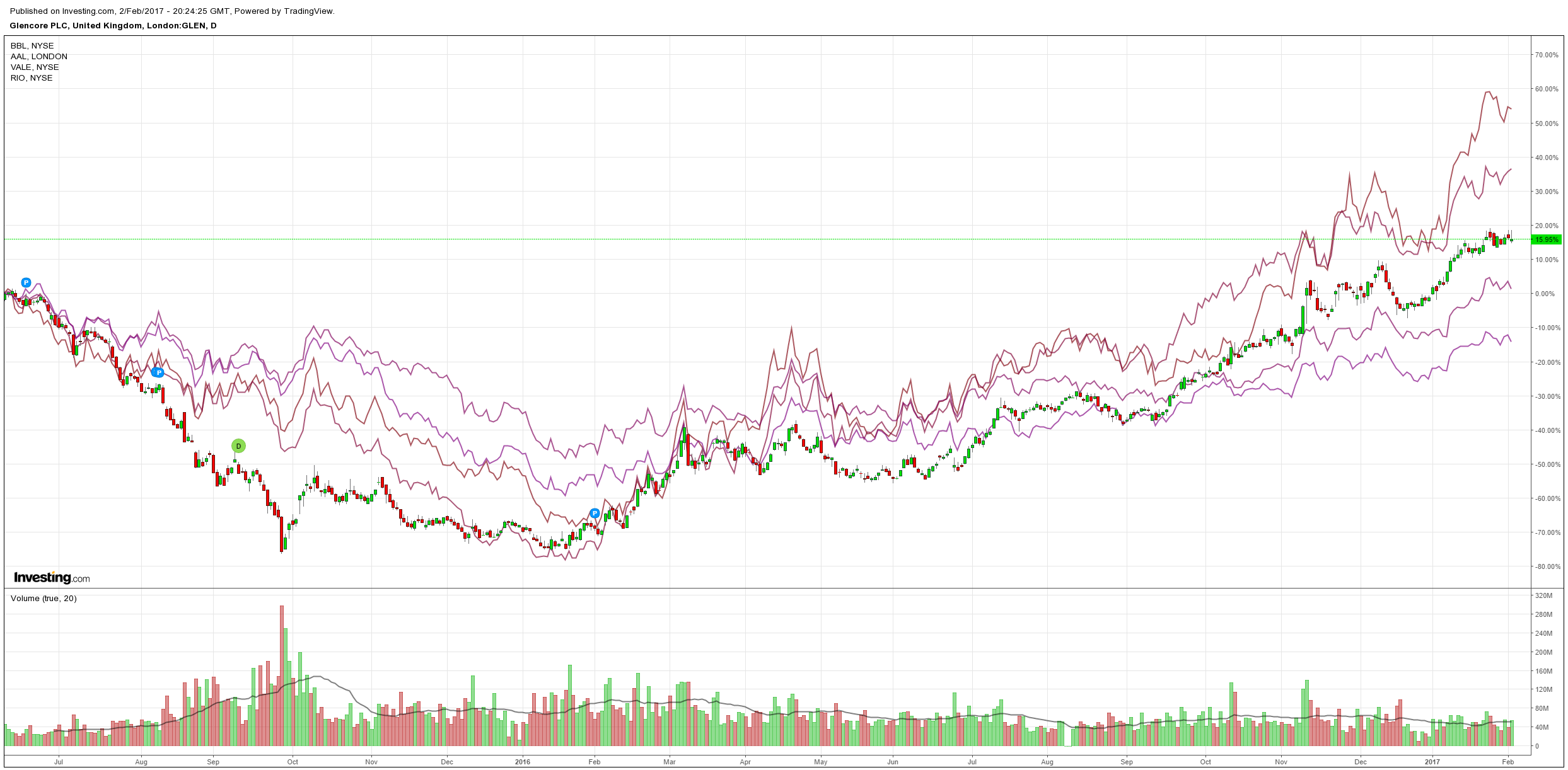

Miners fell:

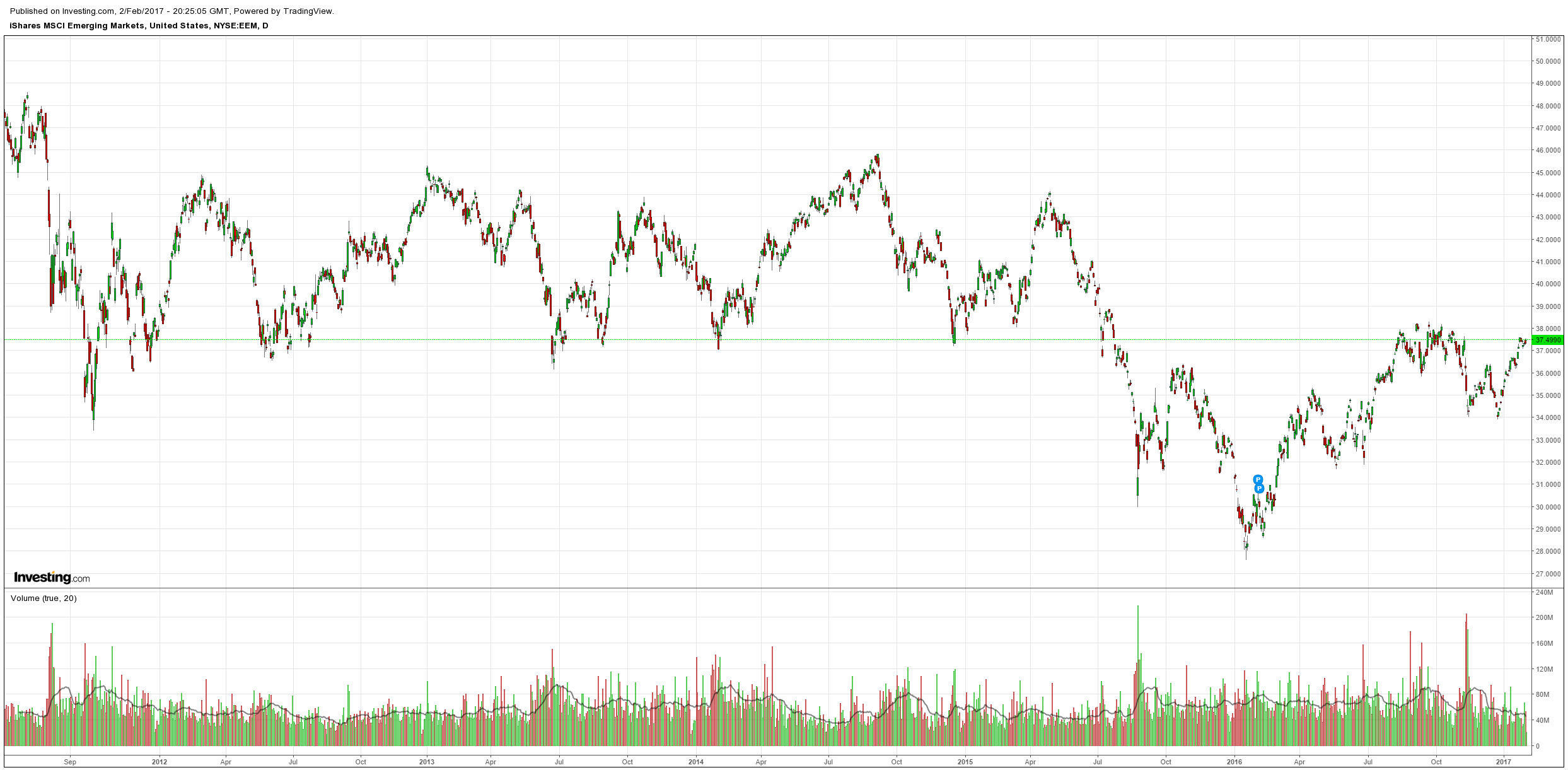

EM stocks fell:

EM and US high yield was bid:

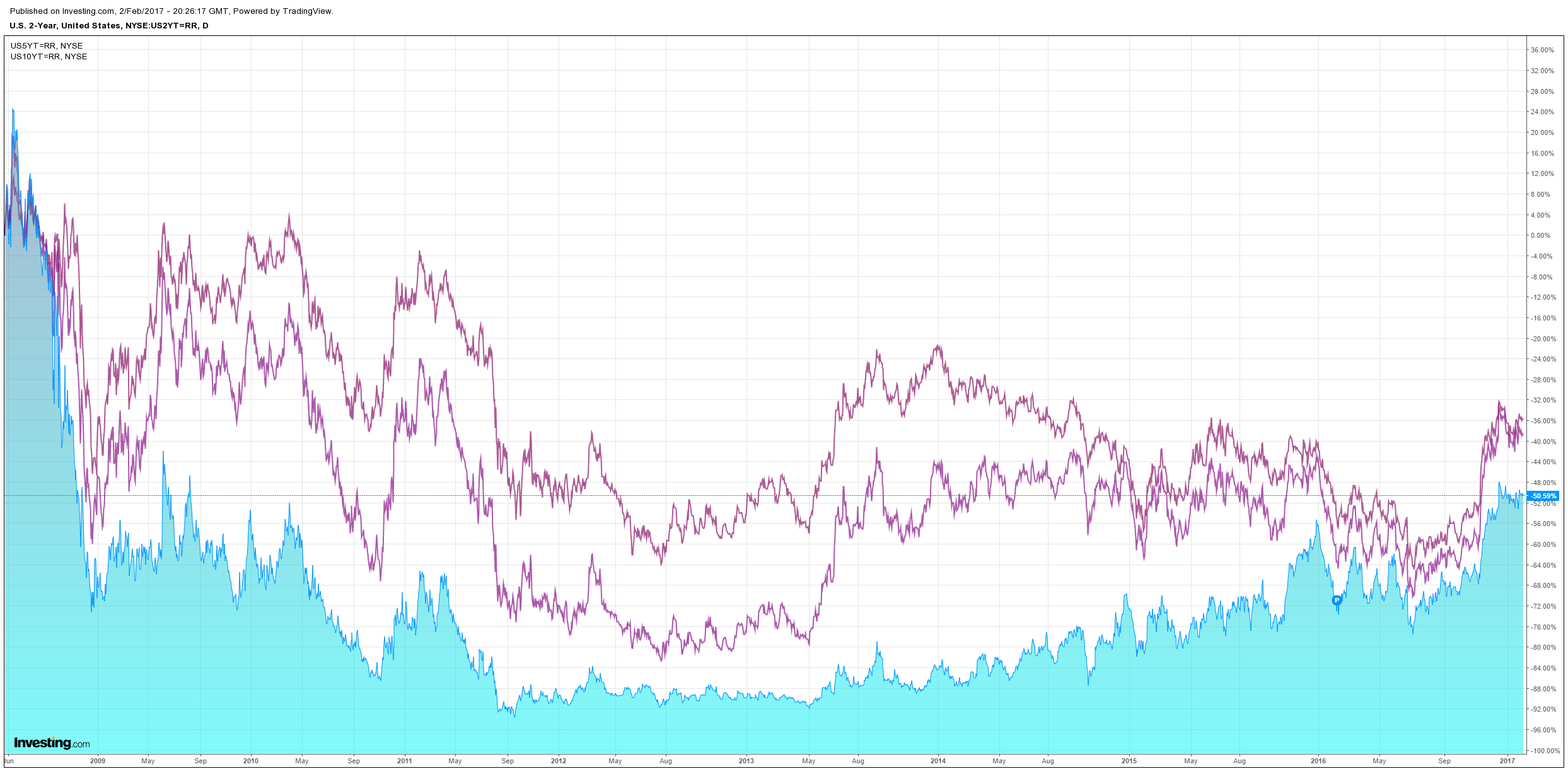

Treasuries fell a little:

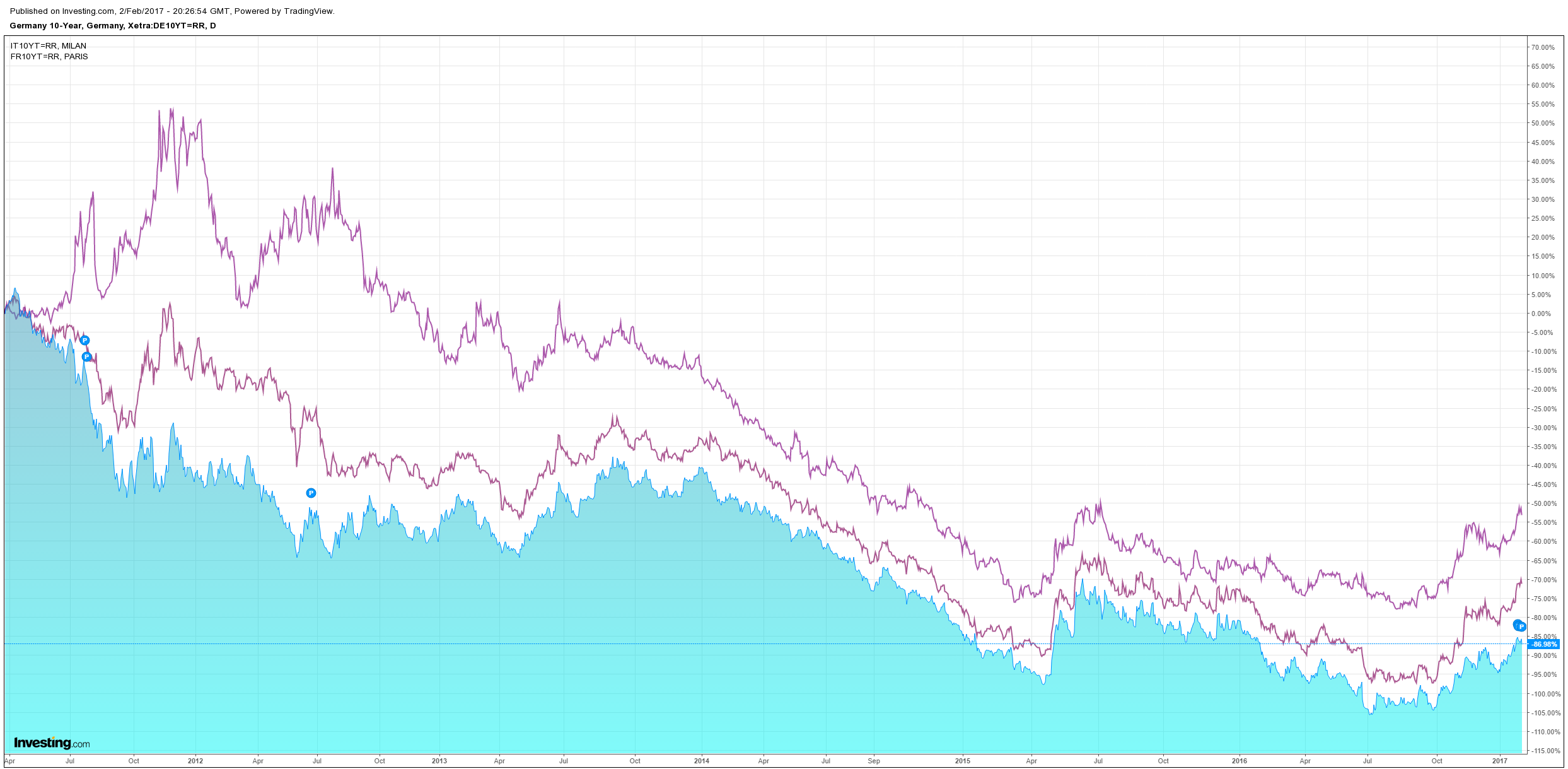

European spreads tightened:

And stocks just won’t sell off:

Tonight is US jobs and the harbingers are good, via Calculated Risk:

On Friday at 8:30 AM ET, the BLS will release the employment report for January. The consensus, according to Bloomberg, is for an increase of 175,000 non-farm payroll jobs in January (with a range of estimates between 155,000 to 195,000), and for the unemployment rate to be unchanged at 4.7%.

The BLS reported 156,000 jobs added in December.

Important note: Friday morning the BLS will also release the annual revision to “reflect the annual benchmark adjustment for March 2016 and updated seasonal adjustment factors.” The preliminary estimate of the benchmark revision was for a decrease of 150,000 jobs as of March 2016.

Here is a summary of recent data:

• The ADP employment report showed an increase of 246,000 private sector payroll jobs in January. This was above expectations of 168,000 private sector payroll jobs added. The ADP report hasn’t been very useful in predicting the BLS report for any one month, but in general,this suggests employment growth above expectations.

• The ISM manufacturing employment index increased in January to 56.1%. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll increased 14,000 in January. The ADP report indicated 15,000 manufacturing jobs added in January.

The ISM non-manufacturing employment index for January has not been released yet.

• Initial weekly unemployment claims averaged 248,000 in January, down from 257,000 in December. For the BLS reference week (includes the 12th of the month), initial claims were at 237,000, down from 275,000 during the reference week in December.

The increase during the reference suggests more layoffs during that week in December as compared to November. This suggests an above consensus employment report.

• The final December University of Michigan consumer sentiment index increased to 98.5 from the December reading of 98.2. Sentiment is frequently coincident with changes in the labor market, but there are other factors too like gasoline prices and politics.

• Conclusion: Unfortunately none of the indicators alone is very good at predicting the initial BLS employment report. However the ADP report, ISM manufacturing and weekly unemployment claims all suggest stronger job growth. So my guess is the January report will be above the consensus forecast.

And Goldman:

We forecast that nonfarm payrolls rose 200k in January, following an increase of 156k in December, with reacceleration reflecting a combination of lower-than-usual year-end layoffs, favorable weather effects, and further improvement in labor market indicators.

We believe the U3 unemployment rate is likely to fall one-tenth to 4.6% – which would mark a return to the cycle low – in part driven by reduced year-end retail layoffs. We expect average hourly earnings to rise 0.3% month over month and 2.8% year over year, reflecting firming labor markets and state-level minimum wage hikes.

The report will also be accompanied by the annual benchmark revision to the establishment survey as well as the annual introduction of new population controls in the household survey.