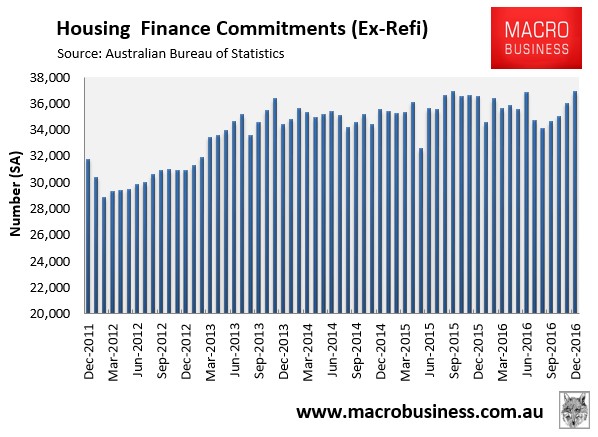

Today’s housing finance data for December, released by the Australian Bureau of Statistics (ABS), posted another monthly increase in finance commitments, with annual mortgage growth also rising.

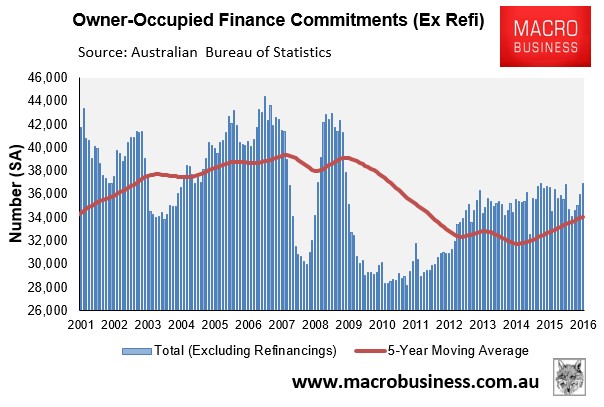

According to the ABS, the total number of owner-occupier finance commitments (excluding refinancings) jumped by a seasonally adjusted 2.4% over the month to be up 0.9% over the year:

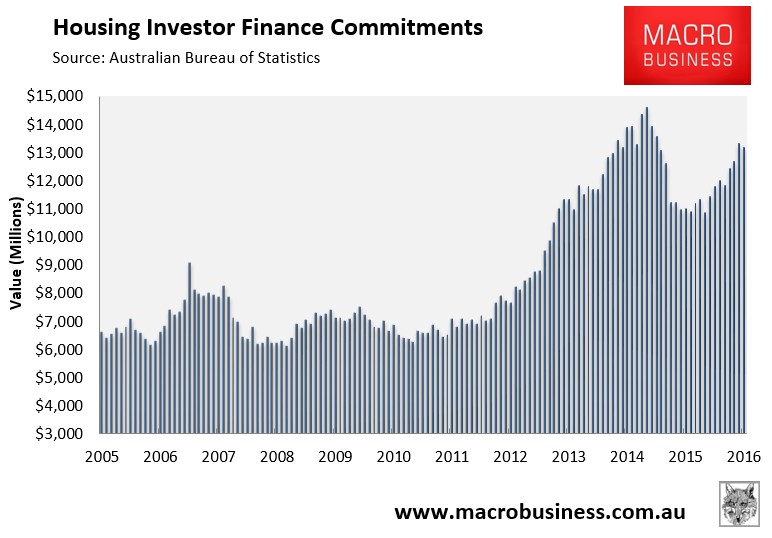

However, the value of investor finance commitments retraced 1.0% in December but was up by 19.9% over the year (see next chart).

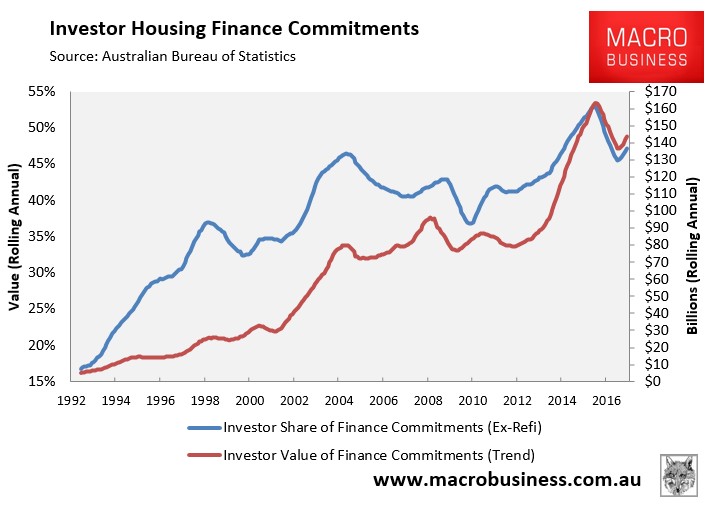

The annual share of total loans going to investors (excluding refinancings) rose by 0.3% to 47.1% in December, but was still down significantly from the peak of 52.9% recorded in July 2015:

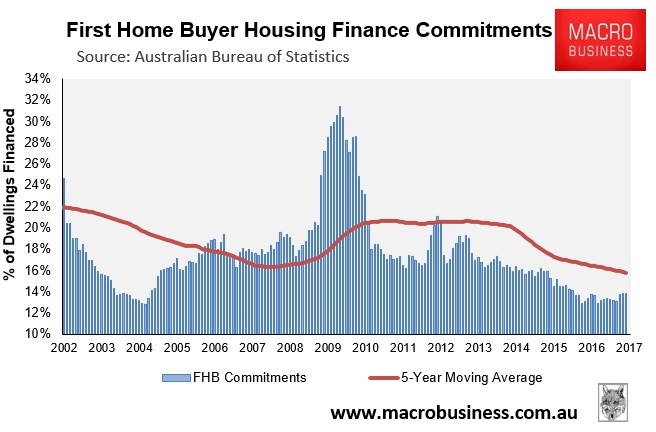

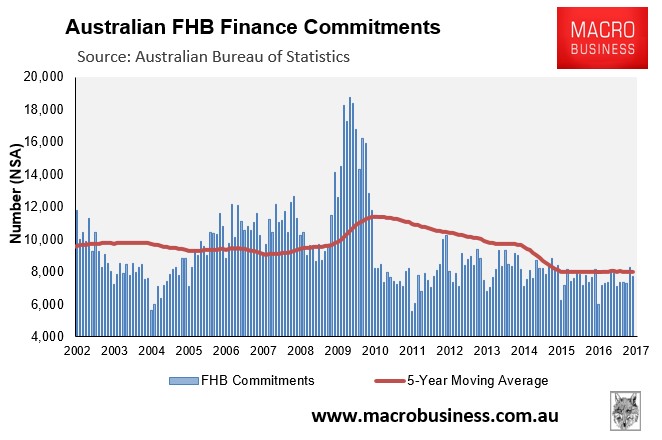

First home buyer (FHB) owner-occupied demand slumped in December. It tanked by 7.1% over the month to be down 5.6% year-on-year, and represented just 13.8% share of total owner-occupied finance commitments (see below charts).

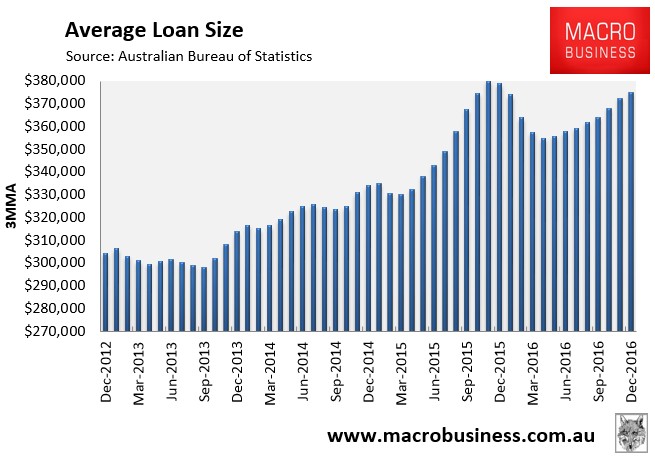

Meanwhile, the average loan size fell slightly in December, down 0.2% over the month, but was still up by 0.5% over the year. The trend also continues to recover following the sharp falls at the start of last year:

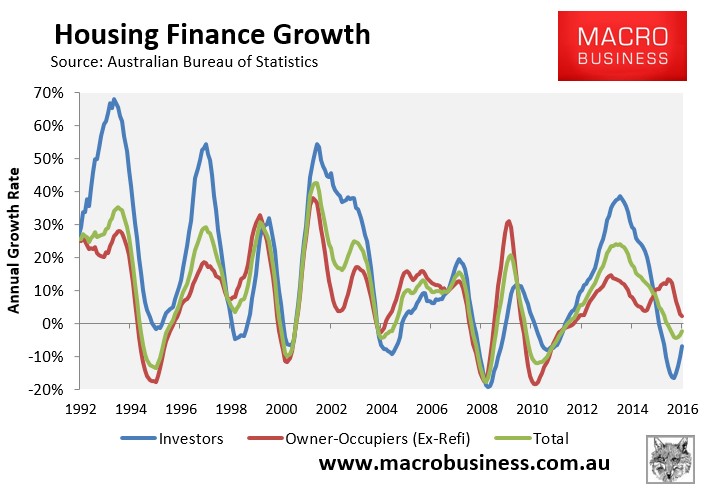

Finally, the below chart shows that falling annual growth in owner-occupied housing demand is now being more than offset by rebounding investor demand, causing overall growth of housing finance (excluding refinancings) to rise:

Back in December 2016, David Murray – the former CEO of the Commonwealth Bank and head of the Financial System Review – appeared on Switzer TV and likened the Australian housing market to the 1600’s Dutch Tulip Bubble. Murray also warned that “something needs to be done about it in a regulatory sense and the RBA and APRA need to stay on it”.

Is APRA listening? Why won’t it immediately lower its investor loan speed limit to 5%?

unconventionaleconomist@hotmail.com