by Chris Becker

A more positive session in Asia today, helped by a slightly weaker Yen due to BOJ intervention, a lack of bad data and economic catalysts while commodity prices surged due to continued speculation in China and ructions in copper, while oil came off the boil again, just in time for the DOE inventories tonight.

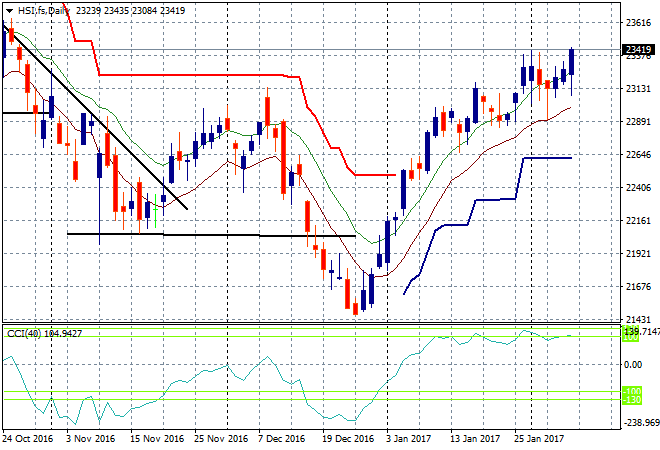

The Shanghai Composite is positive, up 0.4% to be at 3166 points still trying to build momentum and find any buyers while the Hang Seng Index was more bullish, up 0.6% and shooting out of the gates on the daily chart:

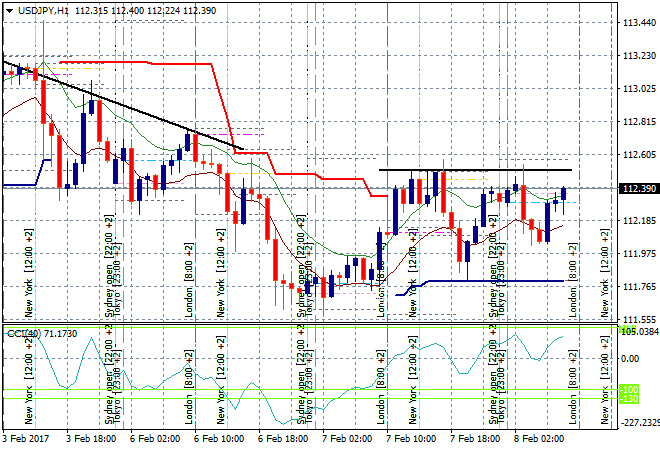

Japanese stocks were positive for once with the Nikkei up 0.5% to be above 19000 points again as the Yen weakened slightly against the USD and other currencies. The hourly chart for USDJPY shows an possible consolidation zone between 111.75 and 112.50 that could swing to the upside as the BOJ again steps in and provides liquidity:

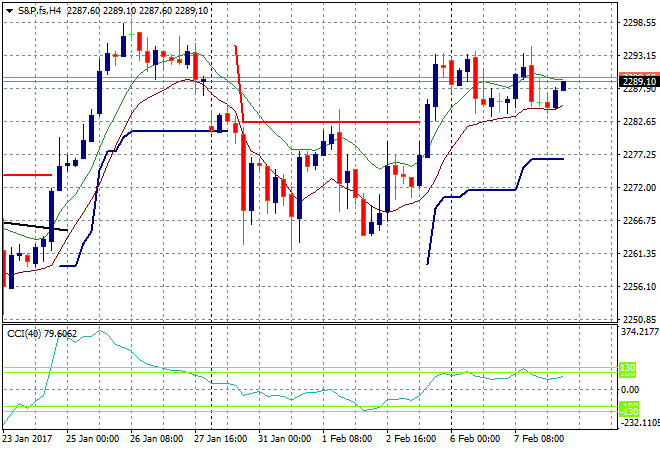

S&P Futures are again flat, with the mid point of control unchanged at 2285 points or so, although there is a slow uptick to the lows here that might suggest a more positive night tonight. There’s still nothing to get excited about with US stocks here until the previous week’s high at 2298 is breached:

The ASX200 had a surprisingly good day buoyed by commodity prices, closing up 0.5% to 5651 points, although it was financials that really led the way with BHP off slightly due to possible striking action at one of its copper mines and the lower oil price.

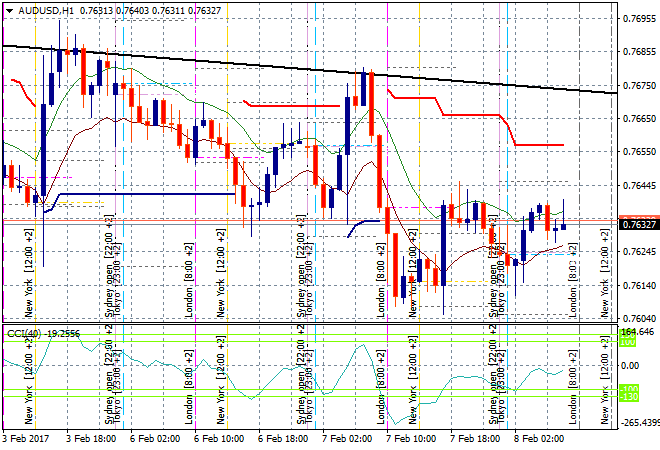

The Aussie dollar is trying hard to get back to last night’s sessions highs but is struggling with strong resistance at the 76.40 zone against USD. The hourly chart below shows further resistance overhead so we could be seeing some bullish bets unwinding:

The data calendar is again very quiet tonight, although we do get DOE oil inventory and first up in the morning its the RBNZ’s turn at deciding its interest rates/property bubble quandary.