The Australia Institute (TAI) has released another report, entitled Oligopoly money How a company tax cut would be wasted on big business, which argues that the Turnbull Government’s planned company tax cut would be unlikely to encourage the largest companies in Australia to increase investment.

Below is the report’s summary:

The Abbott-Turnbull Government’s enterprise tax plan will, if implemented, grant a company tax cut worth $50 billion over 10 years. Supporters claim the tax cut would increase long run investment, innovation and employment. Such claims require close scrutiny especially when the costs of the tax cuts are upfront and the public benefits are 20 years or more in the future.

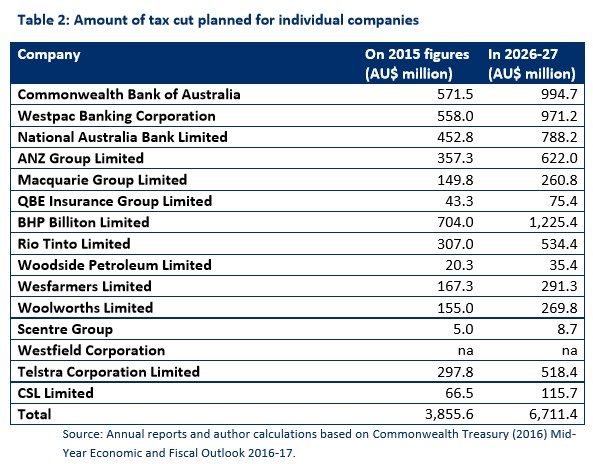

Together the biggest beneficiaries of the tax cut are the largest 15 listed companies in Australia:

Commonwealth Bank

Westpac

National Australia Bank

ANZ

Macquarie

QBE Insurance

BHP Billiton

Rio Tinto

Woodside Petroleum

Wesfarmers

Woolworths

Scentre Group

Westfield

Telstra

CSL

Collectively these companies stand to gain a third of the tax cut, worth $6.7 billion per year, once it is fully implemented.

Yet little of this gain is likely to be put into productive, innovative, job-creating employment:

The large banks and insurers made nine per cent of taxable company income in 2015, yet made just 1.2 per cent of private investment in Australia.

Mining investment is dependent on where minerals are and their price rather than changes to company tax.

Investment by the dominant retailers focuses on gaining advantage over each other, rather than innovation, for example through strategic property purchases.

Telstra makes little net investment. In the last two years its investment in property, plant and equipment was $5,896 million while its depreciation on property, plant and equipment was almost the same at $5,872 million. If Telstra was a serious investor in innovation, there would be no need for NBN Co.

The reason these firms make few investments that increase innovation, employment or productivity is that they do not operate in truly competitive markets. Many of Australia’s key markets are dominated by a small number of companies – ‘oligopolies’ in economics jargon. Oligopolies are unlikely to change their investment or employment decisions based on a cut in company tax rates.

Economists refer to oligopolies as being ‘lazy’ – more interested in maintaining their market power than trying to innovate. Investments they do make focus on strategic behaviour and are designed to maintain their market position.

Oligopolies that do undertake innovation usually do so to lower their own costs, in particular by reducing labour costs. Examples of this include ATMs, internet banking and self-serve checkouts. This is unlikely to be the types of innovation that the proponents of the company tax cuts are talking about when they say it will encourage additional employment.

If the aim of the company tax cut is to increase investment and employment much of it will be wasted if it is given to large oligopolies. If the government wants to encourage investment and employment it should focus on reducing the market power of these oligopolies rather than handing them billions in company tax cuts.

Another way to promote business investment at much lower cost is to junk the company tax cuts and instead offer direct incentives like accelerated depreciation allowances, investment allowances, or some other measures (see yesterday’s post).

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.