The Australia Institute (TAI) has released a new report, entitled Company tax and foreign investment in Australia, which comprehensively debunks the arguments used by the Turnbull Government and business lobby to support cutting the company tax rate from 30% to 25%.

Below is the Summary of the TAI report, along with the key charts and tables:

The government’s 10-year company tax cut plan was announced in the May 2016 budget but was always going to be difficult to sell as an urgently needed reform. Since then the debate has effectively shown that there is nothing in it that would increase the incentive to invest. This reflects the role of dividend imputation which acts like a withholding tax for dividend recipients. That means that any cut in company tax would thereby reduce the amount withheld on behalf of dividend recipients and so increase the amount shareholders will have to ‘top up’ at tax time.

These arguments do not apply to foreigners who will unambiguously benefit from Australian company tax cuts. We contend that recognition of the role of foreign investors has caused the Treasurer to downplay any domestic considerations but instead concentrate on the role of foreign investment. Hence foreign investment is presented as a ‘must have’ and the company tax cuts become necessary to encourage foreign investment. Others such as former Prime Minister Paul Keating see it as ridiculous that Australia contemplates giving a large sum of money to foreigners.

The rest of this paper examines whether indeed a company tax cut is likely to boost foreign investment in Australia.

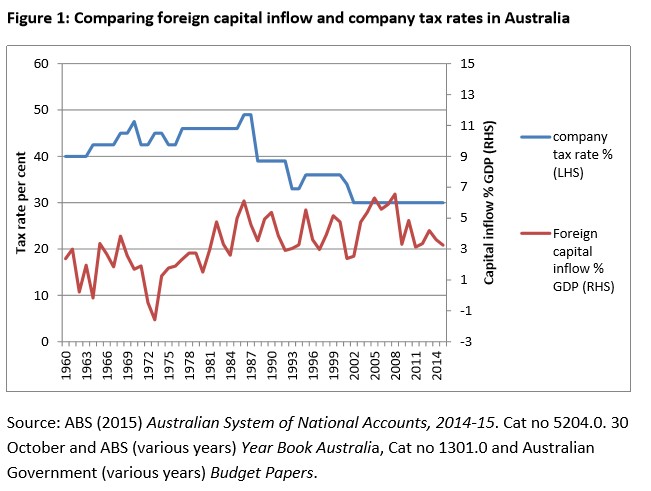

Australia’s company tax rate has gone from 40 per cent in 1960 to a peak of 49 per cent in the 1980s to 30 per cent in 2001 where it is now (except for the 28.5 per cent rate applying to small companies with turnovers to $2 million beginning in July 2015). Under the thesis that tax cuts encourage foreign investment we should have seen first a fall in foreign investment to the late 1980s and then a rise from the late 1980s to the present. In fact the opposite happened in the period to the mid-1980s and then there seems to be no trend in foreign investment as the company tax rate fell.

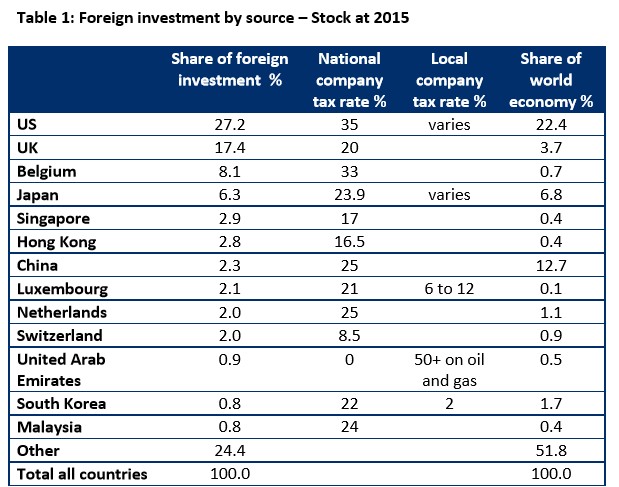

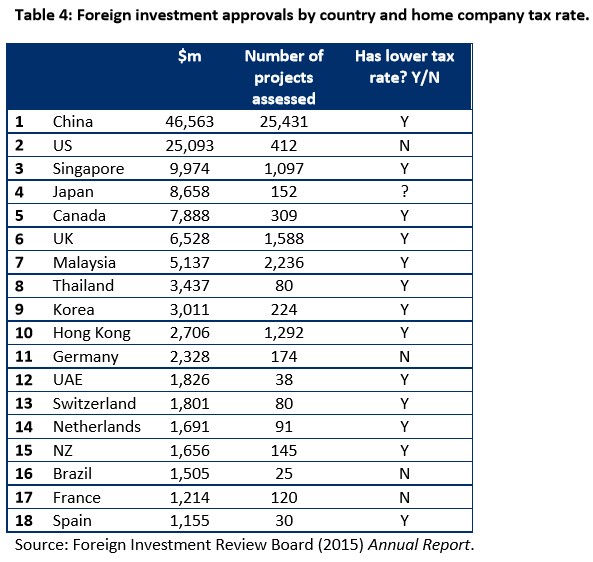

Whatever the past, the Treasurer suggests there is a ‘fight’ to attract foreign capital and company tax is the weapon. That caused us to examine where Australia’s foreign investment comes from and the tax arrangements in the source countries. We find that Australia’s stock of foreign investment is dominated by 13 countries, some with higher and some with lower company tax rates. Nine of these countries have lower company tax rates than Australia’s, yet they invest in Australia out of proportion to their significance in the world economy. For example, the UAE’s share in foreign investment is twice its share of the world economy and its company tax rate is zero!

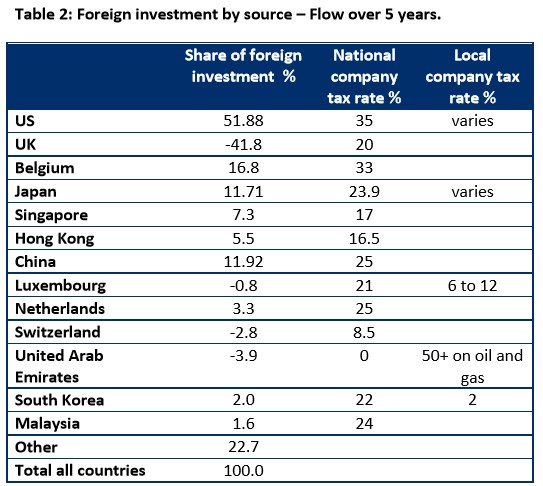

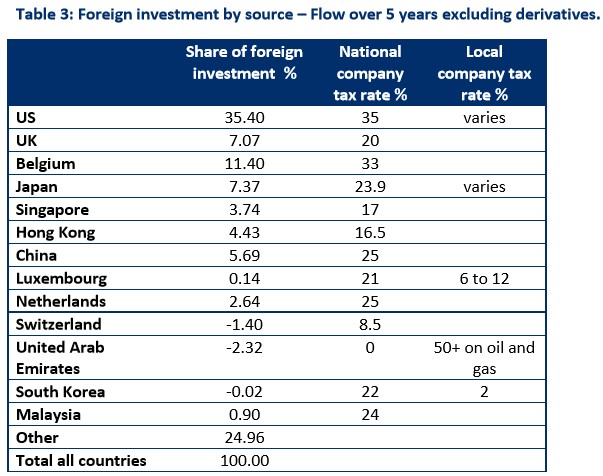

At first the UK seem to confirm the tax cut thesis. It has recently lowered its company tax rate and now shows large negative figures for foreign investment in Australia.

However, that large negative figure reflects financial derivatives and without those UK investment flows have been much higher than the UK’s significance in the world economy and so contradicting the thesis.

We also examined Foreign Investment Review Board figures which confirm that a lot of Australia’s investment comes from countries with lower company tax rates. By value 71 per cent of foreign investment applications come from countries with company tax rates lower than Australia’s rate and by number a large 97 per cent come from countries with company tax rates lower than Australia’s rate. All of this raises the question – if Australia is already successful at attracting foreign investment why would we give tax cuts to foreigners?

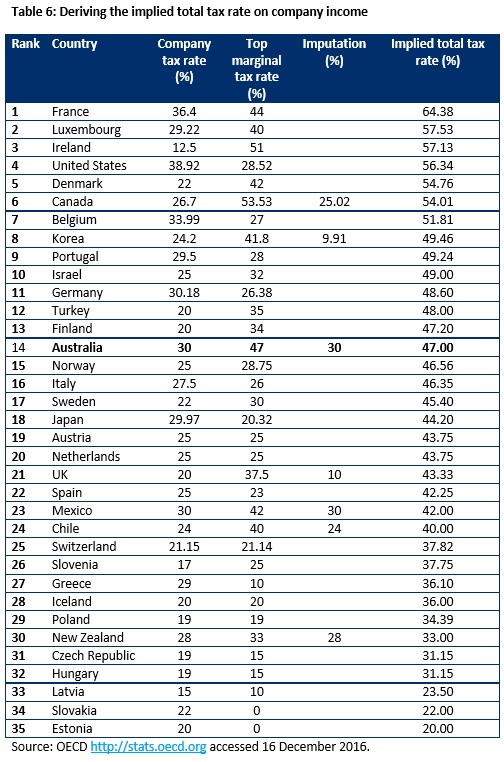

Throughout the whole debate it is assumed that company tax rates are the critical variable affecting investment. However, any returns to the ultimate investors will depend on the individual tax system as well as the company tax and the interaction between the two. When we look at company tax alone Australia has the equal fifth highest among OECD counties yet when we examine the implied total tax rate Australia falls to fourteenth and is only marginally above countries such as the UK.

We conclude that the available evidence suggests that Keating is indeed correct— Australia is on the brink of handing a large gift to foreign investors while the evidence suggests Australia will not get even the dubious benefits of an increase in foreign investment.

Yet another nail in the Turnbull Government’s company tax cut agenda.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.