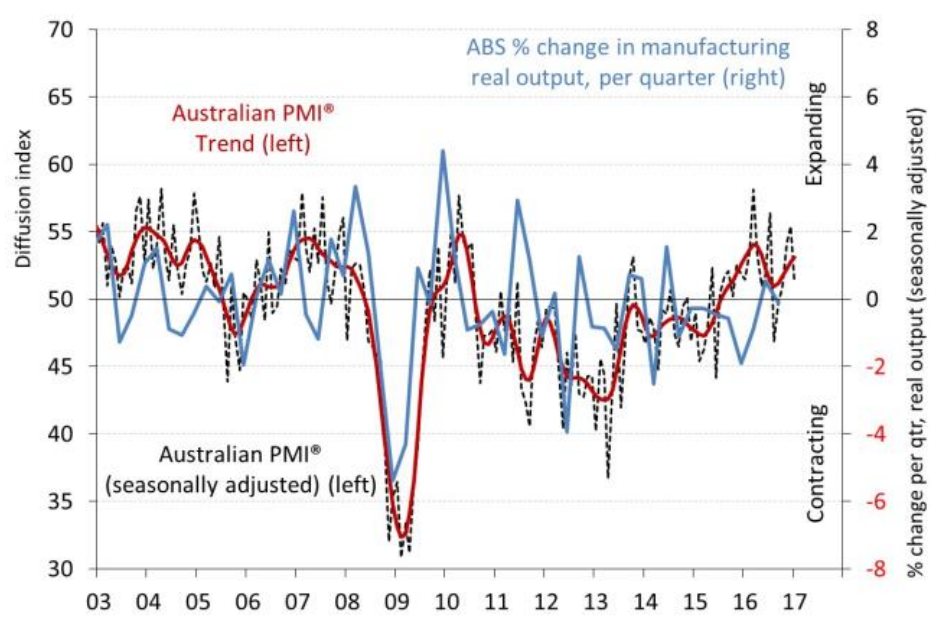

The Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI® ) has expanded for a fourth consecutive month, with a reading of 51.2 points in January, albeit down by 4.2 points since December (results above 50 indicate expansion and the distance from 50 points indicates the strength of expansion). This adds to the solid growth seen at the end of 2016.

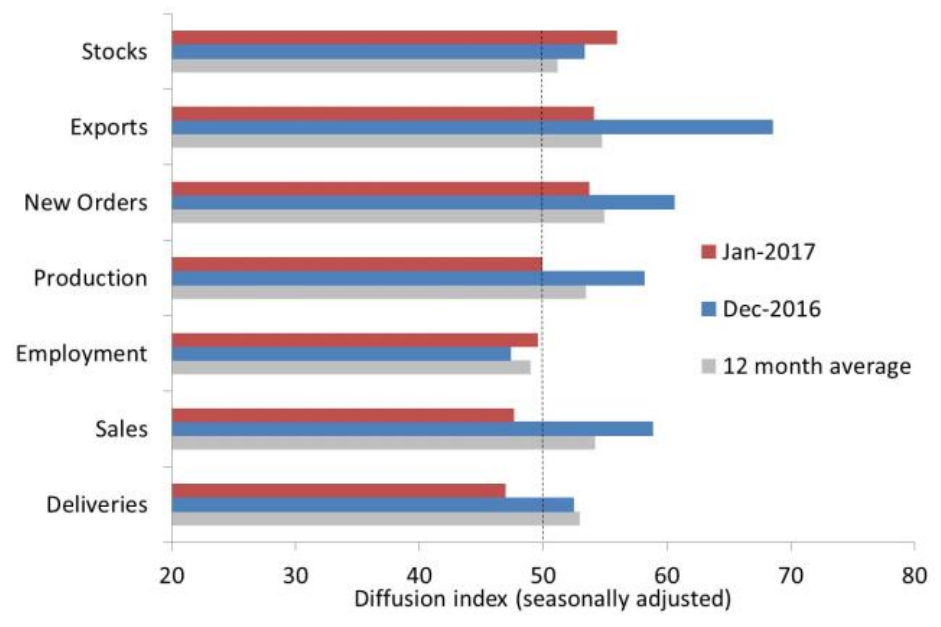

Three of the seven seasonally-adjusted manufacturing sub-indexes expanded in January with two sub-indexes stable and two contracting. In a positive indicator for near term growth, new orders continued to expand (53.7 points). Exports expanded (54.1 points) and stock levels (56.0 points) built up over the month. Production (49.9 points) and employment (49.6 points) were stable while deliveries (47.0 points) and sales (47.6 points) contracted.

In trend terms, four of the eight sub-sectors in the Australian PMI® expanded in January, two were stable and two contracted. Food & beverages (53.9 points) and petroleum & chemical products (53.5 points) continue to grow albeit at a slower pace. Non-metallic mineral products (65.9 points) and machinery & equipment (57.5 points) expanded at a quicker pace, while wood & paper products (50.5 points) and metals products (49.9 points) improved to more stable conditions. Textiles & clothing moved closer to stable conditions (47.9 points) while printing & recorded media sank further into contraction (35.5 points).

Comments from manufacturers in January show new orders are picking up across many sub-sectors at the start of the year. While demand appears to be patchy, some construction projects are helping activity and pockets of growth in agriculture and mining (due to some recovery in commodity prices) are lifting activity for manufacturers. As with much of 2016, exports continue to spur growth mainly due to the continued lower Australian dollar. Recently, inventories look to have built up for most manufacturers and this may impact production in coming months. Energy costs and reliability remain prominent issues for manufacturers with higher prices in particular impacting the profitability of many manufacturers.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.