We have updated our analysis of how sensitive households with an owner occupied mortgage are to an interest rate rise, using data from our household surveys. This is important because we now expect mortgage rates to rise over the next few months, as higher funding costs and competitive dynamics come into pay, and as regulators bear down on lending standards.

To complete this analysis we examine how much headroom households have to rising rates, taking account of their income, size of mortgage, whether they have paid ahead, and other financial commitments. We then run scenarios across the data, until they trip the mortgage stress threshold.

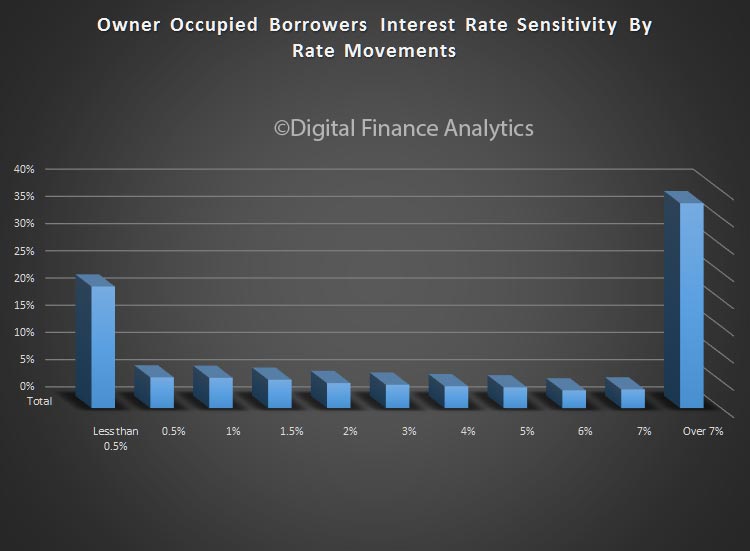

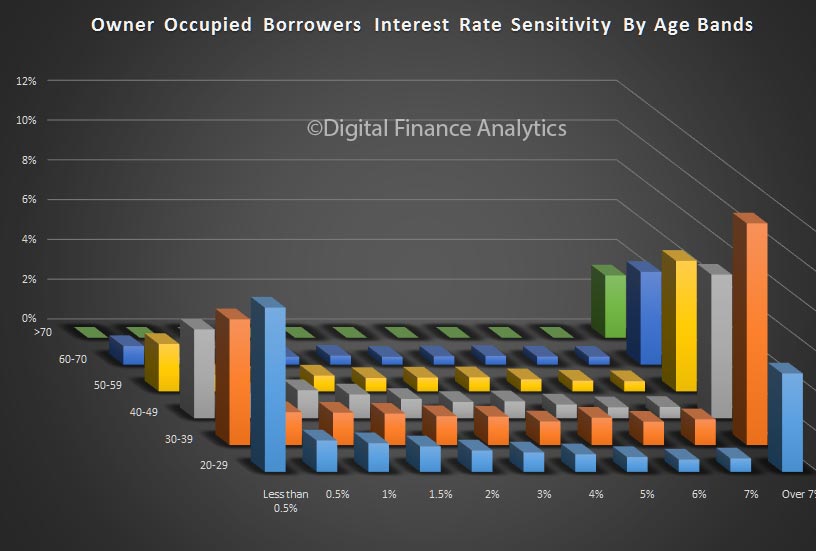

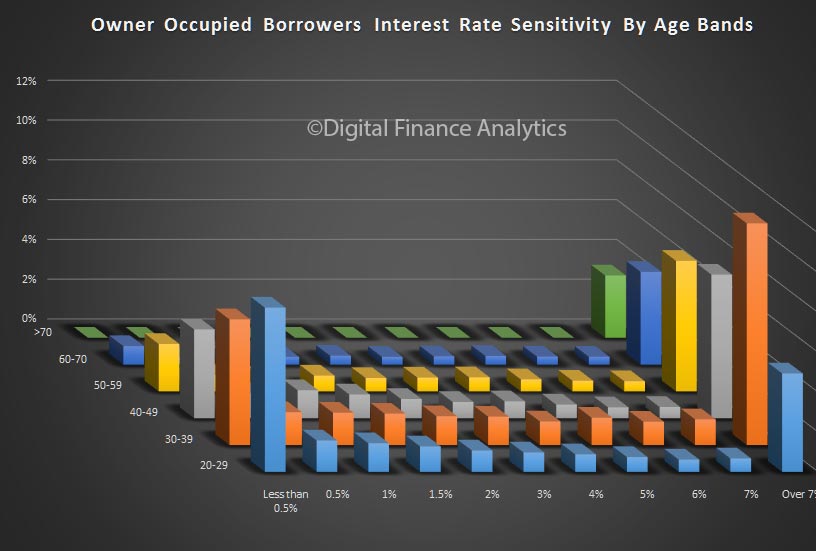

At this level, they will be in difficulty. The chart shows the relative distribution of borrowing households, by number. So, around 20% would have difficulty with even a rise of less than 0.5%, whilst an additional 4% would be troubled by a rise between 0.5% and 1%, and so on. Around 35% could cope with even a full 7% rise.

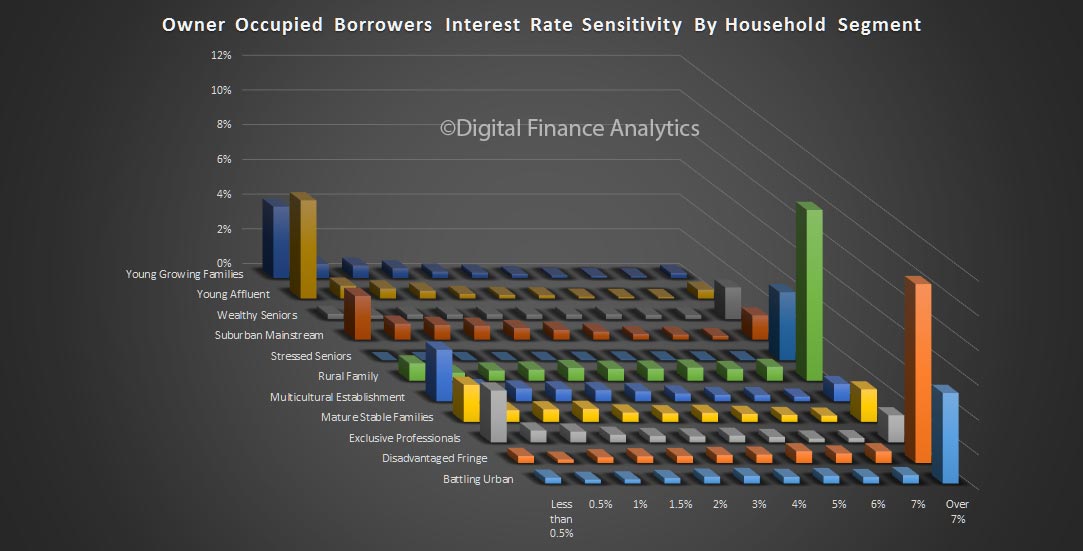

If we overlay our household segments, we find that young growing families and young affluent households are most exposed to a small rate rise. However, some in other segments are also at risk.

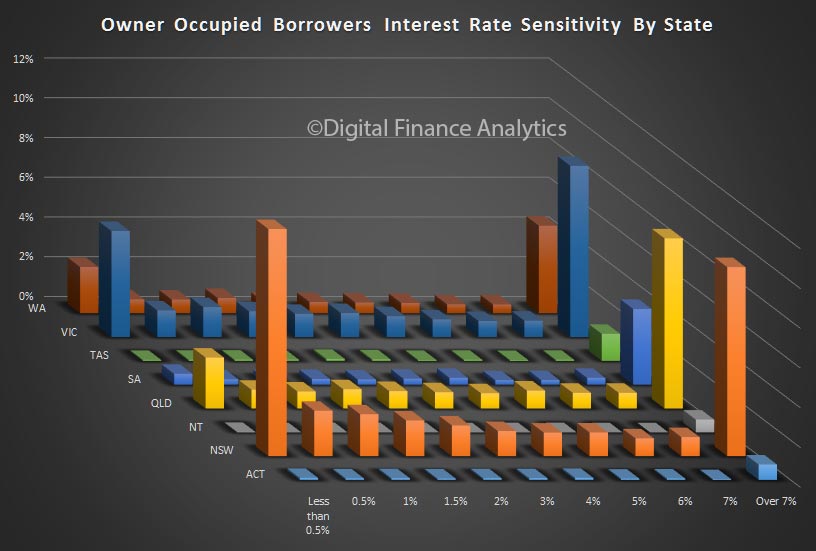

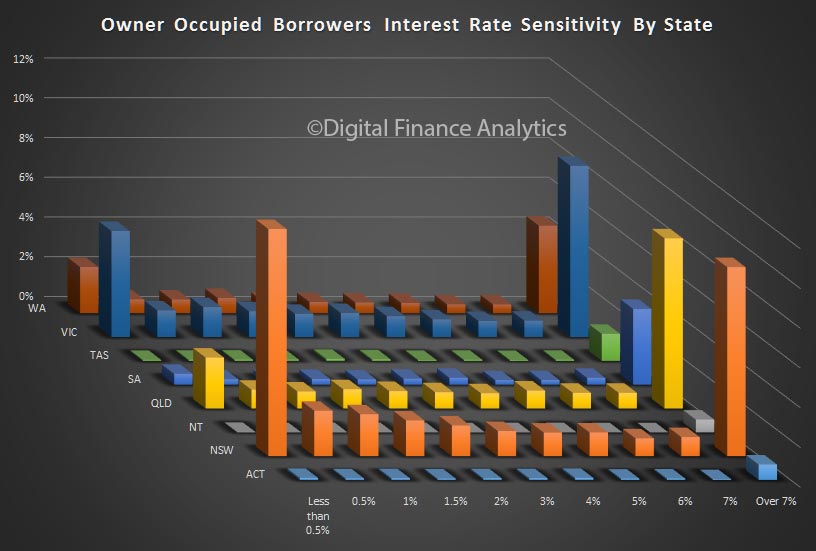

State analysis highlights that households in NSW are most sensitive, a combination of larger volumes of loans as well a larger loans, relative to incomes resulting is less headroom.

Younger households are relatively more exposed, because their incomes tend to be more limited and are not growing in real terms relative to mortgage repayments.

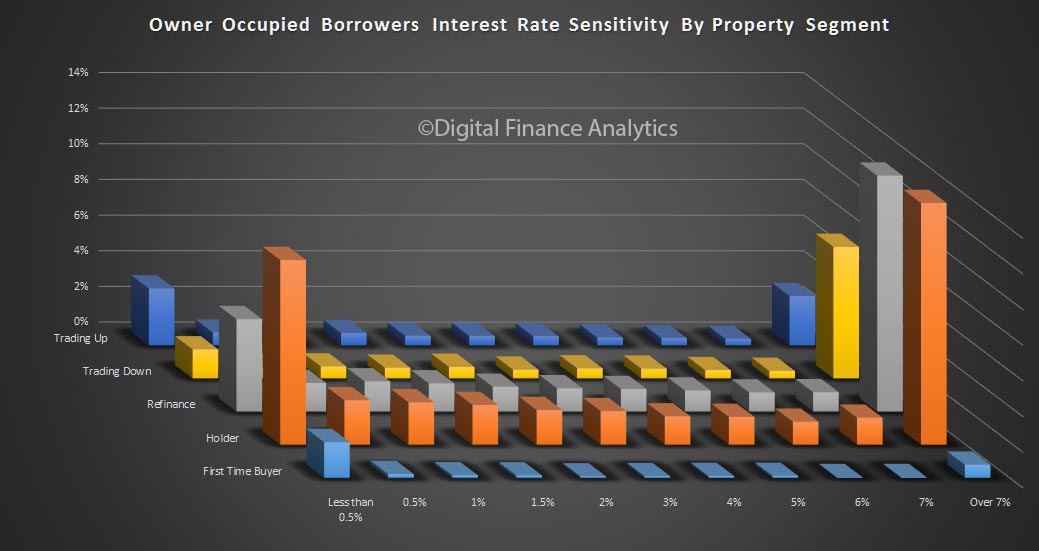

Analysis by DFA property segment shows that whilst some first time buyers are exposed at low rate movements, those holding a mortgage with no plans to change their properties (holders) are also exposed. In addition, some seeking to refinance are doing so in the hope of reducing payments, because they have limited headroom.

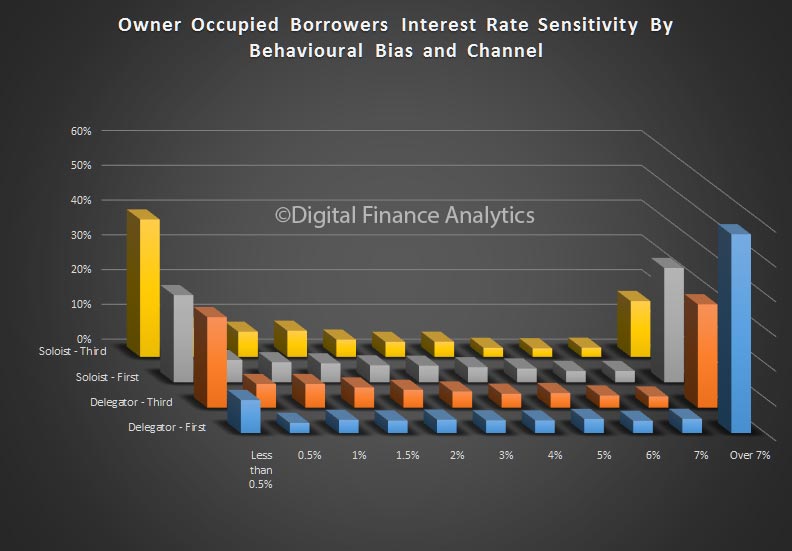

Finally we turn to other insights from our data. First, those households who sourced their mortgage via a mortgage broker are more likely to be in difficulty with a small rate rise, compared with those who went direct to a bank. This, once again, shows third party loans are more risky. This perhaps is connected to the types of people using brokers, as well as the broker’s ability to suggest lenders with more generous underwriting standards and coaching on how to apply successfully.

We also see that rate seekers (we call these soloists) who are driven primarily by best rates, are more sensitive to small rate rises, compared with those who are more inclined to seek advice, and appreciate service more than price (we call these delegators).

Soloists who went via a broker are the most exposed should rates rise even a little, whereas delegators going to a bank, are more able to handle future rises.

Segmentation, effectively applied can results in quite different portfolio outcomes!

{kind=link}

{kind=link}