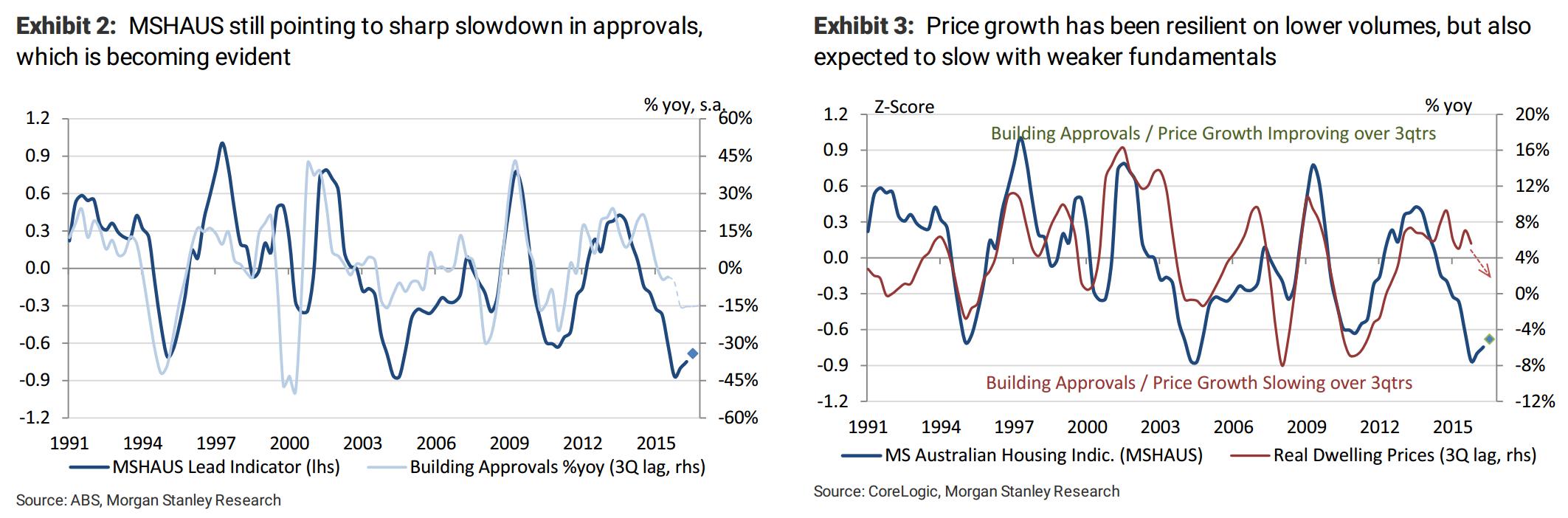

Last October we launched the proprietary Morgan Stanley Housing Australia indicator, which is calibrated to lead the building approvals and dwelling price growth cycle by 3-4 quarters (see Australia Macro+: Australian Housing: Stressing the Foundations, 19 Oct 2016). While the initial MSHAUS reading of -0.8 was near the lows seen over the 25-year history of the series, incoming data updated last week has provided only marginal support.

Factoring in just-released 3Q16 completions,as well as broader housing dynamics, we find the latest reading stands at -0.7 (time series available on Bloomberg under MSAHAUS Index). The subcomponents of our MSHAUS framework paint a weaker picture of the housing market’s ‘fundamentals’ (supply/demand, rental conditions and accessibility),albeit with some offset from looser credit conditions and stronger sentiment (especially among investors).

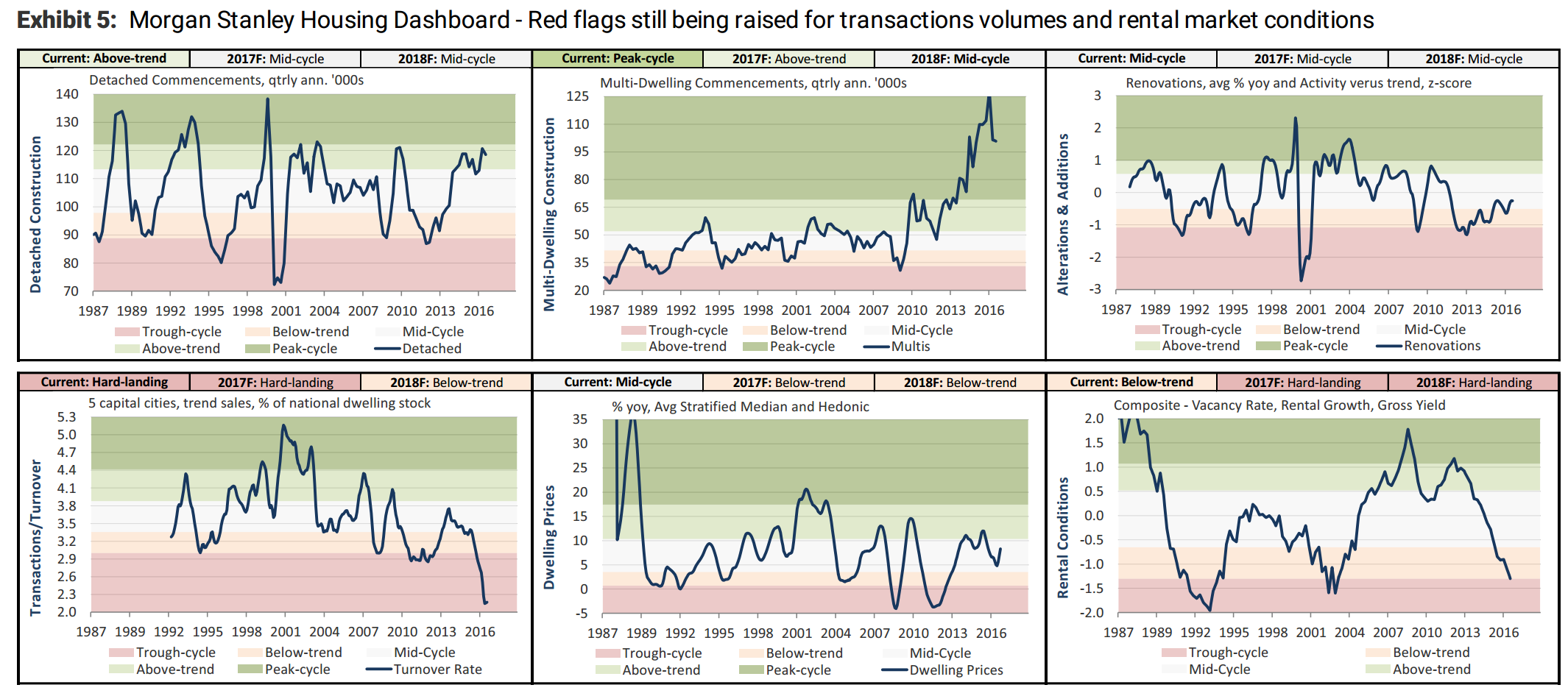

Red Flag for Transactions Activity: In conjunction with our MSHAUS indicator, our Housing Dashboard provides a snapshot of the six cycles of housing. Activity indicators softened in 3Q16, with commencements falling across both detached and multi-dwelling segments, while renovations spending (12% of resi construction) was more or less unchanged.

Red flags continue to be raised by the transactions cycle, where just 2.2% of the estimated dwelling stock turned over in 3Q16, while timely data of new and total property listings to 29 January 2017 were down -11% and -15% over the year in Sydney and Melbourne, respectively.

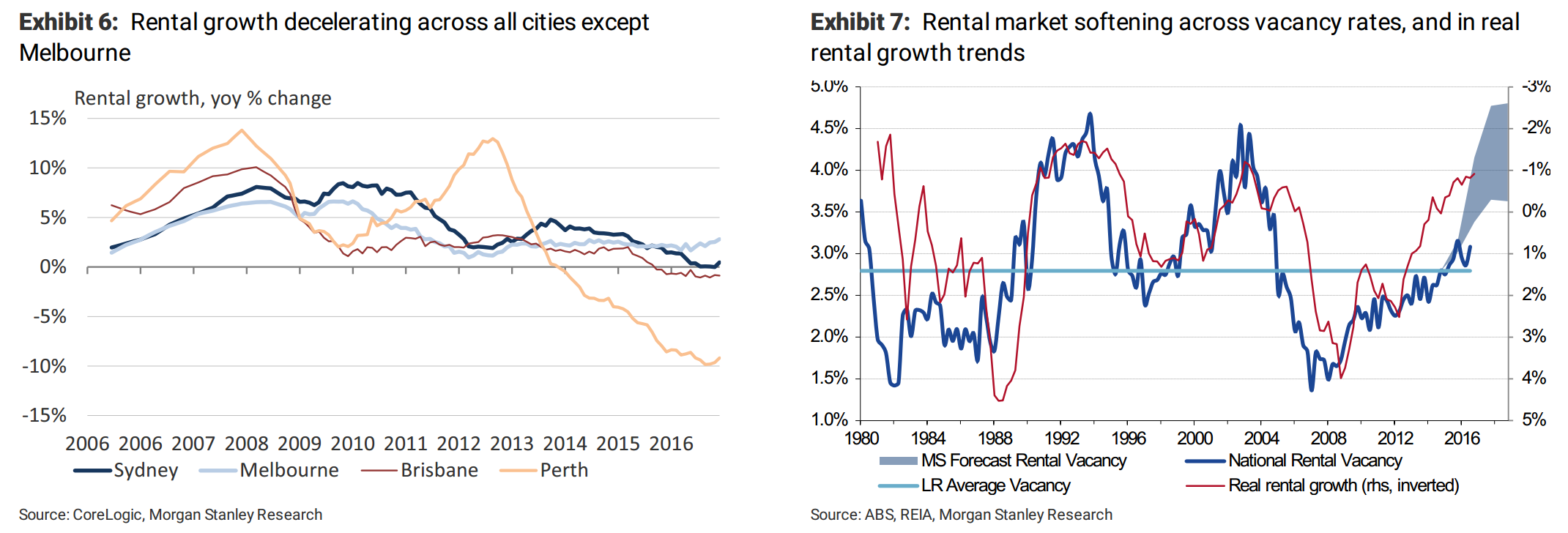

Rental market conditions are also softening quickly, with headline rent inflation of 0.6% yoy equating to a -0.9% yoy fall in real rents over the year to 4Q16. As of 3Q16, rental vacancies stood at 3.1%,and rental yields of 3.2% are at the lows of their 11-year history.

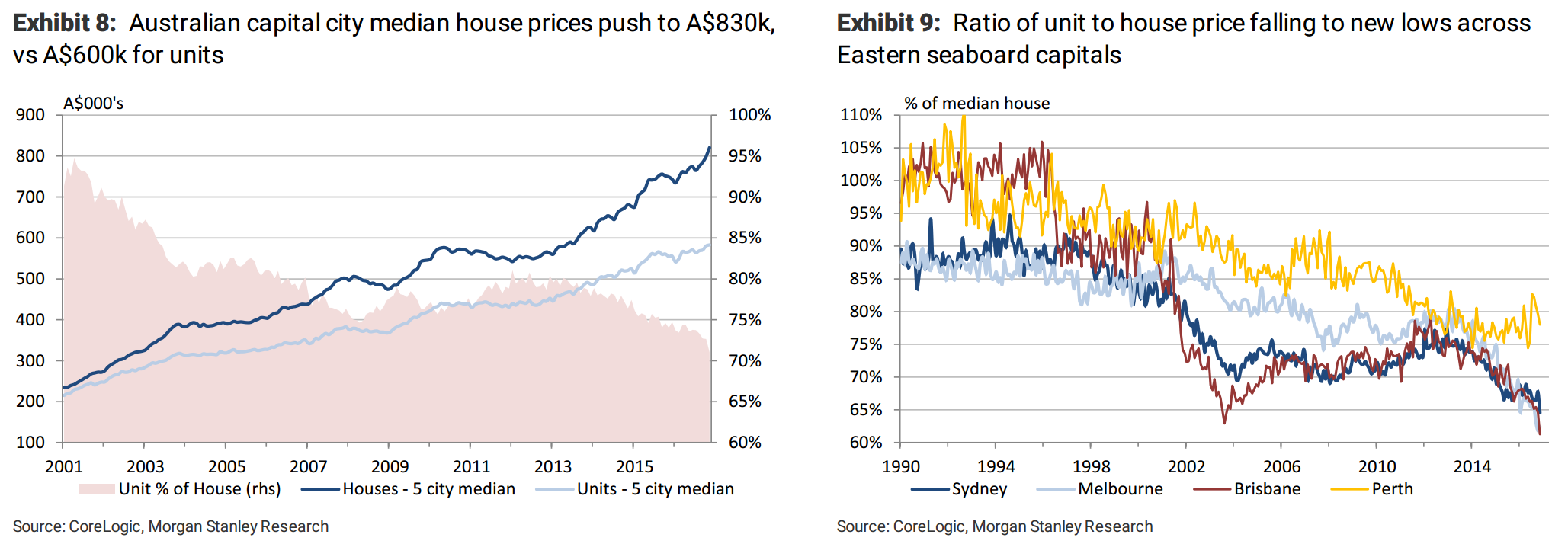

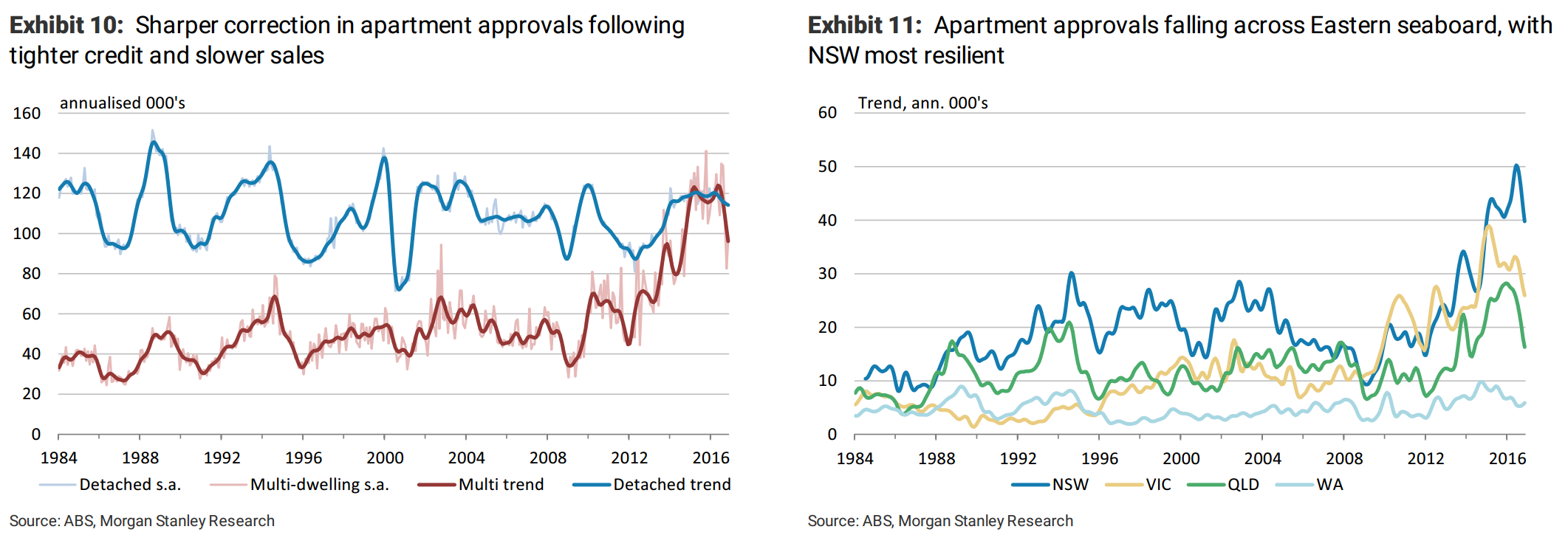

Apartments diverging from detached: Drilling down, we note weaker trends for the apartment cycle versus detached housing – consistent with our view of a hard landing in the former. Capital city price growth over 2016 came in at an aggregate 10.8%, with units up 5.9%,effectively half the 11.6% in capital gains for houses. We believe this reflects the relative supply of apartments, which will increase further over 2017-18,versus the support for underlying land values from urban densification. This divergence saw the ratio of median unit prices hit a new record low versus houses in 2016,at 65% in Sydney, 62% in Melbourne and 61% in Brisbane.

Likewise on the construction side, we have seen a sharper slowdown in building approvals for new units, which in trend terms are down 22% from their May 2016 peak, where detached approvals have edged down 5% from their March highs. This is consistent with our thesis that the development cycle is slowing quickly on tighter credit availability for developers and investors.

Supervisors Stepping Up Again? Over the past week, we have seen CBA,and its subsidiary, BankWest, take steps to slow the growth in investor property loans (IPLs), suspending the refinancing of mortgages for those switching banks and further repricing its interest-only IPLs by another 12bp. These steps may be related to the group’s 10.2% annualised run-rate in December, which exceeds APRA’s 10% speed limit.

In addition, BankWest has announced that it would tighten IPL serviceability criteria by excluding negative gearing tax benefits. We were under the impression that these were already wound back, after APRA Chairman Wayne Byres called out the practice in a speech on 13 May 2015. Still, we see this step by BankWest as ‘better-late-than-never’ and will monitor whether others follow suit – given it should reduce the gearing capacity of investors most stretched on a disposable income basis,and thus be well targeted to both restraining the market and improving its financial resilience.

RBA anticipating leverage to global recovery: The RBA’s quarterly SoMP confirmed a more upbeat outlook for global growth,noting that “the global economy entered 2017 with more momentum than earlier expected”and “growth in the major advanced economies is expected to be above potential”. In addition, Australia’s terms of trade have risen by more than 15% since mid-2016,helped by stronger Chinese demand and supply disruptions. These two changes saw the Bank hold its Australian growth forecasts unchanged through 4Q17 and 2018, despite modestly downgrading its outlook for consumption.

Deleveraging resources/fiscal sector and slowing housing activity to delay pass through: In contrast, we see these macro tailwinds providing less benefit than historically, especially through CY2017. Our view is that the resources sector will use the FCF windfall to pay down debt, and pay out dividends, while the Federal government sequesters any boost to revenues in the hope of retaining its universal AAA sovereign rating. This outlook would leave consumption exposed to weak income growth and the housing-related headwinds discussed above.

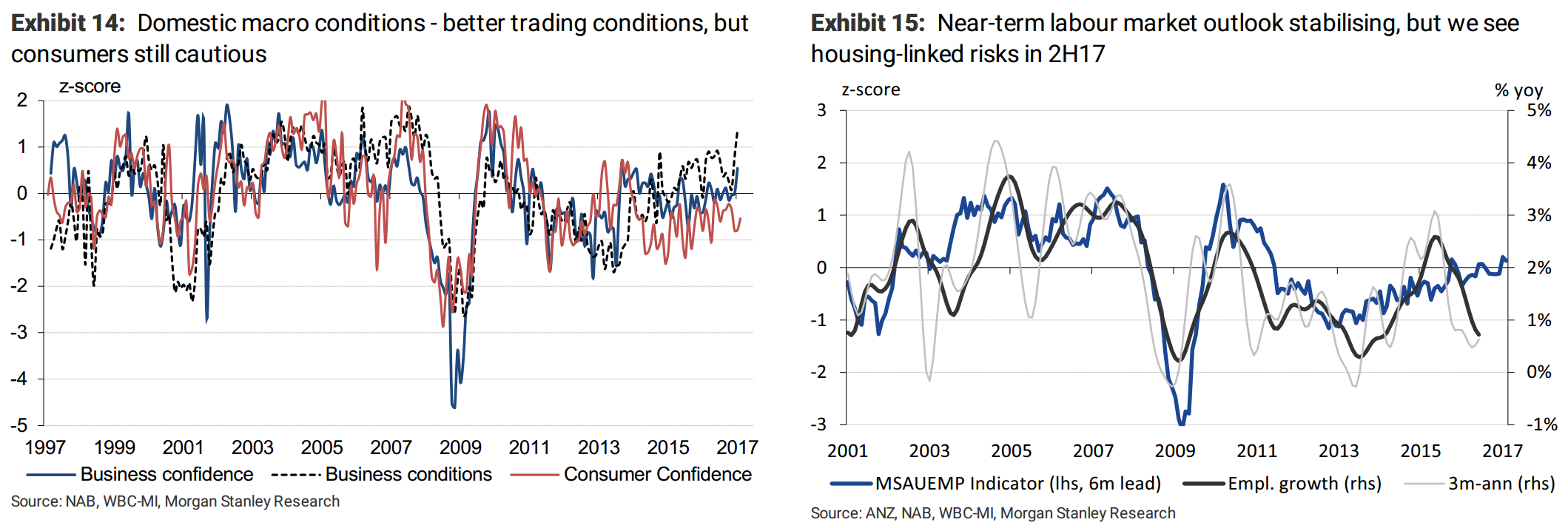

That said, in the near-term we will continue to monitor domestic macro conditions, including through consumer and business sentiment data. This week saw a notable improvement in business conditions,although we will look to see whether this is sustained, particularly as it was not mirrored on the consumer side.Likewise, our MSAUEMP edged up on stronger hiring intentions, but remains well below mid-cycle conditions. All up, we see little near-term pressure for the RBA to cut rates (our forecast is for a final cut in 3Q17), but we are even less convinced that a tightening cycle is either warranted or imminent.

While the tone of the SoMP appeared more balanced than Tuesday’s Governor’s statement, we view the RBA’s outlook as highly reliant on the external environment. We think risks are skewed towards a near-term retracement in the AUD,and continue to suggest being long front-end/belly AUD rates as well as curve steepeners.

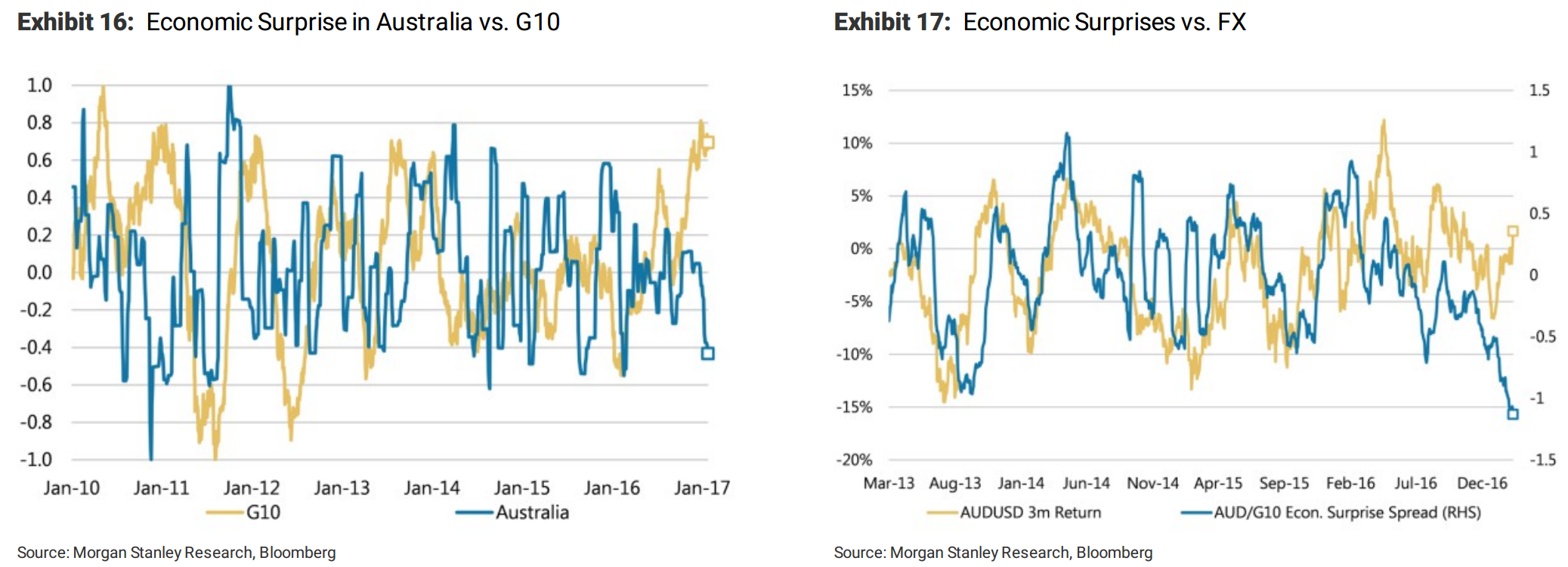

Against the backdrop of domestic data failing to participate in the broad improvement in DM data (see Exhibit 16),and the weak outlook for housing, the improvement in commodity prices and terms of trade appears to have outweighed domestic dynamics for the AUD. Despite domestic data not keepingup with developments in G10, AUDUSD has trended slowly but firmly higher since the start of the year (see Exhibit 17). A possible interpretation of this would be that the market is expecting Australia to benefit relatively more from an improved global environment.

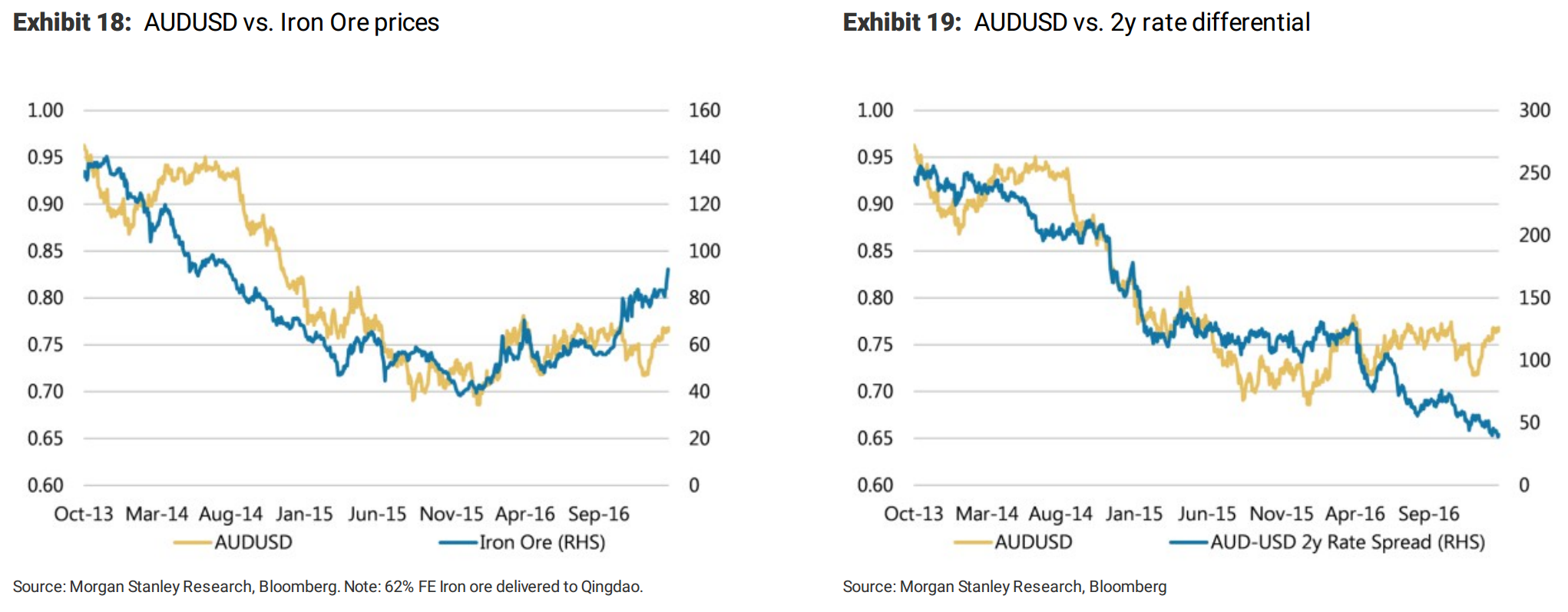

More specifically, we believe the continued rally in bulk commodities has putupward pressure on the AUD over the past few months. While the increase in,e.g. iron ore prices, would have implied a sharper AUD rally (see Exhibit 18), rate differentials are pullingFX the other way (see Exhibit 19). Rate differentials vs. the US should continue to converge, given our expectations of a further RBA cut in 2H17, while the Fed delivers two hikes in 2017, on our forecasts and as implied by the market.

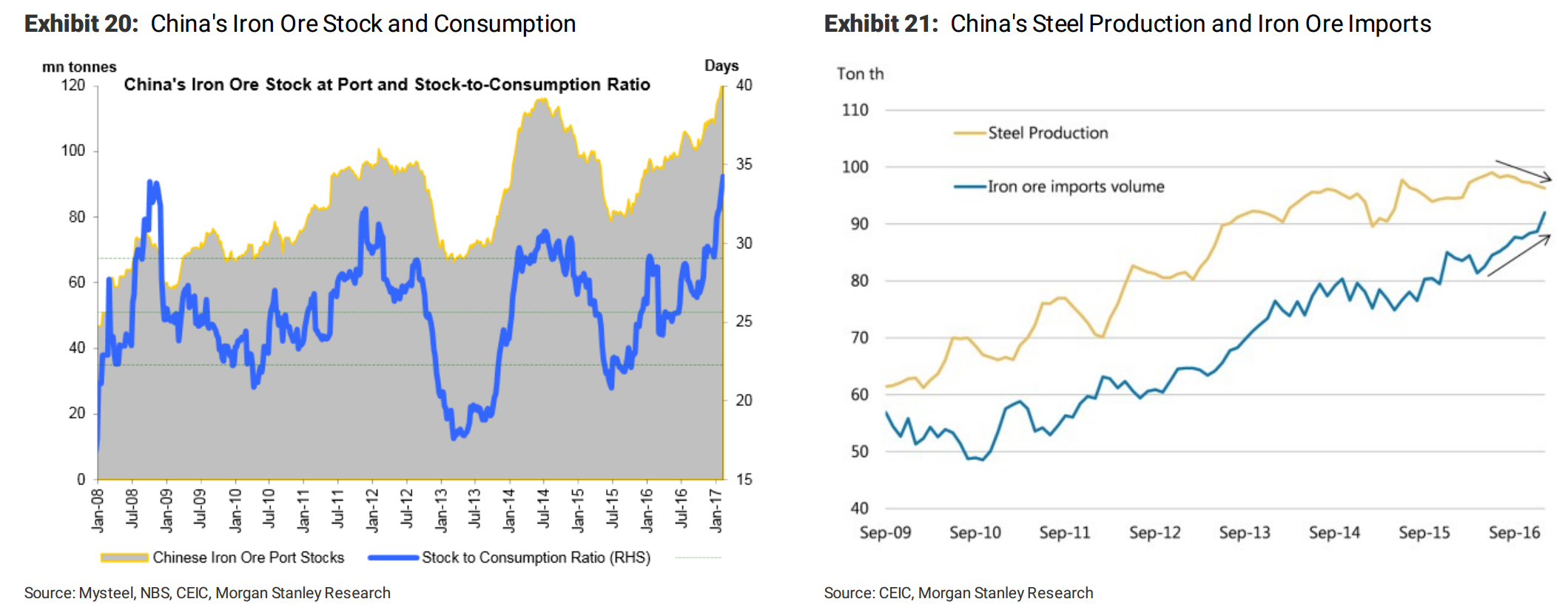

Meanwhile, Chinese iron ore inventories appear stretched relative to consumption (see Exhibit 20), with the stock-to-consumption ratio near multi-year highs. We also note that Chinese iron ore imports have outpaced e.g. steel production (see Exhibit 21), both pointing towards price action that is at least in part driven by higher Chinese inventory rather than activity. Should price action in iron ore soften from here, we think AUD could weaken quickly.For example,using the historical relationship between AUDUSD, iron ore and 2y rates differentials since 2013as a guide,a decline back to $60/tonne for iron ore should see AUD soften to around 0.70.

Risks to the trade would come from continued cyclical strength in China and G10, keeping commodity prices and exports from Australia supported.

On the rates side, we continue to suggest receiving the AUD front-end, receiving the belly against USD,and like steepeners as a hedge against a continued improvement in global conditions.For a more detailed outline of our Australian rates views, please see Aussie Downside Surprises and Reconciling with Reflation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.