by Chris Becker

A pretty positive end to the week here in Asia as markets react positively to a mixed lead overnight with moves in currency markets as macro forces really start to weigh at the end of President Trump’s first week in the Oval Office. The Yen and Peso have sold off with Japanese CPI coming in nearly on target but still required the BOJ to step in to purchase bonds while Aussie bonds sold off slightly.

The Shanghai Composite is closed heading into the Chinese New Year while the Hang Seng had a short session, closing flat but futures are indicating a big move higher when it returns next week:

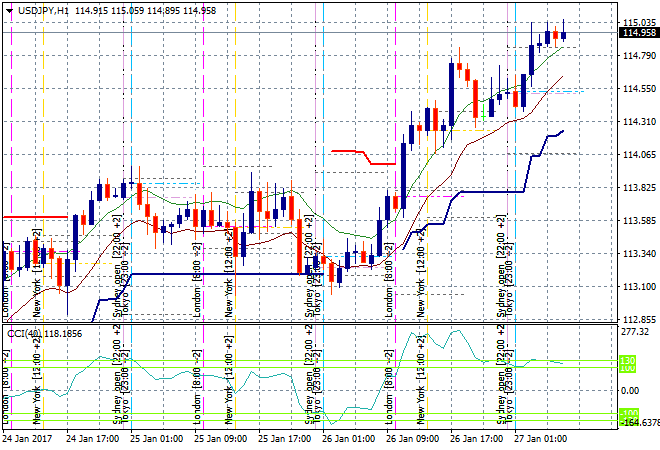

Japanese stocks are having mild rallies today with the Nikkei closing up 0.3% higher as Yen weakened throughout the session, almost at 19500 points and firming here. The hourly chart for USDJPY shows a breakout above resistance at 113.80 or so has had legs up to the 115 handle but we could get a pullback tonight if the GDP print undershoots, so I’m watching the 114.50 zone closely:

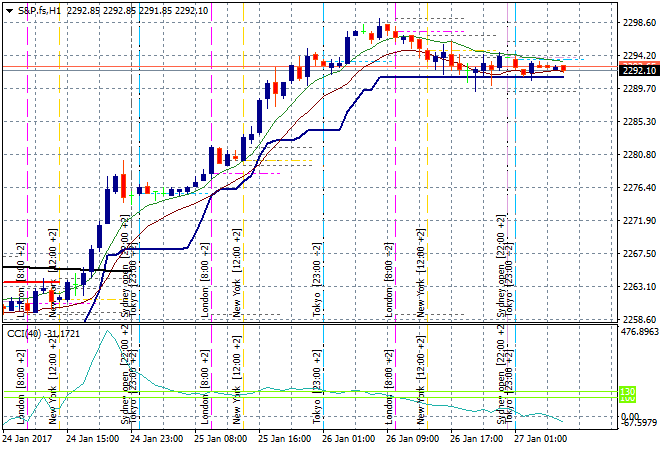

S&P Futures are completely stable given the yuge moves overnight on the broader market. While nominally well overdone, the impetus is there to keep going. Buy construction stocks if Trump announces his inane wall:

The ASX200 had a very solid session to end the week, gaining 0.7% to close back above 5700 points again, driven mainly by bank stocks with the majors up at least 1% or more.

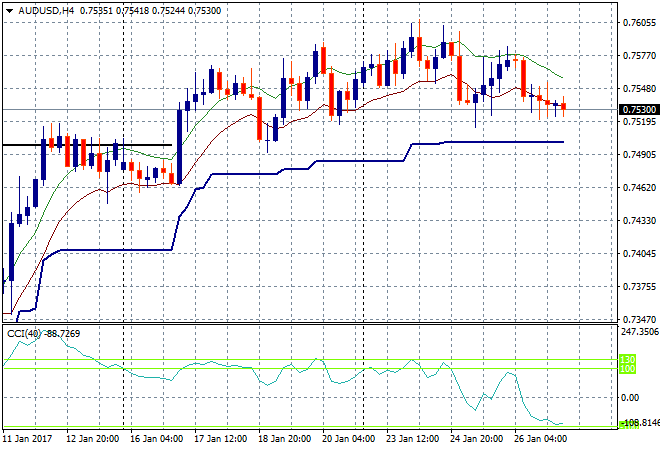

The Aussie dollar is slowly moving down to support against USD, currently hovering just above 75 cents as we head into the London open. This rounding top pattern on the four hourly chart would be confiremd if ATR support at 75 cents proper is closed below tonight:

The data calendar finishes the week with the USD GDP print tonight, alongside durable goods orders.