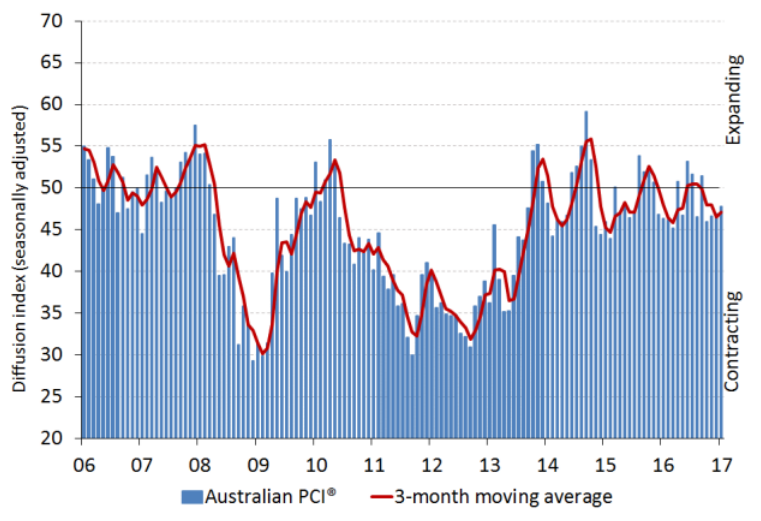

The national construction industry experienced a slow start to 2017 with the Australian Industry Group/Housing Industry Association Australian Performance of Construction Index (Australian PCI®) registering 47.7 points in January (readings below 50 points indicate contraction).

This was an increase of 0.7 points from December, indicating a slight moderation in the rate of decline for the industry as a whole. The Australian PCI® has now been below the 50 points level that separates expansion from contraction for four consecutive months.

The milder decline in the Australian PCI® in January was due to less pronounced reductions in employment and deliveries from suppliers. However, highlighting the soft overall state of business conditions in the sector, both activity and new orders contracted at a slightly steeper rates during the month.

Across the four sub-sectors of the construction industry in the Australian PCI, house building stabilised in January. This follows five consecutive months of declines in house building activity, as the sector moderated from the strong growth levels of mid-2016.

Apartment building and commercial construction remained in negative territory in January, with activity in both sectors declining at broadly unchanged rates from the previous month. Engineering construction activity was weaker at the start of the year after moving close to stabilisation in December, recording its second lowest activity reading in 12 months.

Respondents to the Australian PCI® said that the industry’s soft conditions heading into 2017 were due to subdued overall demand conditions, citing fewer new tender opportunities and a lower volume of new work to replace end-of-year completed projects.

Residential builders mainly commented on slow market conditions due to soft new orders, lower housing sales and caution by prospective buyers.

Reports from Australian PCI® survey respondents also indicated on-going pressures from a highly competitive pricing environment and tight margins.

This will probably get worse before it gets better. Full report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.