An interesting skirmish has erupted between Assistant Minister to the Treasurer, Liberal MP Michael Sukkar, and his Labor counterpart, Andrew Leigh, over the impact of Australia’s dividend imputation system on company tax cuts.

The fight began when Sukkar accused Leigh of misunderstanding the dividend imputation via the below media release:

Confused Leigh’s own words come back to bite him

Andrew Leigh is repeating his misrepresentation of Australia’s corporate tax rate to defend his backflip on now opposing a cut to the corporate tax rate he once supported.

Yesterday and again today, the Shadow Assistant Treasurer tried to incorrectly claim that we don’t need to reduce the 30% corporate tax rate because somehow the corporate tax rate is actually akin to a 20% rate:

“What Australians have to recognise is that our corporate rate has dividend imputation. That means we take a third of the company tax revenue and we give it back. So a corporate tax rate of 30 per cent with imputation raises as much as a rate of 20 per cent without imputation.”

Leading tax professionals throughout Australia have expressed alarm at this misrepresentation, or even worse, concern that the Shadow Assistant Treasurer is genuinely confused about such a fundamental part of Australia’s tax system.

Firstly, we do have a dividend imputation system in Australia that was introduced by Labor in the 1980s to avoid double taxation. Double taxation occurs when the company pays 30% on profits and the shareholder pays tax again at their full marginal rate on the dividend.

Secondly, the corporate tax rate is currently 30%.

Yet again, Andrew Leigh’s own words come back to haunt him, when he wrote in 2010:

“One key feature is the extent to which there is an imputation system, under which part of any corporation tax paid is treated as a pre-payment of personal income tax.”

Dividend imputation does not reduce the corporate tax rate.

Dividend imputation does not reduce the tax paid by corporate entities.

Dividends are paid from after tax profits and the corporate tax rate is 30% not 20%.

Let’s take the example of a company generates $100 in profit and pays $30 in tax at the 30% rate.

This leaves the company with $70 profit after tax and if it pays $70 of that to shareholders as a dividend.

When the shareholder receives the $70 dividend they are also entitled to the $30 franking credits at the ATO. Therefore the total assessable income or grossed up dividend is $100.

The shareholders marginal tax rate will determine if they have to pay the ATO additional tax or potentially receive franking credits back as a tax refund.

But the corporate tax paid by the company in this example remains at 30%.

According to Treasury: Under imputation, company tax acts as a withholding tax on Australian shareholders by collecting some of the tax that would be paid by the shareholder when they receive a dividend. Australian shareholders then receive a credit against their tax liability for the tax paid by the company.

Further, while Australian shareholders can claim franking credits, company tax is a final tax on foreign shareholders. Foreign shareholders face the 30% tax rate, which is high by international standards.

Lowering the corporate tax rate will make more business investment opportunities viable. It is the 30% company tax rate that matters for foreign investment as they cannot use franking credits.

No amount of obfuscation or confused justifications from Andrew Leigh can cover for the fact that, he now opposes a cut to the corporate tax rate he once strongly supported and argued for.

To which Andrew Leigh hit back with the following media release:

In a confused media release today, Assistant Treasury Minister Michael Sukkar suggests that we should ignore dividend imputation when discussing Australia’s company tax rate.

Dividend imputation reduces the revenue available to government. Most of the countries that the government likes to compare Australia’s company tax rate with do not have dividend imputation.

Research by Macquarie University Professor Geoffrey Kingston estimates that dividend imputation returns about one-third of the corporate tax revenue to taxpayers.

So a corporate tax rate of 30 per cent with imputation raises as much as a rate of 20 per cent without imputation.

Worryingly, Mr Sukkar seems not to understand this basic fact.

This latest gaffe comes just weeks after Mr Sukkar refused to rule out making all mortgage interest payments tax deductible, which the Grattan Institute estimates would cost the budget $19 billion a year.

With an economic team like this, it’s little wonder that Australia’s net debt will soon be twice as large as it was when the Abbott-Turnbull Government took office in 2013.

Other than pedantry, I fail to understand the point of Sukkar’s attack. Is he seriously trying to claim that dividend imputation does not reduce the federal government’s take from company taxation? Because this was the central point initially made by Leigh.

Ultimately, there is one threshold issue that needs to be overcome in deciding whether to cut Australia’s company tax rate to 25% from 30%:

“Would cutting company taxes generate enough investment, jobs and growth to justify the estimated $8.2 billion cost to the Budget each and every year, and are there better uses of scarce taxpayer money”?

The first part of this question is easily answered by looking at the Treasury modelling of the proposed company tax cut. It showed minimal benefits to either jobs or growth, as explained by The Australia Institute’s Richard Denniss:

According to Treasury’s in-house modelling, and the modelling it commissioned from Chris Murphy, if the company tax rate is lowered from 30 per cent to 25 per cent then gross domestic product will double by September 2038, while without the tax cut it won’t double until December 2038. Wow, a whole three months earlier. Both modelling exercises conclude that in 20 years’ time the unemployment rate will be 5 per cent regardless of whether we spend $50 billion on company tax cuts or not…

The “benefits” are more accurately described as rounding error than significant reform.

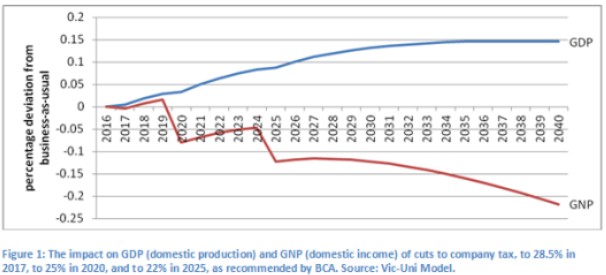

You could also consider the modelling from Victoria University senior research fellow, Janine Dixon, which showed that Australian national income would likely be reduced from cutting company taxes:

Regarding the second part of the question, there are plenty of better policy alternatives, including using some or all of the funds that would be spent on cutting company taxes to:

- undertaking critical infrastructure investment and restoring Australia’s dilapidated infrastructure stock;

- using direct measures to spur business investment, such as accelerated depreciation allowances, investment allowances, or some other measures; or

- boosting spending on education.

Any of these measures are likely to generate far bigger pay-offs to the resident population than the Coalition’s clumsy plan to slash the company tax rate, which would merely gift billions of dollars to foreign owners/shareholders in the blind hope that they may increase investment.

unconventionaleconomist@hotmail.com