From Wilson Advisory:

While we believe housing growth will continue, we have reduced our CY17/CY18 growth forecasts and increased our CY19 growth forecasts…

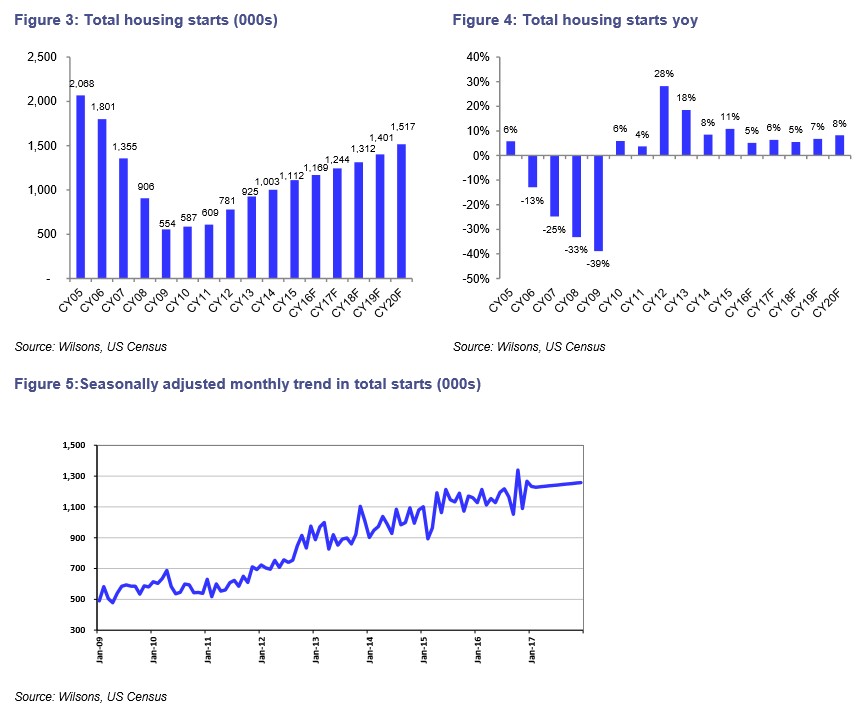

Our forecasts for total US housing starts have declined by -10% to 1,244k starts for CY17. Forecasts have declined -12% in CY18 to 1,312k units and -9% in CY19 to 1,401k units. We note that a significant portion of this reduction is a decline in our multifamily starts forecasts. On a year on year basis, we forecast total US housing starts growth of 6% yoy in CY17, 5% in CY18, 7% in CY19 and 8% in CY20…

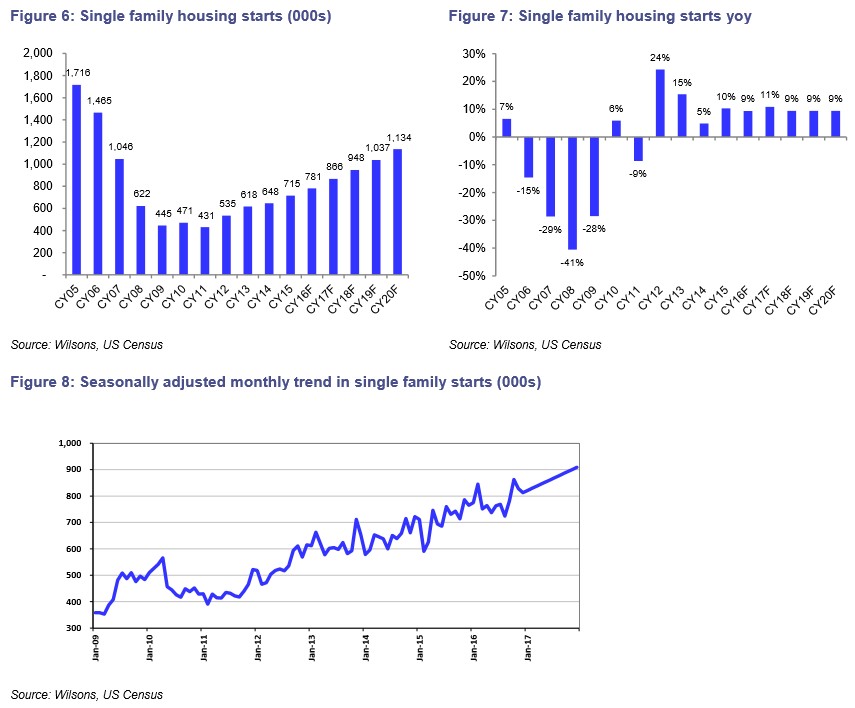

We now forecast 866k and 948k US single family housing starts in CY17 and CY18 respectively. As a result of declines in our US single family housing starts, our yoy growth forecasts have declined marginally in CY17 and CY18 to 11% yoy and 9% yoy respectively (versus previous growth forecast of 15% yoy and 10% yoy respectively). However, we now expect the cycle to last longer and have increased our CY19 forecast from 5% to 9% yoy (+9% yoy in CY20)…

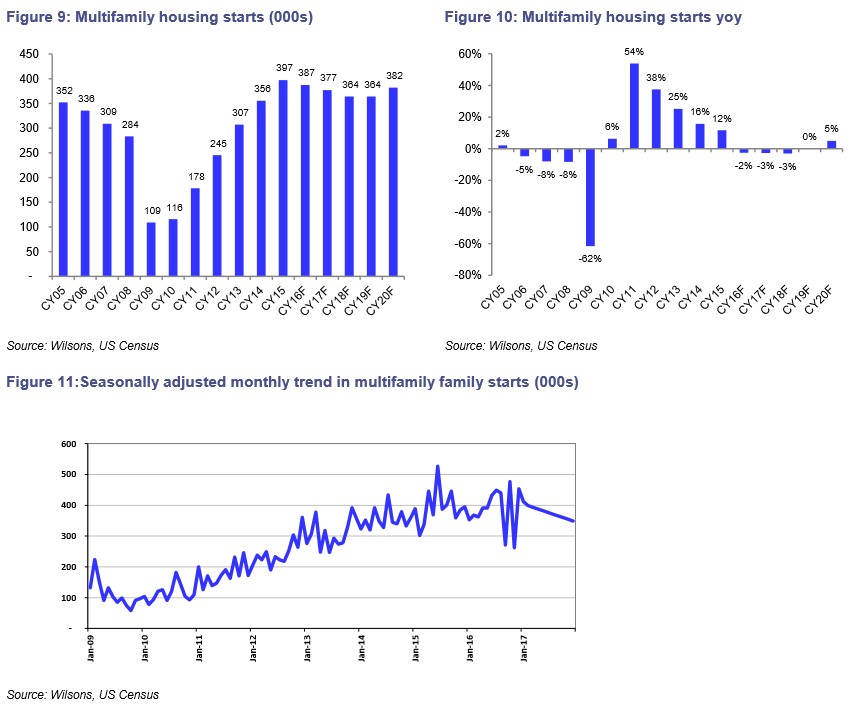

Our forecasts for US multifamily housing starts have declined -15% for CY17 from our previous forecast of 444k units to 377k units. Our forecasts for CY18 and CY19 declined by -20% and -21% respectively to 364k units in both the years (versus our previous forecasts). On a yoy basis, we expect multifamily starts growth to decline by -3% yoy in CY17, -3% yoy in CY18, flat yoy in CY19 and then increase by 5% in CY20…

We believe that our new forecasts are achievable despite an increase in US interest rates. Historically, a 100bps increase in rates has resulted in a 3% decline in new home sales. However, the last time rates were raised over a sustained period (April 2013) new home sales declined 11%. We believe this is unlikely to occur as a result of a rate rise given: 1) the FHA mortgage premium cut helps offset the rate increase; 2) consumer confidence is higher, particularly among lower income groups than in 2013; 3) affordability is still cheap versus rentals; and 4) recent rate increases occurred in the slowest months for home sales.